奧飛娛樂(002292.SZ)深度報告:聚焦與變革,有望重回增長

作者:蔡靖

來源:楊仁文研究筆記

核心觀點:

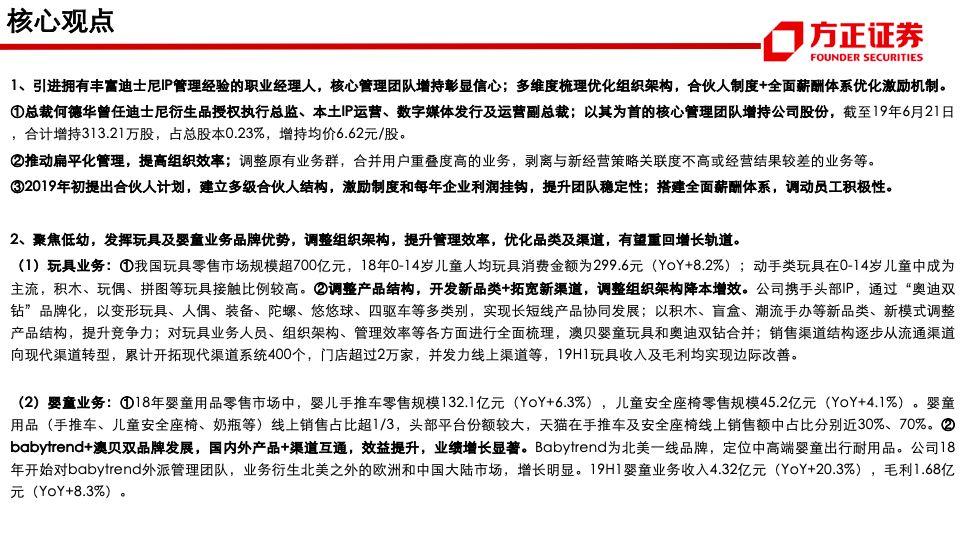

1、引進擁有豐富迪士尼IP管理經驗的職業經理人,核心管理團隊增持彰顯信心;多維度梳理優化組織架構,合夥人制度+全面薪酬體系優化激勵機制。

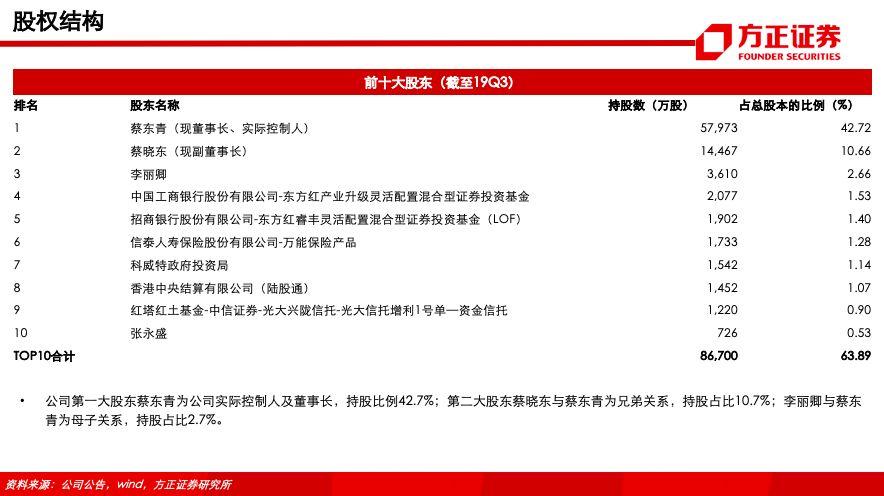

①總裁何德華曾任迪士尼衍生品授權執行總監、本土IP運營、數字媒體發行及運營副總裁;以其為首的核心管理團隊增持公司股份,截至19年6月21日,合計增持313.21萬股,佔總股本0.23%,增持均價6.62元/股。

