本文來自格隆匯專欄:中金研究,作者:林英奇、許鴻明等

投資建議

我們預計最早2022年12月社融增速可能歷史首次下滑至10%以下,2023年全年社融增速也可能低於10%。儘管如此,我們認為這並不意味着金融對實體經濟支持力度將下降,而是由於長期經濟結構轉變導致。我們預計2023年新增貸款和社融規模分別達到22.7萬億元/33.5萬億元,分別同比多增1.4萬億元/2.5萬億元。我們預計2023年信貸結構相比2022年有所改善,基建、普惠小微、綠色貸款、製造業等領域佔比超過80%,房地產貸款佔比低於10%。總體而言,“穩增長”和“弱需求”的博弈將繼續成為主線。

理由

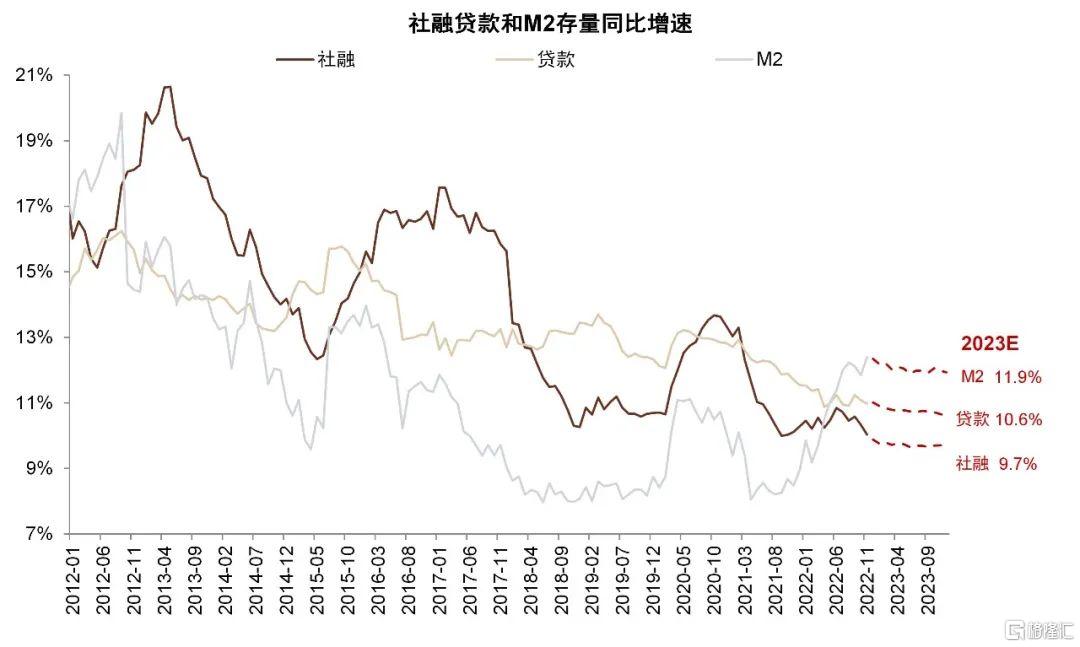

預計2023年社融增速可能首次破“10%”。中央經濟工作會議強調“穩健的貨幣政策要精準有力”,同時延續“房住不炒”和“防範化解地方政府債務風險”的原則,我們認為意味着貨幣政策更強調對實體經濟的支持,而非“大水漫灌”。在此假設下,我們預計2023年新增貸款和社融規模分別達到22.7萬億元/33.5萬億元,分別同比多增1.4萬億元/2.5萬億元,信貸和社融餘額增速分別為10.6%/9.7%,同比下滑0.4ppt/0.2ppt。結構上,預計2023年信貸結構相比2022年有所改善,基建、普惠小微、綠色貸款、製造業等領域佔比超過80%,房地產貸款佔比低於10%;預計社融增量貢獻除貸款外主要來自政府債券(增量約8萬億元)。預計社融和貸款餘額增速均將創歷史新低,其中社融增速可能首次跌破“10%”關口。

