如何理解近期金融支持房地產“組合拳”?

本文來自格隆匯專欄:中金研究,作者: 嚴佳卉 侯德凱等

11月8日以來,一系列金融支持優質房地產企業融資的政策接連出台,我們預計銀行在支持對象的選擇上可能仍然相對審慎,但好於此前的保守態度,市場對優質房企敞口資產質量擔憂的緩解有利於銀行估值修復。

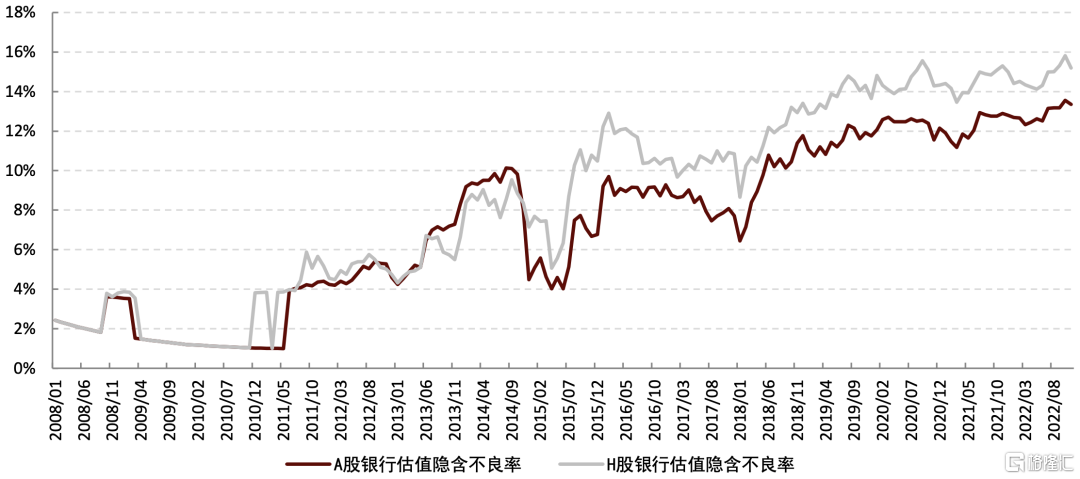

金融支持優質房企融資的政策組合拳有利於銀行估值修復。截至11月14日,A股和H股銀行估值隱含不良率為13.4%和15.2%,處於歷史高位,其中包括了市場對疫情衝擊、地產風險等諸多負面因素的擔憂。近期一系列支持優質房企融資的金融政策出台後,我們預計市場對銀行房地產敞口的資產質量擔憂可能有所緩解,推動銀行估值修復。具體而言:

► 11月8日,中國銀行間交易商協會公吿推進並擴大“第二支箭”,由人民銀行再貸款提供資金支持,委託專業機構按照市場化、法治化原則,通過擔保增信、創設信用風險緩釋憑證、直接購買債券等方式,支持包括房地產企業在內的民營企業發債融資。預計可支持約2500億元民營企業債券融資,後續可視情況進一步擴容。

