環球一覽 | 美通脹重回“6時代”,為美聯儲放慢加息步伐留出空間;美聯儲大鷹派稱希望儘快加息到5%以上

美東時間週四,美股三大指數震盪收漲,延續近期漲勢。截至收盤,道指漲0.64%,報34189.97點;納指漲0.64%,報11001.10點;標普500指數漲0.34%,報3983.17點。通脹顯示出緩解跡象,這可能使美聯儲有理由繼續放慢加息步伐,以防止經濟進一步下滑。

熱門中概股漲跌不一,蔚來、滿幫漲超2%,理想汽車、網易、小鵬汽車漲超1%,騰訊音樂、拼多多、京東小幅上漲。愛奇藝、富途控股跌超2%,微博、阿里巴巴、百度跌超1%,嗶哩嗶哩、唯品會小幅下跌。

大型科技股多數上漲,Meta漲近3%,微軟漲超1%,亞馬遜、奈飛小幅上漲;蘋果、谷歌A小幅下跌。

其他個股方面,3B家居繼續狂飆突進,收漲逾50%,本週四個交易日累計漲幅約300%,觸及去年11月初以來的最高水平,此前該公司的破產警吿重新點燃了投資者對這家零售商的興趣。3B家居的暴漲也帶動了一眾MEME股,Carvana漲逾46%,遊戲驛站漲8%。

歐股收盤全線上漲,德國DAX指數漲0.74%報15058.3點,法國CAC40指數漲0.74%報6975.68點,英國富時100指數漲0.89%報7794.04點。