②推動扁平化管理,提高組織效率;調整原有業務羣,合併用户重疊度高的業務,剝離與新經營策略關聯度不高或經營結果較差的業務等。

③2019年初提出合夥人計劃,建立多級合夥人結構,激勵制度和每年企業利潤掛鈎,提升團隊穩定性;搭建全面薪酬體系,調動員工積極性。

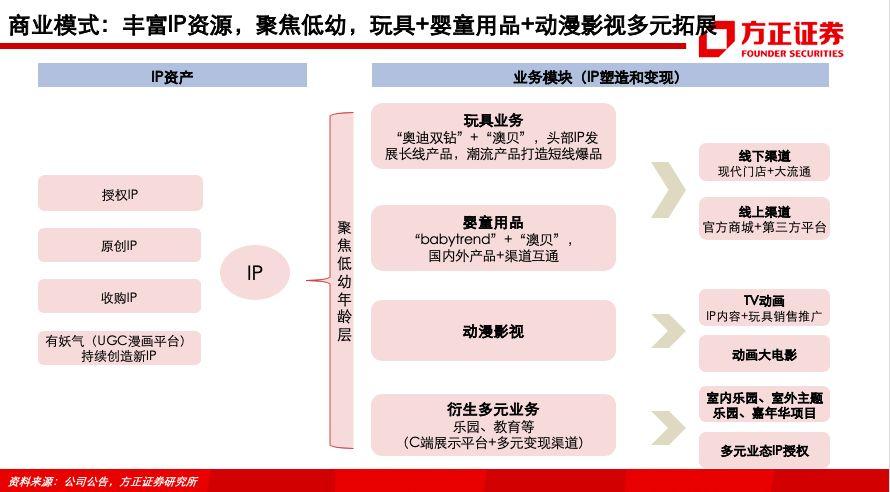

2、聚焦低幼,發揮玩具及嬰童業務品牌優勢,調整組織架構,提升管理效率,優化品類及渠道,有望重回增長軌道。

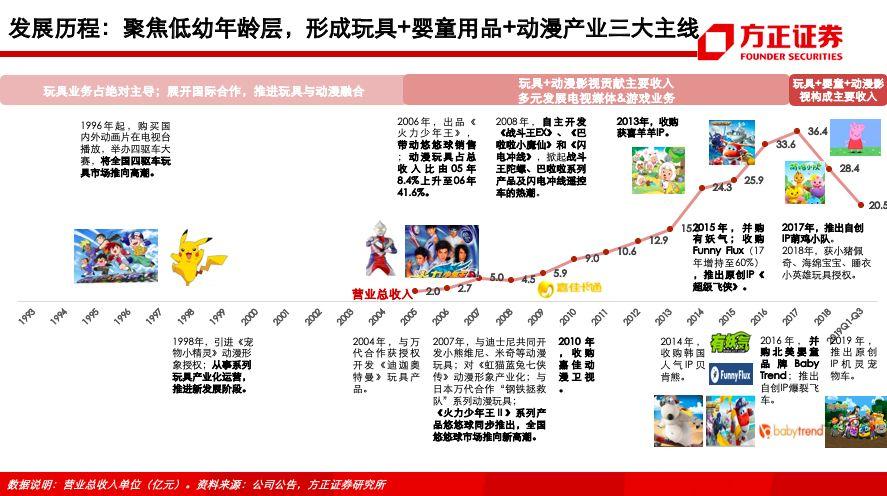

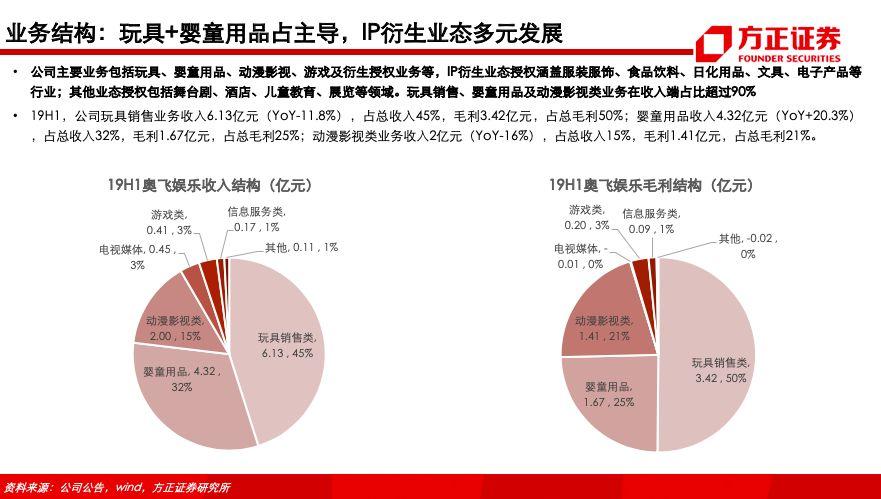

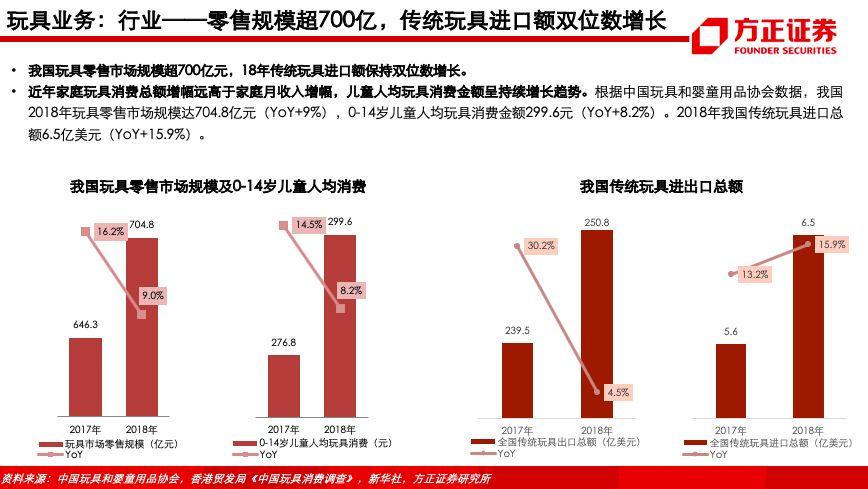

