本文來自格隆匯專欄: 梁中華宏觀研究,作者:梁中華、李俊

· 概 要 ·

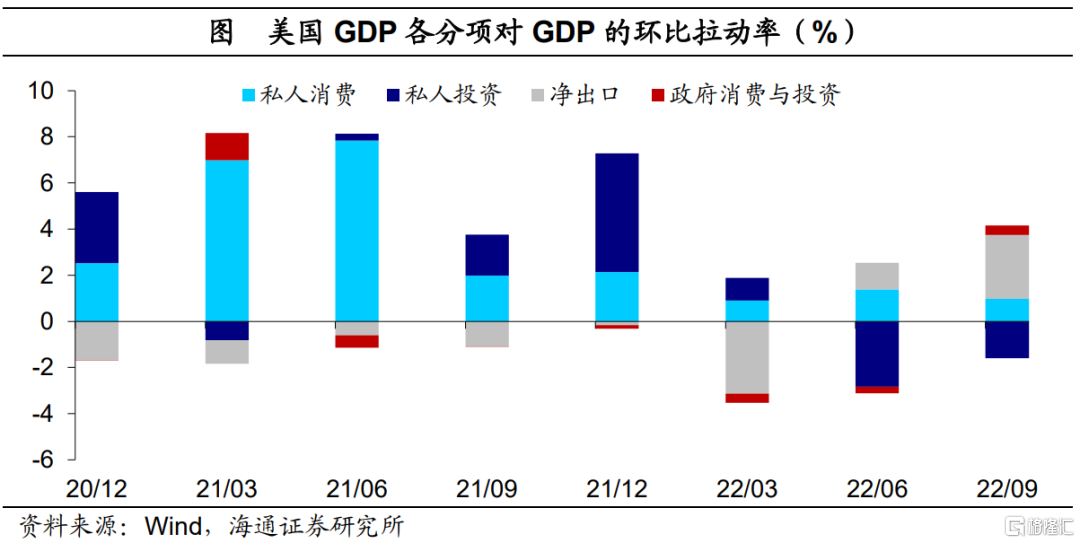

美國經濟明顯回升。美國2022年3季度GDP環比折年率回升至2.6%,較2季度明顯回升。從結構來看,淨出口是最大貢獻,淨出口的貢獻來自於進口的明顯回落,或難以持續。投資是最大拖累,尤其是住宅投資,或與美聯儲持續加息有關。私人消費貢獻有所走弱,不過服務消費貢獻仍強,剔除基數,商品消費和服務消費增速均高於疫情前,消費整體不差。

美聯儲或難放緩加息。當前美國勞動力市場表現強勁,失業率維持歷史低位,生產和消費也仍有一定韌性,我們認為美國經濟有韌性。美國當前的核心矛盾依然是通脹,也是美聯儲的主要目標。在核心通脹沒有明顯回落跡象的背景下,我們認為,美聯儲或難放緩加息。

美國3季度GDP環比增速扭負轉正。2022年10月27日,美國公佈了2022年3季度經濟數據初值,其中3季度GDP不變價環比折年率為2.6%,較2季度的-0.6%明顯回升。

從結構上來看,淨出口貢獻最大。3季度美國商品和服務淨出口對GDP環比的拉動由2季度的1.2%上升至2.8%,創1980年3季度以來的新高。淨出口拉動上升主要是與美國出口維持強勁,而進口大幅回落有關。