長期信貸和社融增速進入新常態。我們認為經濟結構的調整將使得長期信貸和社融增速中樞系統性下行、且波動降低,進入“新常態”。人民銀行曾在2022年二季度《貨幣政策執行報吿》專欄中對長期信貸的增速和結構進行了展望, 主要觀點包括:1) 隨着城鎮化進程和房地產週期趨緩,傳統基建和房地產等資金密集型領域信貸需求可能轉弱; 2) 綠色投資、 普惠小微、 新基建、 新型城鎮化建設,重大工程建設等在一定程度上可為信貸增長提供支撐,綠色和新基建投資可能每年貢獻投資額約 5 萬億元(我們估算約佔每年固定資產投資 10%); 3)信貸增速長期可能有所回落,但貨幣供應量和社會融資規模增速同名義經濟增速仍將保持基本匹配。對於銀行而言,可能體現為長期貸款增速穩中略降、淨息差略有收窄但信用成本節約、盈利總體穩健。

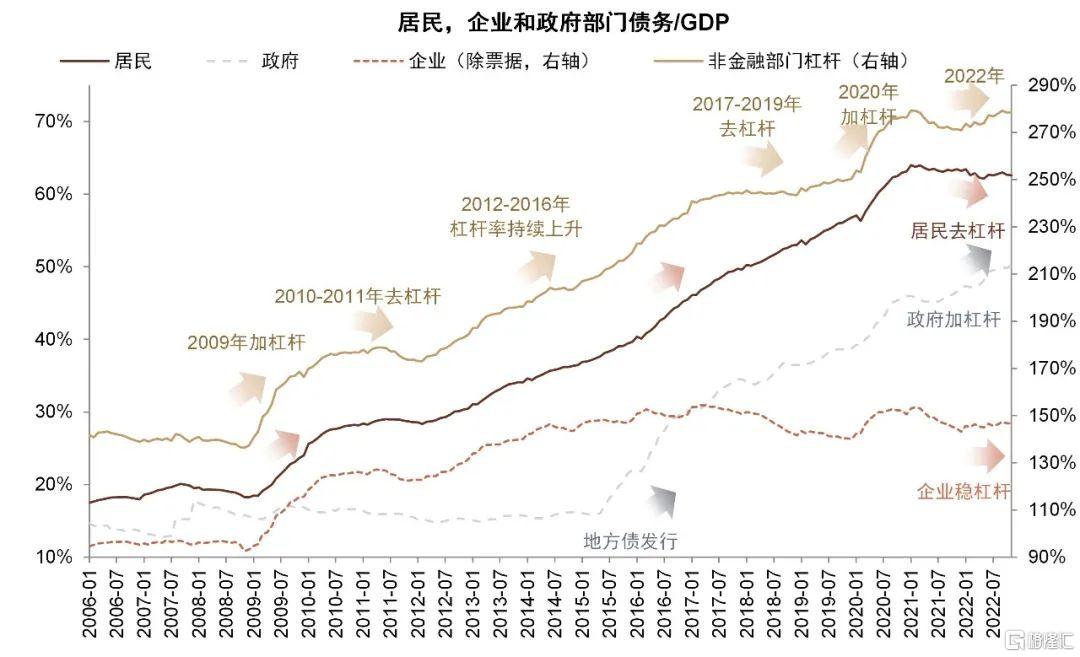

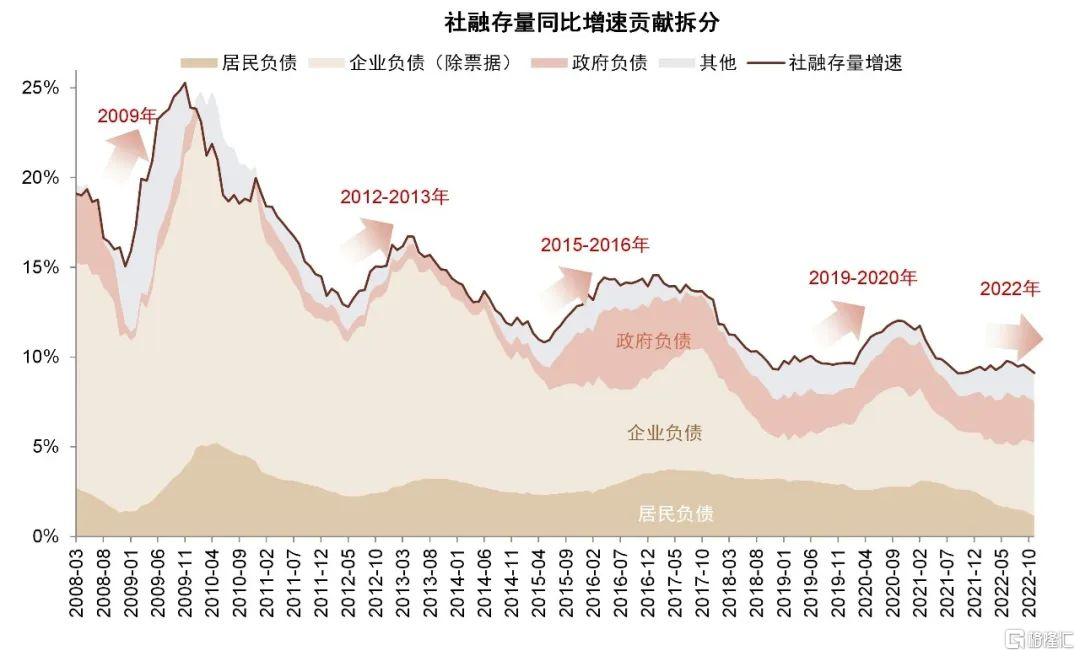