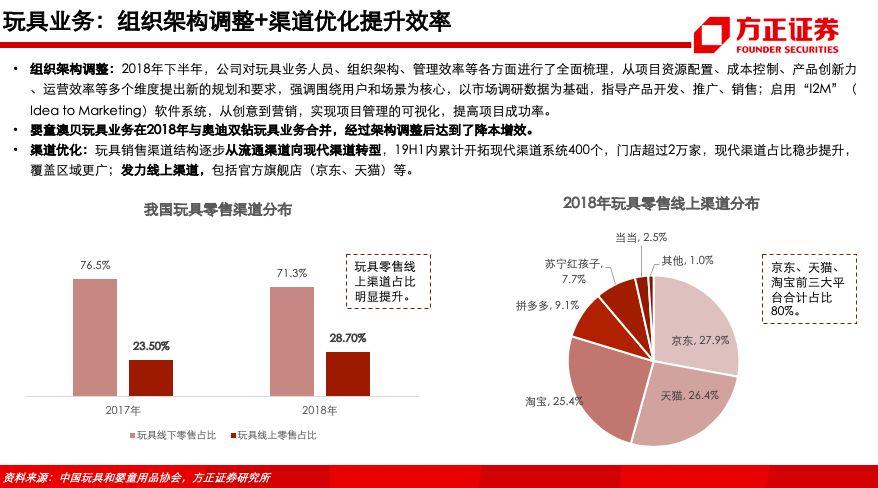

(1)玩具業務:①我國玩具零售市場規模超700億元,18年0-14歲兒童人均玩具消費金額為299.6元(YoY+8.2%);動手類玩具在0-14歲兒童中成為主流,積木、玩偶、拼圖等玩具接觸比例較高。②調整產品結構,開發新品類+拓寬新渠道,調整組織架構降本增效。公司攜手頭部IP,通過“奧迪雙鑽”品牌化,以變形玩具、人偶、裝備、陀螺、悠悠球、四驅車等多類別,實現長短線產品協同發展;以積木、盲盒、潮流手辦等新品類、新模式調整產品結構,提升競爭力;對玩具業務人員、組織架構、管理效率等各方面進行全面梳理,澳貝嬰童玩具和奧迪雙鑽合併;銷售渠道結構逐步從流通渠道向現代渠道轉型,累計開拓現代渠道系統400個,門店超過2萬家,併發力線上渠道等,19H1玩具收入及毛利均實現邊際改善。

