港股收評:恒科指險守3000點,蘋果概念股重挫,教育、煤炭板塊逆勢上揚

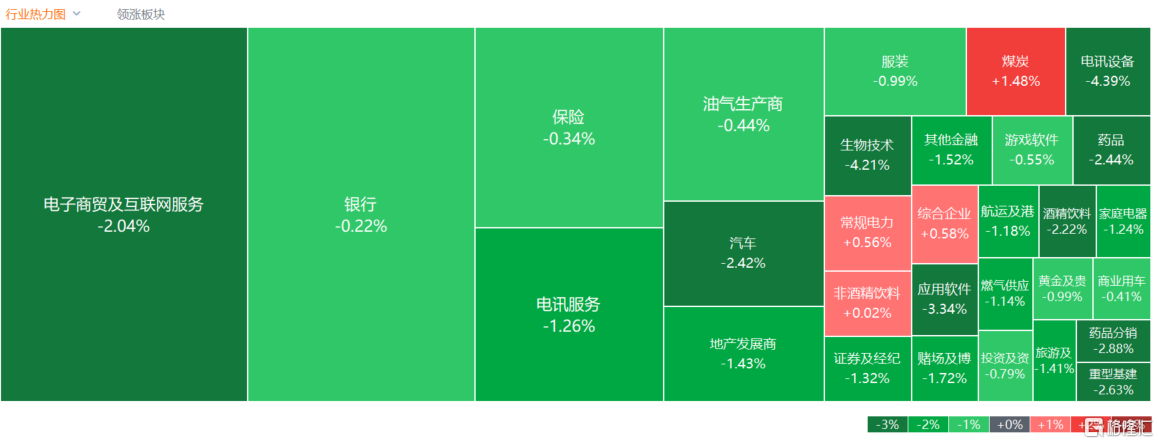

1月31日,港股午後跌幅繼續擴大,市場情緒十分低迷,熱門行業板塊近乎全部下挫。截至收盤,恒生科技指數收跌3%表現最差,險守3000點關口,恒指、國指分別下跌1.39%及1.54%,三大指數均錄得2連跌行情。1月交易收官,恒生科技指數累計跌幅超20%,恒指、國指跌超9%。

盤面上,大型科技股繼續表現弱勢大市承壓,美團跌超4%,京東、阿里巴巴、百度、騰訊皆走低;前期助力大市上升的中字頭股表現分歧,中國中鐵跌超6%,中國太平、中國中免、中國國航、中國外運、中國海洋石油等紛紛下挫;蘋果概念股跌幅明顯,汽車股、餐飲股、半導體股、濠賭股、手遊股、光伏股、家電股齊跌。另一方面,在線教育股部分走勢較好,收入增速超業績指引,新東方升近1%;煤炭股中國神華髮盈警,股價反而刷新階段新高。

具體來看:

大型科技股繼續表現弱勢大市承壓,小米、美團跌超4%,京東、快手跌超3%,阿里巴巴跌超2%,騰訊跌超1%。

蘋果概念股受挫,舜宇光學科技跌超11%,瑞聲科技跌7.68%,丘鈦科技跌5.5%,高偉電子跌4.42%。天風國際分析師郭明錤最新研報稱,蘋果已下調上游關鍵半導體零組件的2024年iPhone出貨預估至約2億部(同比衰退15%)。他認為,2024年全球主要手機品牌中,蘋果可能是衰退幅度最大者,尤其是中國市場出貨量持續下滑。

體育用品股普跌,安踏體育跌超5%,李寧跌超3%,361度、特步國際跟跌。

餐飲股延續跌勢,九毛九、海底撈跌超4%,呷哺呷哺、奈雪的茶跌超4%。野村發佈研報稱,餐飲業消費情緒去年第四季疲軟情況可能延續至今年首季,並認為投資者短期對內地餐飲股的投資情緒仍然低迷,該行繼續偏好展示更精簡及靈活業務模式,以及近期營運數據潛在上升的股份。基於持續推廣環境及高基數效應,該行覆蓋的股份,其中包括九毛九等企業的盈利率在今年或持續受壓。

半導體板塊下跌,上海復旦跌超7%,華虹半導體跌5.46%,中芯國際跌2.36%。消息面上,AMD公佈,公司上一財季實現營收62億美元,超出分析師預期。但今年一季度的營收指引只有54億美元,低於市場預期的57億美元。公司股價盤後下跌超6%。AMD稱,上半年的加速器產能趨緊,預計將在下半年改善;每個季度的加速器營收都將增長;有足夠的供應超過35億美元的AI芯片目標。

汽車股表現疲軟,蔚來、小鵬汽車、零跑汽車跌超5%,長城汽車跌超3%,比亞迪股份跌超2%。

教育股多數走強,東方甄選升超6%,中國新華教育、卓越教育集團升超3%,楓葉教育、新東方-S跟升。廣發證券指出,教育板塊業績與估值雙重修復趨勢可延續。年初至今,教育行業剛需屬性凸顯,外部影響因素解除後業務開展快速恢復,同時政策情緒穩步改善支撐估值向合理中樞修復。K12課外培訓:規範化發展或推動行業格局重塑,龍頭充分受益;職業技能培訓:招生穩步恢復,業績釋放可期;企業管理培訓:行業需求韌性較強,龍頭差異化優勢支撐亮眼表現;民辦學校:高教業績穩增長估值有望修復,義務教育學校探索成長新路徑。

部分煤炭股逆勢上揚,蒙古焦煤、兗煤澳大利亞、中國神華升超2%,易大宗、中煤能源紛紛上升。

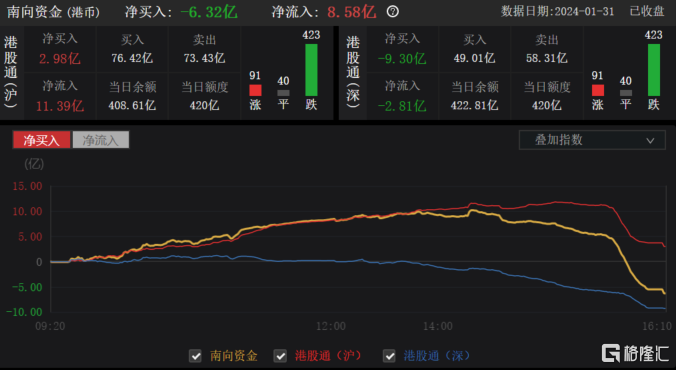

今日,南向資金淨賣出6.32億港元,其中港股通(滬)淨買入2.98億港元,港股通(深)淨賣出9.30億港元。

展望未來,光大證券指出,後續在政策積極發力下,港股市場也有望企穩回升。在政治局會議及中央經濟工作會議定調之後,近期陸續有更為具體的穩增長政策出台,包括央行在1月24日宣佈降準、房地產政策持續優化、萬億特別國債兩批項目清單下達、銀行調整存款利率等。可以預見,未來大概率還會有更多穩增長政策出台落地,並助力經濟逐漸回暖。

配置方向上,建議關注:1)產業景氣與AI主線並存的半導體、通信、電子等科技股。2)政治局會議強調,“切實提高國有企業核心競爭力”,建議繼續關注“中特估”主題,包括建築裝飾、石油石化、銀行、煤炭等行業。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.