預計居民部門去槓桿趨勢延續。我們預計居民部門負債可能仍然是社融和貸款的主要拖累因素,中金地產組預計房地產市場或呈“緩築底、慢復甦”態勢, 2023年銷售面積和金額同比或由負轉正至 1.9%和 5.2%。在此假設下,我們預計居民按揭貸款增速2023年仍為4%的低位,居民部門債務/GDP全年下降2ppt,延續去槓桿趨勢。企業部門方面,預計基建項目落地將繼續推動基建貸款和企業中長期貸款增速回升,綠色貸款、普惠小微、高技術製造業仍是投放重點,加槓桿主體以國有企業為主;政府部門方面,考慮到經濟工作會議仍然強調“保障財政可持續和地方政府債務風險可控”,預計2023年政府債務增速與2022年基本持平(約13%),但仍是社融中增速最快的項目。

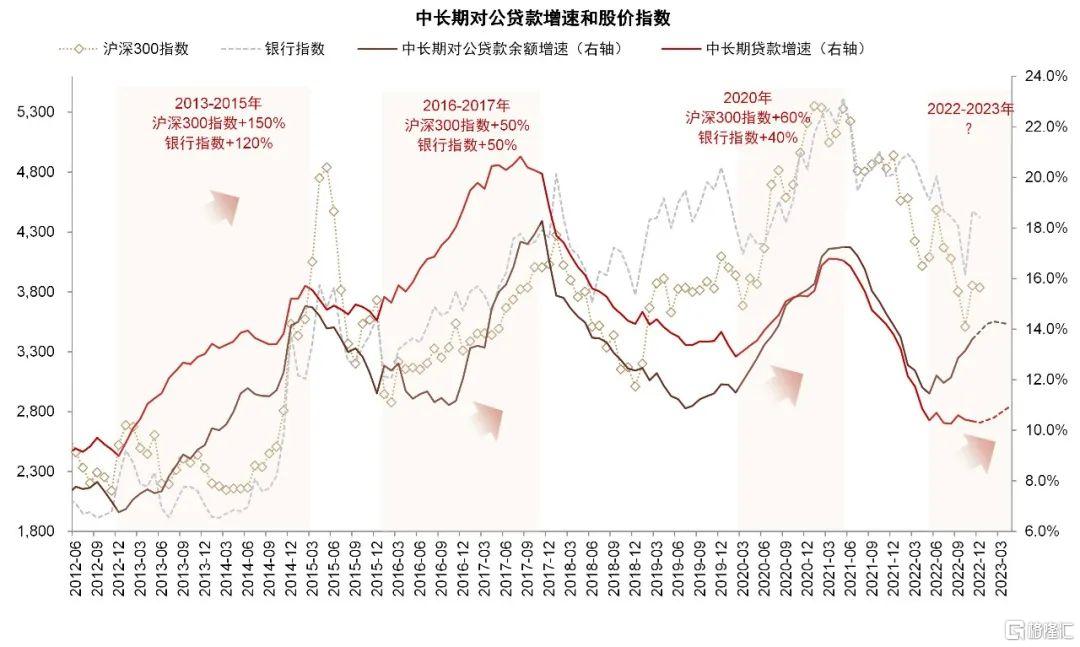

關注信貸需求實質性改善拐點。總體而言,我們預計2023年總體信貸需求仍然偏弱,“穩增長”政策和“弱需求”的博弈將繼續成為明年主線。歷史經驗表明信貸需求的實質改善往往也是股價的重要催化劑,我們建議關注以下信號來判斷信貸需求實質性拐點,從而動態調整對社融和信貸的預期:1)房地產市場銷售和拿地情況;2)基建項目是否加碼;3)居民消費需求恢復情況;4)非國有企業投資需求,等等。