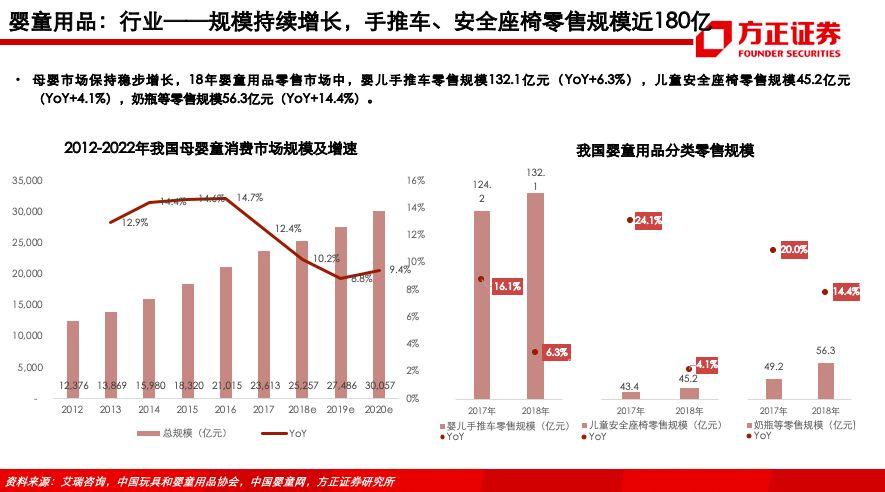

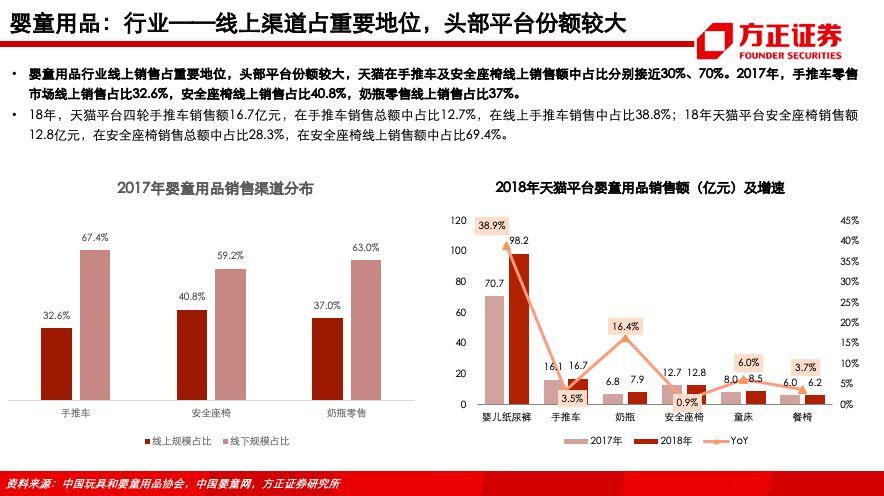

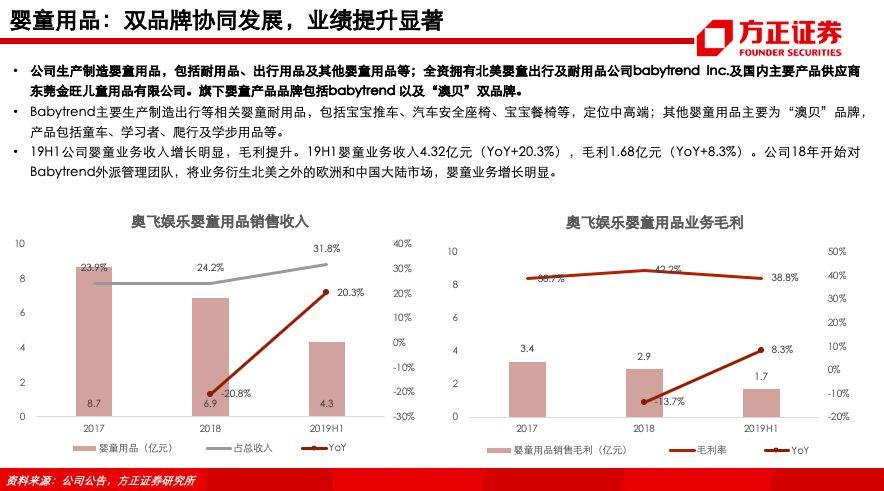

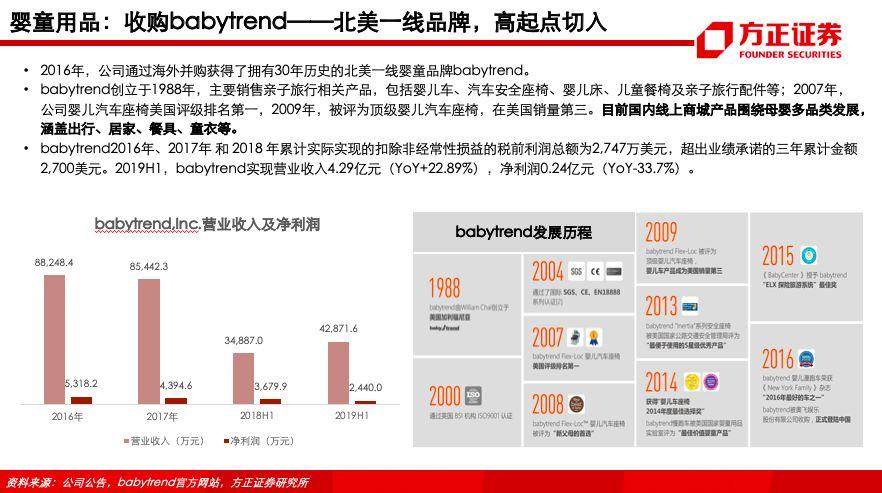

(2)嬰童業務:①18年嬰童用品零售市場中,嬰兒手推車零售規模132.1億元(YoY+6.3%),兒童安全座椅零售規模45.2億元(YoY+4.1%)。嬰童用品(手推車、兒童安全座椅、奶瓶等)線上銷售佔比超1/3,頭部平台份額較大,天貓在手推車及安全座椅線上銷售額中佔比分別近30%、70%。② babytrend+澳貝雙品牌發展,國內外產品+渠道互通,效益提升,業績增長顯著。Babytrend為北美一線品牌,定位中高端嬰童出行耐用品。公司18年開始對babytrend外派管理團隊,業務衍生北美之外的歐洲和中國大陸市場,增長明顯。19H1嬰童業務收入4.32億元(YoY+20.3%),毛利1.68億元(YoY+8.3%)。