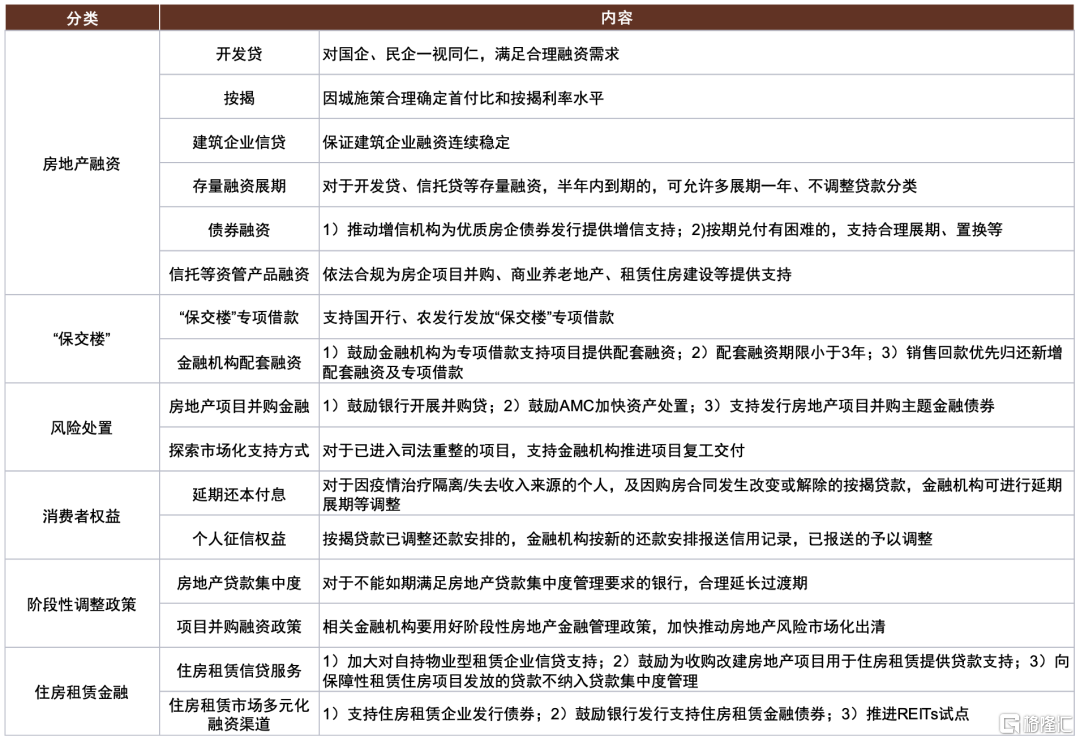

► 11月13日,“金融十六條”出台以支持優質房地產企業融資,包括支持房開貸及信託貸款等存量融資合理展期(未來半年內到期的,可以允許超出原規定多展期1年,可不調整貸款分類,報送徵信系統的貸款分類與之保持一致)、積極做好保交樓金融服務(鼓勵提供配套融資支持,明確後進先出、盡職免責的細則)、階段性調整部分金融管理政策(延長房地產貸款集中度管理政策過渡期安排)等。