風險:疫情反覆,經濟下行,房地產風險繼續擴散。

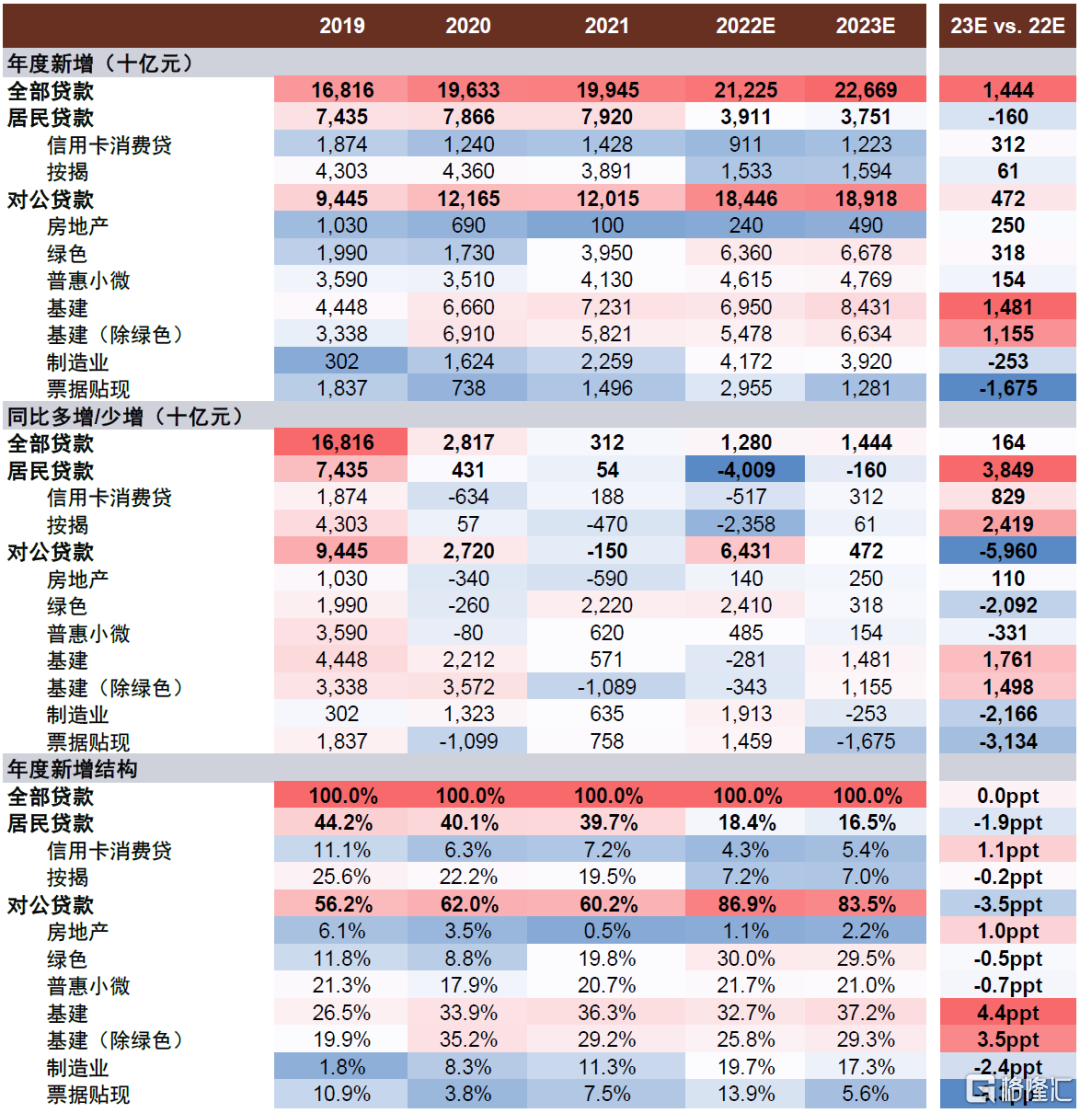

圖表1:人民幣貸款預測:增量及結構

資料來源:Wind,中金公司研究部

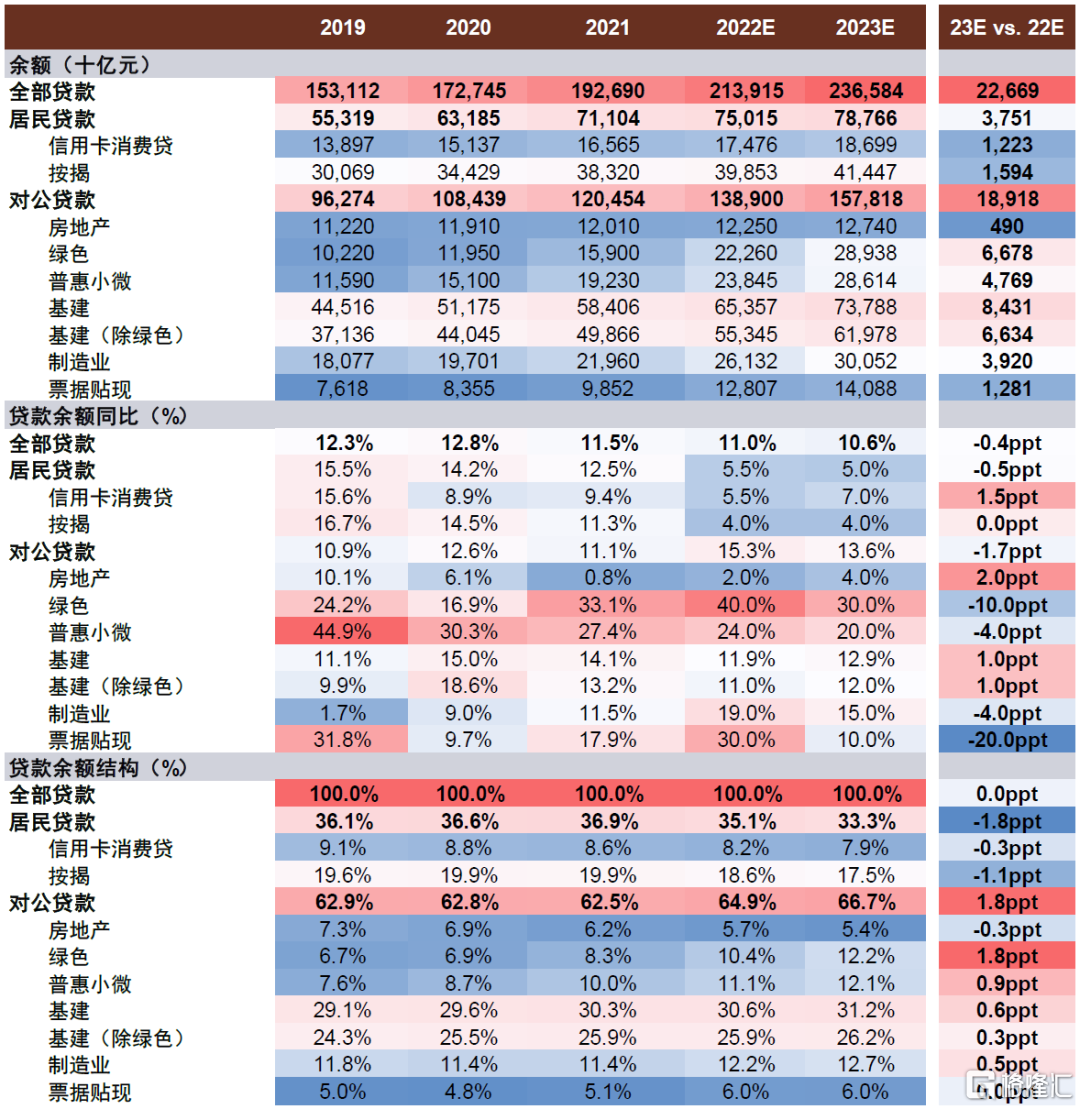

圖表2:人民幣貸款預測:存量及結構

資料來源:Wind,中金公司研究部