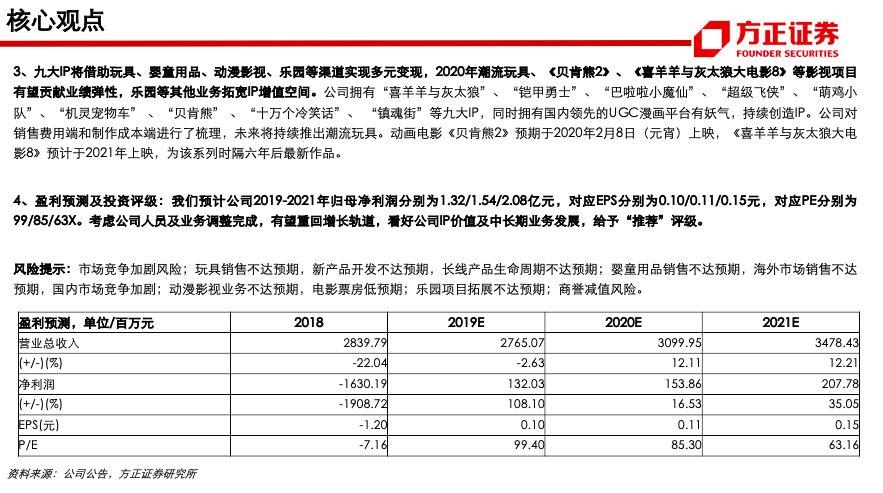

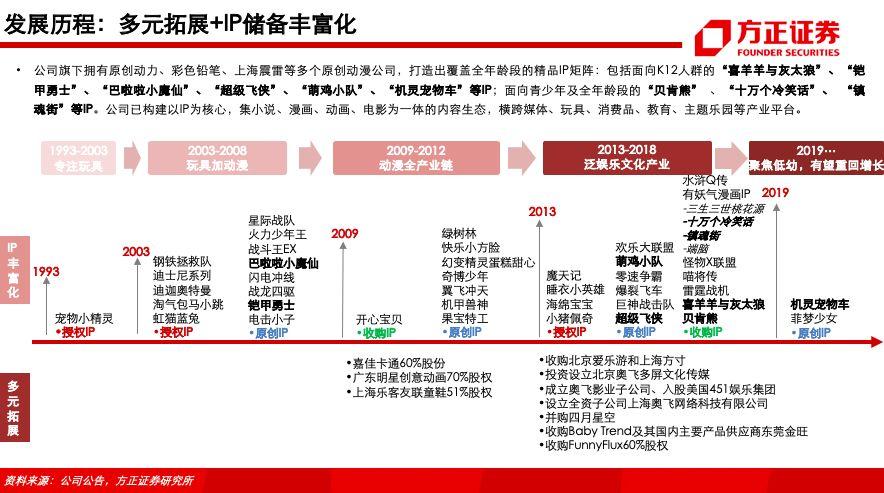

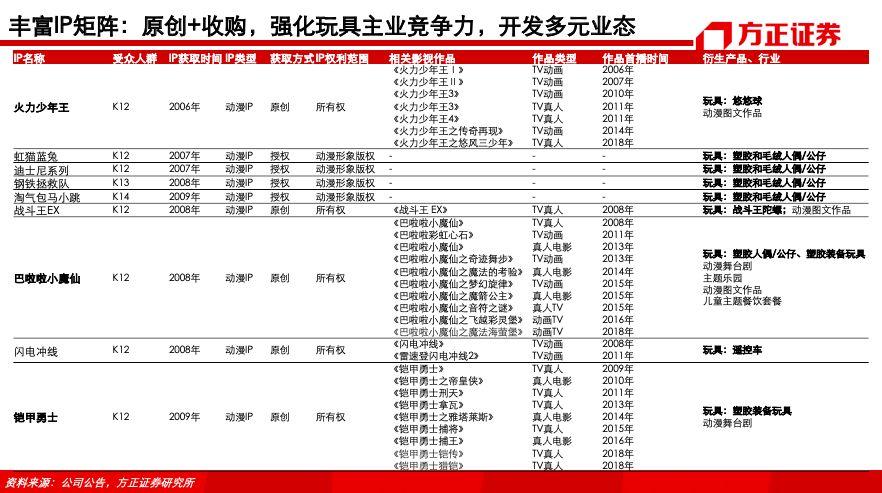

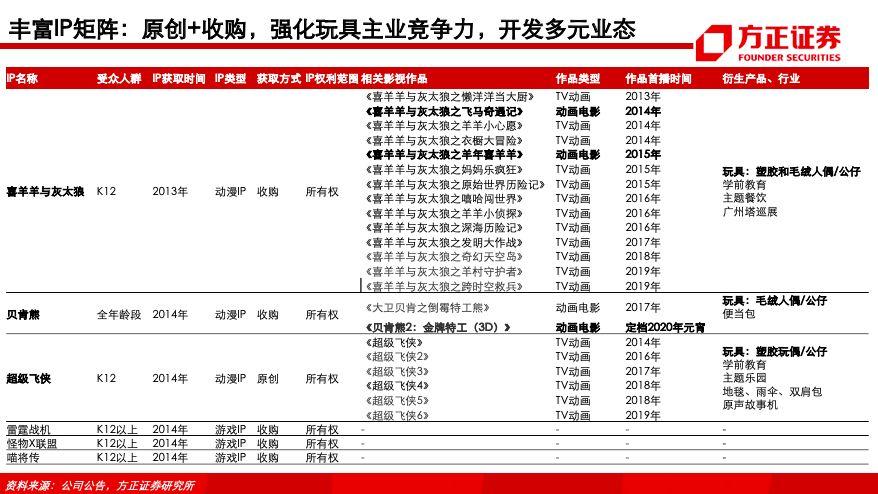

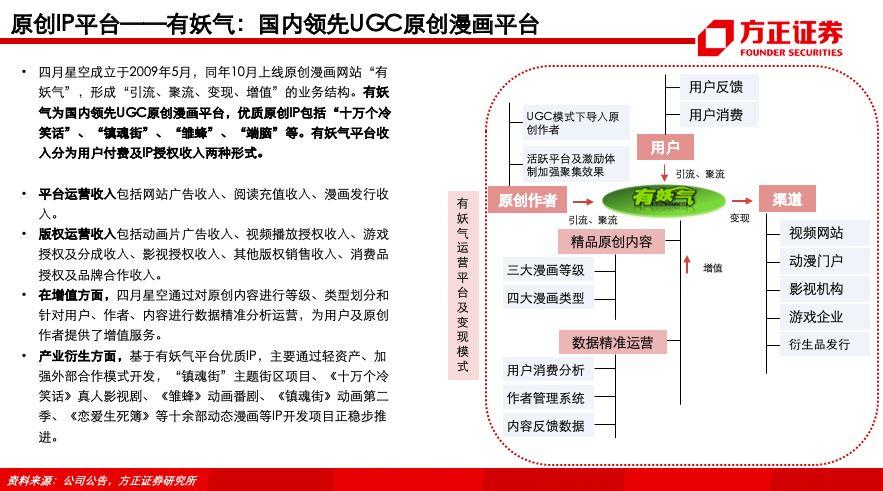

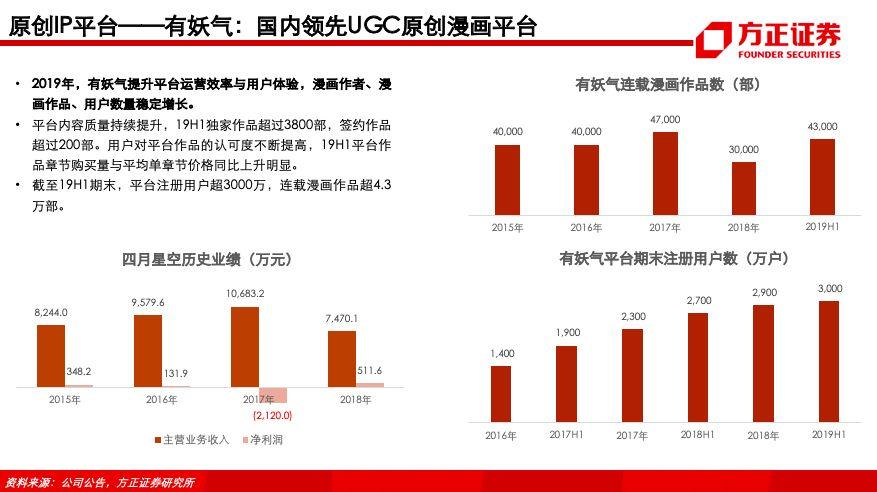

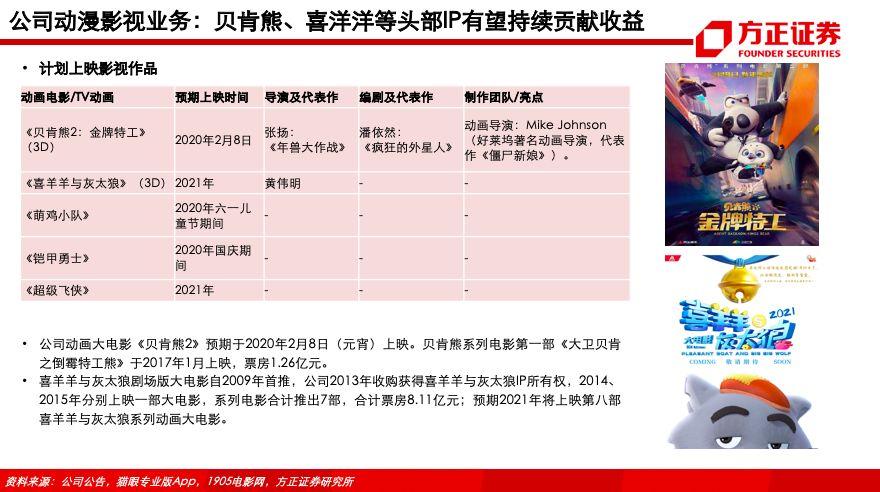