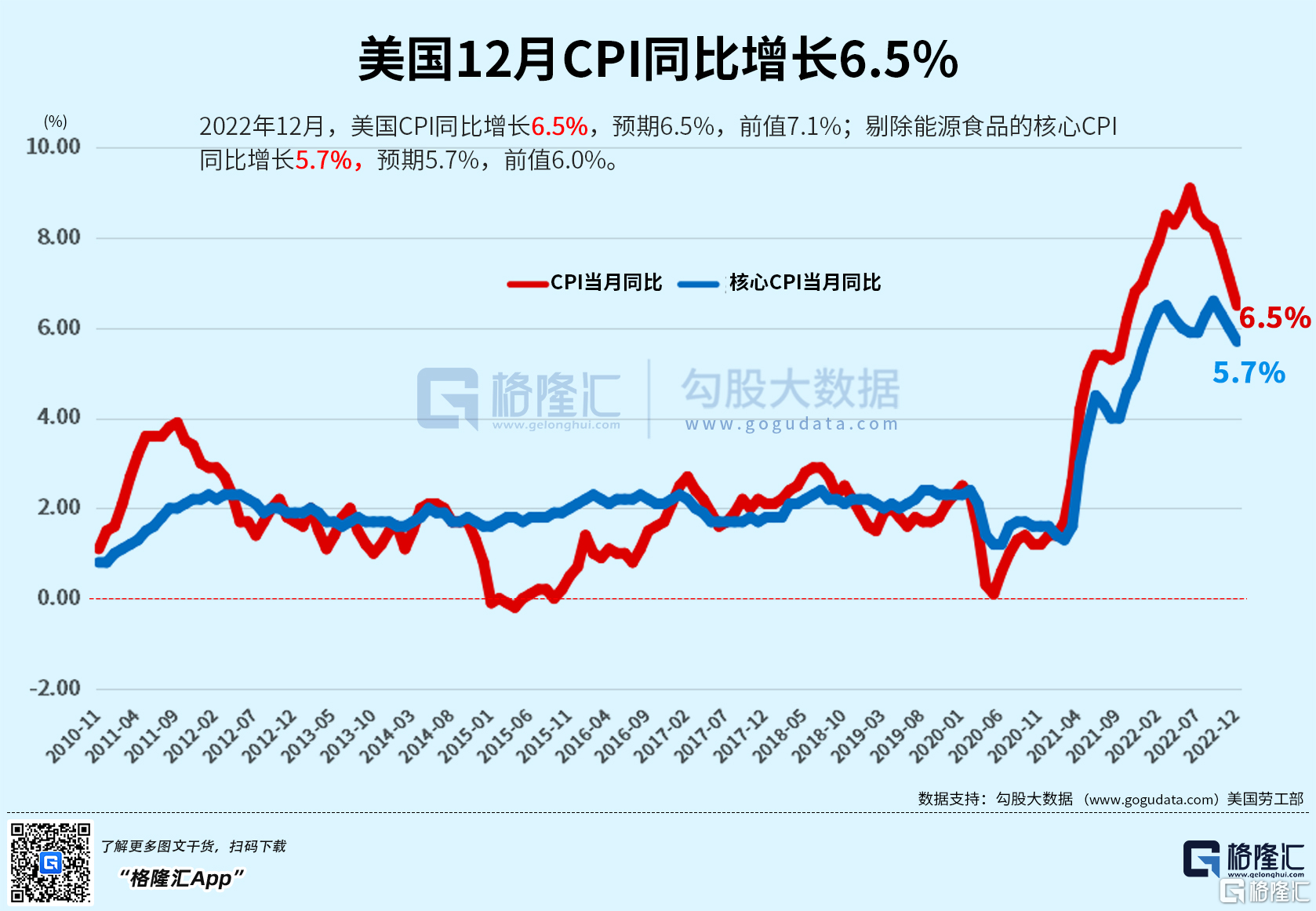

美國12月CPI同比漲6.5%,環比三年來首次轉負

北京時間週四晚21點30分,美國勞工部披露備受關注的12月CPI數據。其中名義通脹率6.5%(預期值6.5%),系2021年12月後首度跌破7%關口;被全球市場緊盯的環比增速為-0.1%(預期-0.1%),也是自2020年春天后首度出現環比下降的情況。

從具體分項來看,美國12月的通脹數據基本符合外界的觀感。引發名義CPI環比下降的主要原因是能源價格環比走弱4.5%,食品價格的環比增速也放緩至0.3%;而扣除食品、能源的核心通脹方面,環比增速0.3%(同比5.7%)也符合預期,新車和二手車的價格繼續回落。

12月份的CPI表現,再加上前幾個月的數據低於預期,表明有更加一致的跡象顯示通脹正在放緩,或許會為美聯儲在2月1日結束的下次會議上將加息幅度下調至25基點鋪平道路。話雖如此,美聯儲控制通脹的工作還遠未結束。(更多點擊閲讀)

美聯儲大鷹派稱希望儘快加息到5%以上

按照放緩加息的邏輯,如果要實現加到美聯儲此前預期的“略超5%”,意味着2月、3月和5月利率決議都要加息25個基點,才能達到5%-5.25%區間。對此美聯儲布拉德有着不同的看法。

布拉德表示,去年美聯儲採取的“前置加息”戰略很好地控制了通脹預期,今年應當延續下去。美聯儲需要避免重蹈上世紀70年代的覆轍,所以得把利率維持在足夠高的位置確保通脹下行。

布拉德進一步表示,即使在今天的CPI數據公佈之後,通脹仍然極高,通脹仍遠高於美聯儲的目標,但正在放緩。美聯儲的政策將通脹預期保持在可控範圍內。未來通脹將降至2%;美聯儲12月點陣圖顯示,2023年利率將超過5%,傾向於儘快將利率提高到5%以上。

作為本輪加息過程中異軍突起的“鷹王”,布拉德在上週的講話中出人意料得“鴿”,不僅指着美聯儲委員們的平均終值利率預期(5.1%)説足以限制經濟,還預期2023年是反通脹的一年。

美國國會或不得不在今夏解決債務限額問題以避免違約

聯邦政府正朝着31.4萬億美元的債務上限衝刺,這一上限可能在幾周內達到,為國會在債務和支出問題上的夏季攤牌做了鋪墊。

近年來,隨着聯邦支出達到歷史最高水平,國家債務不斷膨脹。超過6萬億美元的大流行病救濟金附加在政府的典型年度支出上——目前約1.7萬億美元用於可自由支配項目,約4.2萬億美元用於醫療保險、社會保障和償還國債的強制性支出。

在過去20年中,國債從喬治·W·布什上任時的約10萬億美元上升到巴拉克·奧巴馬上台時的約14萬億美元,到特朗普開始任期時的24萬億美元,以及拜登執政初期的30萬億美元。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.