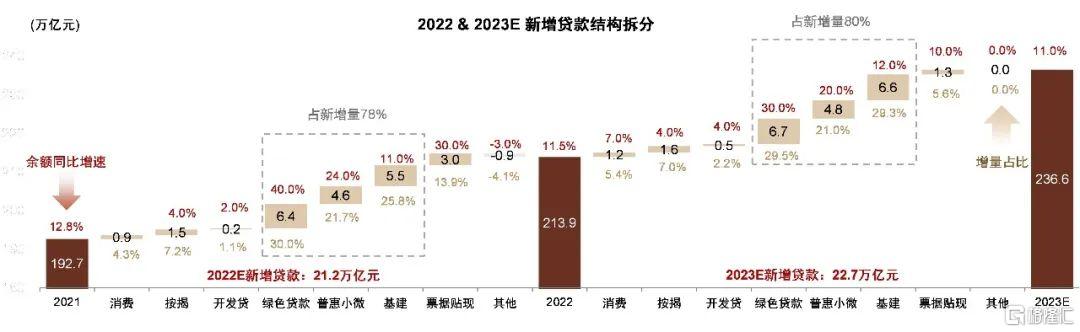

圖表3:2022&2023E新增貸款結構拆分

資料來源:Wind,中金公司研究部

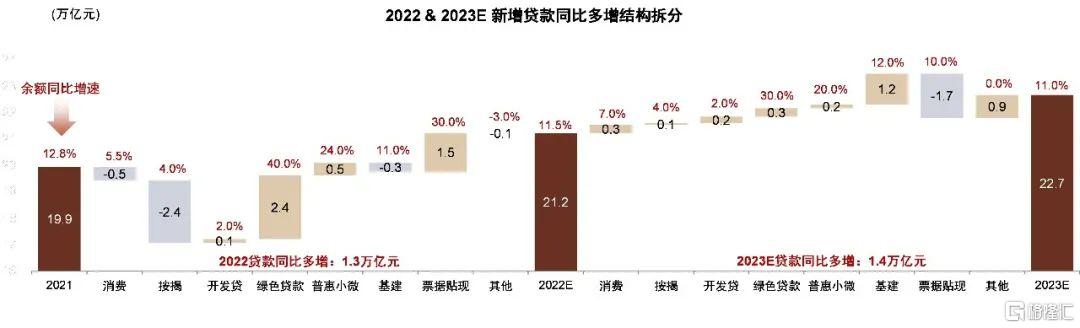

圖表4:2022&2023E新增貸款結構同比多增結構拆分

資料來源:Wind,中金公司研究部

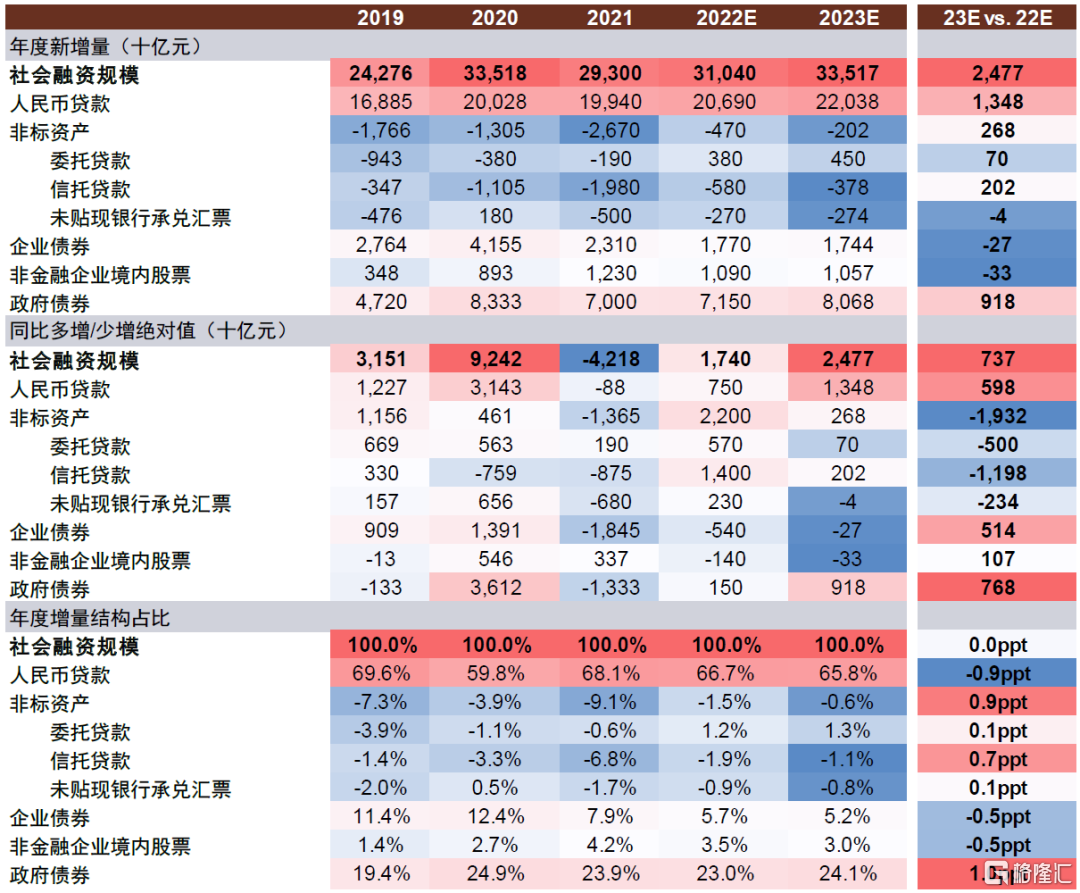