3、九大IP將藉助玩具、嬰童用品、動漫影視、樂園等渠道實現多元變現,2020年潮流玩具、《貝肯熊2》、《喜羊羊與灰太狼大電影8》等影視項目有望貢獻業績彈性,樂園等其他業務拓寬IP增值空間。公司擁有“喜羊羊與灰太狼”、“鎧甲勇士”、“巴啦啦小魔仙”、“超級飛俠”、“萌雞小隊”、“機靈寵物車” 、“貝肯熊” 、“十萬個冷笑話”、 “鎮魂街”等九大IP,同時擁有國內領先的UGC漫畫平台有妖氣,持續創造IP。公司對銷售費用端和製作成本端進行了梳理,未來將持續推出潮流玩具。動畫電影《貝肯熊2》預期於2020年2月8日(元宵)上映,《喜羊羊與灰太狼大電影8》預計於2021年上映,為該系列時隔六年後最新作品。

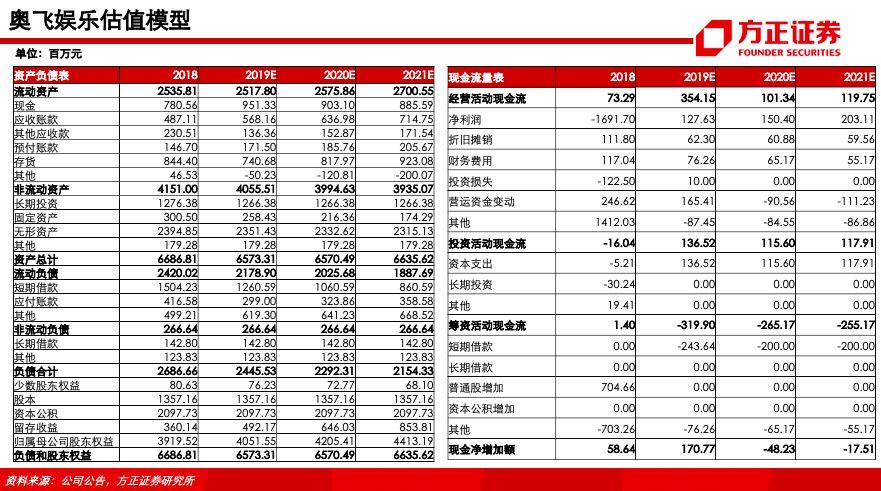

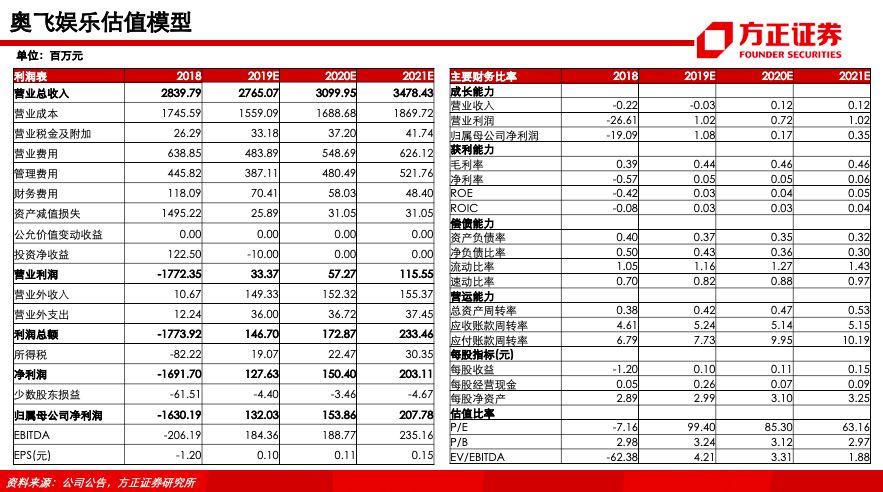

4、盈利預測及投資評級:我們預計公司2019-2021年歸母淨利潤分別為1.32/1.54/2.08億元,對應EPS分別為0.10/0.11/0.15元,對應PE分別為99/85/63X。考慮公司人員及業務調整完成,有望重回增長軌道,看好公司IP價值及中長期業務發展,給予“推薦”評級。

風險提示:市場競爭加劇風險;玩具銷售不達預期,新產品開發不達預期,長線產品生命週期不達預期;嬰童用品銷售不達預期,海外市場銷售不達預期,國內市場競爭加劇;動漫影視業務不達預期,電影票房低預期;樂園項目拓展不達預期;商譽減值風險。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.