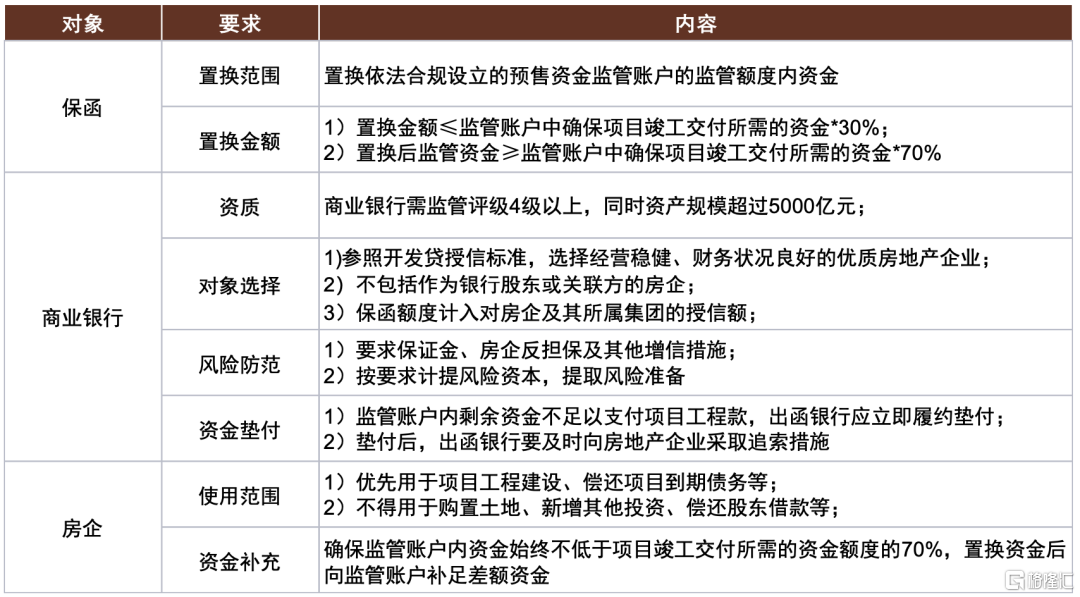

► 11月14日,銀保監“保函置換通知”允許房地產企業在預售資金監管賬户內資金達到規定額度後,向商業銀行申請出具保函置換監管額度內資金,保函置換金額不得超過監管賬户中確保項目竣工交付所需的資金額度的30%,置換後的監管資金不得低於監管賬户中確保項目竣工交付所需的資金額度的70%。商業銀行需按市場化法治化原則自主決策,可提出增信要求,需要計提風險資本、提取風險準備。

► 考慮到上述金融政策仍多次強調市場化法治化原則,我們預計銀行在支持對象的選擇上可能仍然相對審慎,但好於此前的保守態度,資金可能傾向於提供給安全的國央企,或者有存量業務敞口的民營房地產企業,以保障存量信用敞口的資產質量或降低損失率。

我們預計銀行內部分化趨勢仍會延續,風控能力和資產質量依然是選股關鍵。由於上述金融政策中多次強調“與優質房地產企業開展業務”、“支持治理完善、聚焦主業、資質良好的房地產企業”,我們預計政策目的是致力於解決優質房地產企業的流動性問題,而非出險房地產企業的資不抵債問題,因此各家銀行的房地產信用敞口是否會發生損失、損失率在多少,仍然考驗銀行的風險定價能力。

圖表1:金融支持房地產十六條通知主要內容

資料來源:中國人民銀行,中國基金網,中金公司研究部

圖表2:2022年和2018年民企債券支持工具對比

資料來源:中國人民銀行,中金公司研究部

圖表3:《關於商業銀行出具保函置換預售監管資金有關工作的通知》主要內容

資料來源:中國銀保監會,中金公司研究部

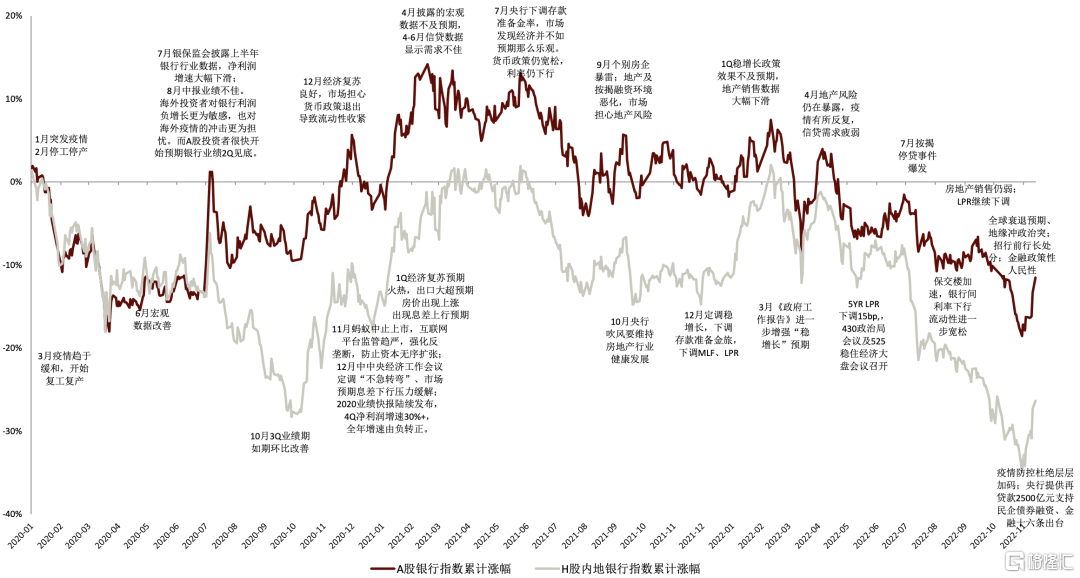

圖表4:銀行股指數覆盤

資料來源:Wind,中金公司研究部

圖表5:A股和H股銀行估值隱含不良率處於13%和15%的歷史高位

資料來源:Wind,中金公司研究部

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.