圖表5:社會融資規模預測:增量及結構

資料來源:Wind,中金公司研究部

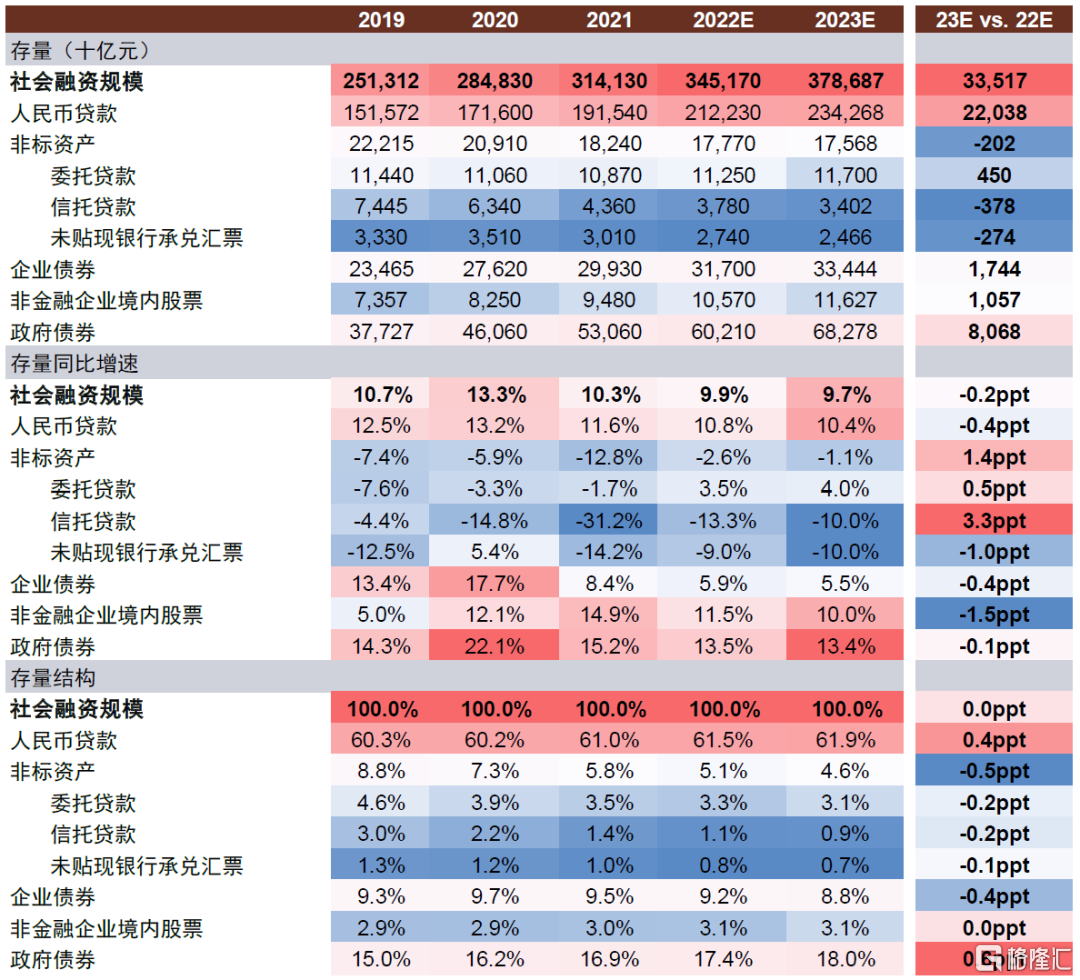

圖表6:社會融資規模預測:存量及結構

資料來源:Wind,中金公司研究部

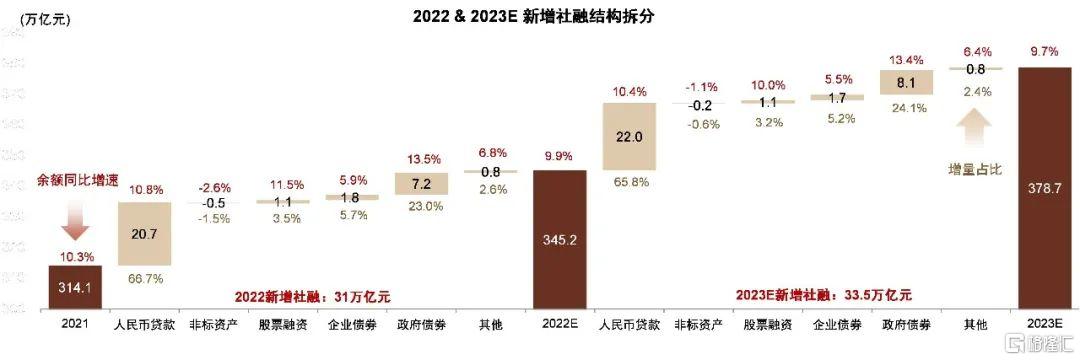

