美股週報(4.18) | CPI 8.5%再創40年新高,核心通脹低於預期;美債收益率曲線繼續走高,三大股指回調;能源和消費板塊持續表現優異,航空酒旅反彈

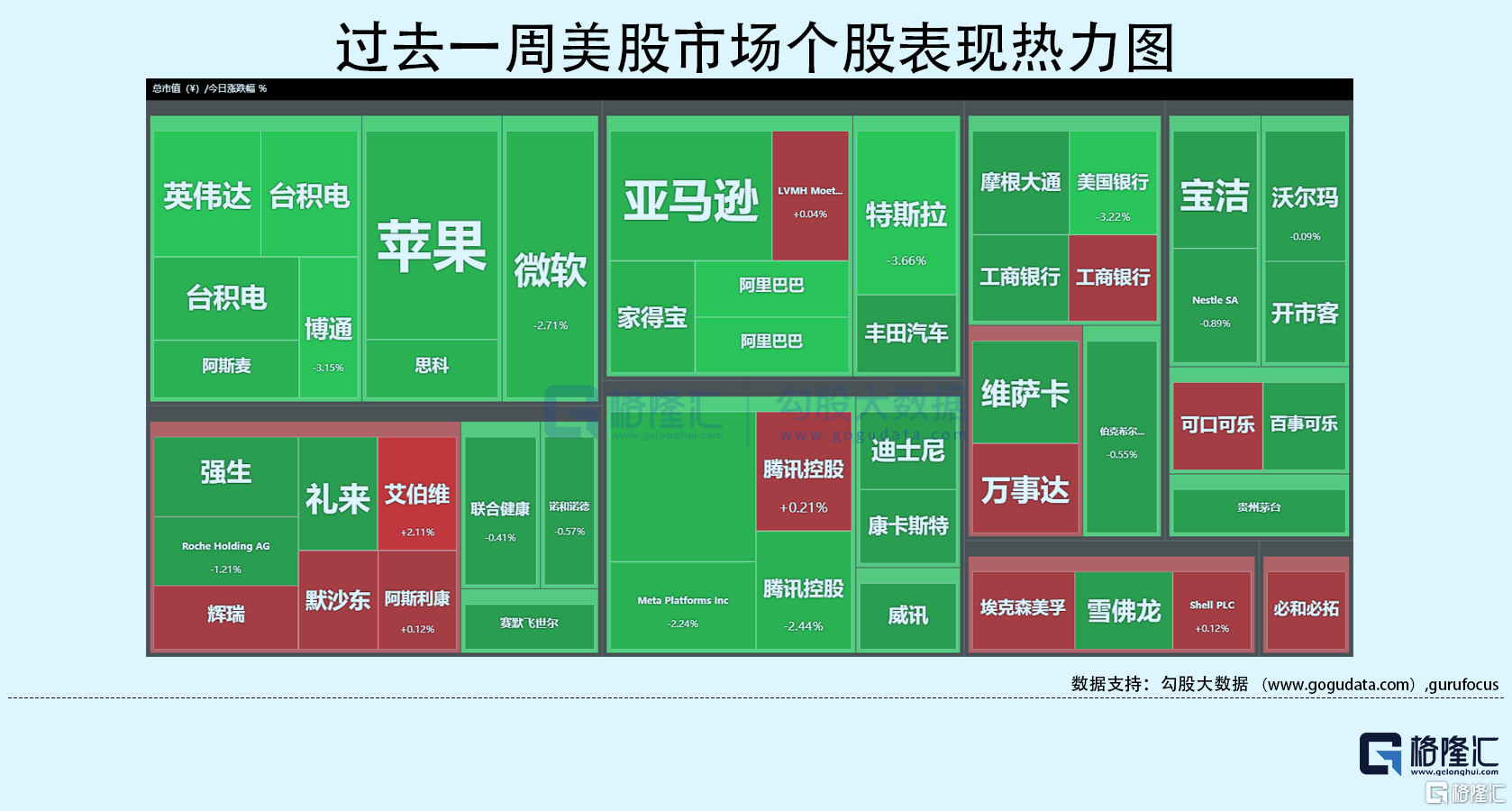

上週美股整體回調。標普收跌2.1%,納指跌2.6%,道指表現相對穩定,收跌0.78%。美國十年國債收益率漲4.4%,收報2.83%,與兩年期國債收益率息差38個基點,相較上週繼續擴大。恐慌指數週漲幅為7.28%。油價重新大漲,WTI和布倫特原油均漲約9%。現貨黃金收漲1.5%,收報1974美元/盎司。

大盤主要走通脹邏輯,表現較好、創新高的集中在能源大宗、必選消費和醫藥醫療等板塊。重點事件包括:中美10年國債收益率近12年來首次倒掛,中國疫情政策可能轉向,盤面體現為航空酒旅強勢反彈。美國3月CPI同比增長8.5%基本在預期內,環比增長0.3%顯著低於預期,也低於此前幾個月的增幅,這讓市場中出現不少認為通脹見頂的聲音。

多位美聯儲官員講話,不過沒什麼新內容,核心圍繞着經濟增長可以匹配美聯儲的緊縮政策,即經濟軟着陸。加息縮表對定價邊際影響已較弱,從點陣圖來看,22年底利率2.5%沒有變動,定價波動主要來自於23年底預期利率——週四收盤報3%,即週中盤面主要圍繞23年多或少加息1次變動。5月、6月加息50個基點的概率不斷提升,5月加息50個基點基本板上釘釘。收益率曲線繼續走高,但邊際變動小。

行業板塊方面,標普11大板塊表現不一。能源和原材料板塊表現較好,分別收漲0.4%、0.66%。必選消費在超市、可樂等帶動下表現穩健,整體小幅收漲0.15%。工業板塊漲0.3%。高科技板塊跌幅居前,周跌幅達3.8%,醫療保健板塊跌3%,金融板塊跌2.6%,通訊板塊跌2.3%。公用事業板塊跌1%。

半導體板塊繼續走弱,費城半導體指數週跌3%,主要反映消費電子退潮的預期。具體而言,投行如高盛等認為由於中國對疫情的封控、俄烏衝突,以及全球性通脹,包括個人電腦、智能手機等在內的消費電子的需求將減弱,這對於芯片股無疑是較大利空。台積電週四盤前發佈超預期財報,但沒有能帶動板塊反彈。據財報和電話會紀要,台積電判斷消費電子需求近期確實在走弱,但同時表示汽車、高性能計算HPC等需求仍然強勁,公司今年增長目標和資本支出維持不變。

本週重點財經數據與事件:

週一中國公佈第一季度GDP數據。

週二美國公佈3月新屋開工數據;聖路易斯聯儲主席布拉德發表講話。

週三德國公佈3月PPI數據;美國公佈至4月15日當週原油庫存。

週四歐洲公佈3月CPI數據;美國公佈4月費城聯儲製造業指數。

週五美聯儲主席鮑威爾和歐洲央行行長拉加德參與IMF小組討論並講話。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.