圖表7:2022&2023E新增社融結構拆分

資料來源:Wind,中金公司研究部

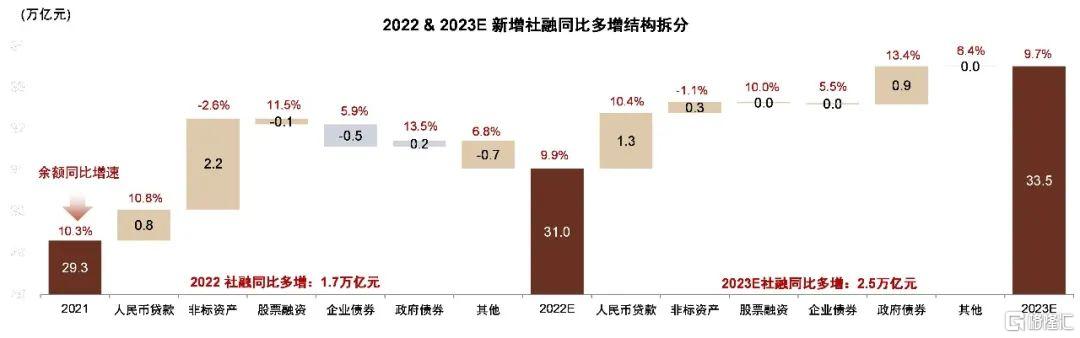

圖表8:2022&2023E新增社融同比多增結構拆分

資料來源:Wind,中金公司研究部

圖表9:社融貸款和M2存量同比增速

資料來源:Wind,中金公司研究部

圖表10:預計2023年居民部門延續去槓桿趨勢,政府和企業部門繼續加槓桿

資料來源:Wind,中金公司研究部

圖表11:預計2023年居民部門負債增速仍然較低

資料來源:Wind,中金公司研究部

圖表12:預計2023年居民部門仍是社融增速主要拖累

資料來源:Wind,中金公司研究部

圖表13:預計居民中長期貸款增速對全部中長期貸款增速形成拖累,總體信貸需求弱復甦

資料來源:Wind,中金公司研究部

More Content