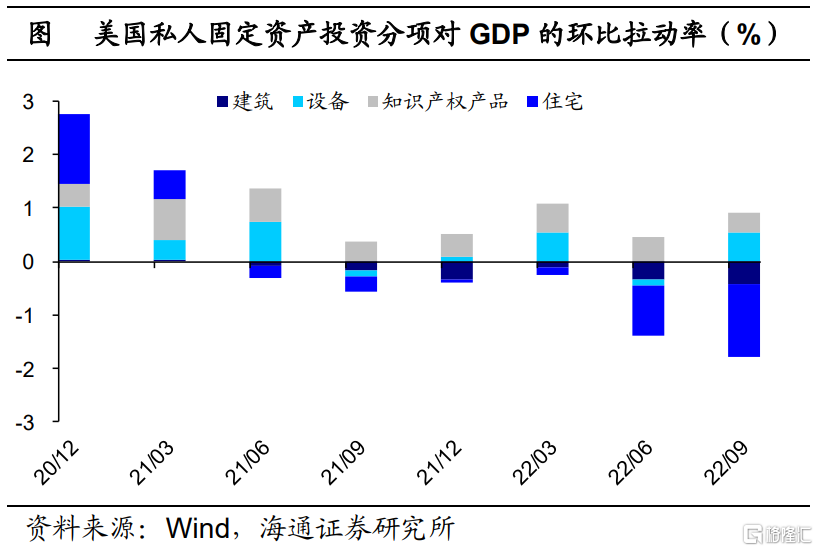

私人投資仍是最大拖累。3季度美國私人投資對GDP環比拉動為-1.6%,連續2個季度為負,是主要的拖累項。而3季度美國個人消費支出對GDP環比的拉動放緩至1.0%,但依然是正貢獻;政府消費與投資的貢獻由負轉正,為去年1季度以來首次轉正,對GDP貢獻較大。

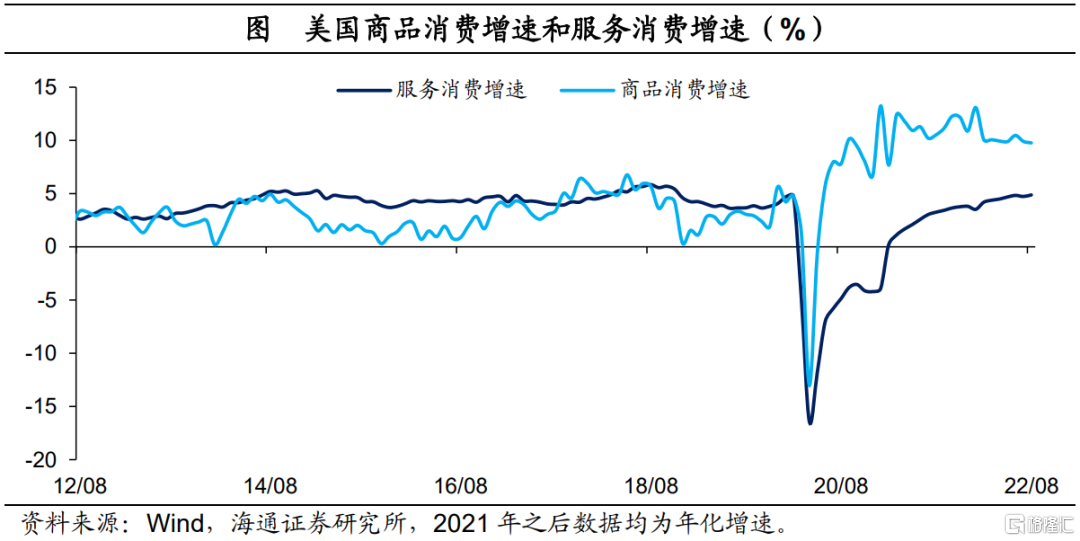

從消費角度來看,延續商品弱、服務強的趨勢。3季度美國個人消費支出環比折年率從2季度的2.0%回落至1.4%。其中,商品消費環比折年率連續3個季度為負,是消費的主要拖累;不過降幅較2季度明顯收窄,尤其是耐用品消費收窄幅度更大。服務消費環比折年率為2.8%,是消費的主要貢獻,儘管較2季度明顯收窄,但依然高於疫情前幾年的平均水平(2020年3月前)。

如果剔除基數,消費並不差。近期消費整體的回落,一定程度上與美聯儲持續加息有關;另一方面,也與基數影響有關。如果我們剔除基數影響,會發現消費整體依然不差,商品消費從高點回落,但仍在高位;而服務消費仍保持上行趨勢。

從投資來看,住宅投資是最大拖累。3季度美國住宅投資環比年化增速的降幅由2季度的-17.8%擴大至-28.4%,連續6個季度為負,拖累GDP環比增速1.4個百分點。住宅投資的下行或與美聯儲持續加息有關,當前(10月27日)美國30年期房貸利率已上升至7.08%,為2002年4月以來新高,新房與成屋銷售同比增速也持續下滑。

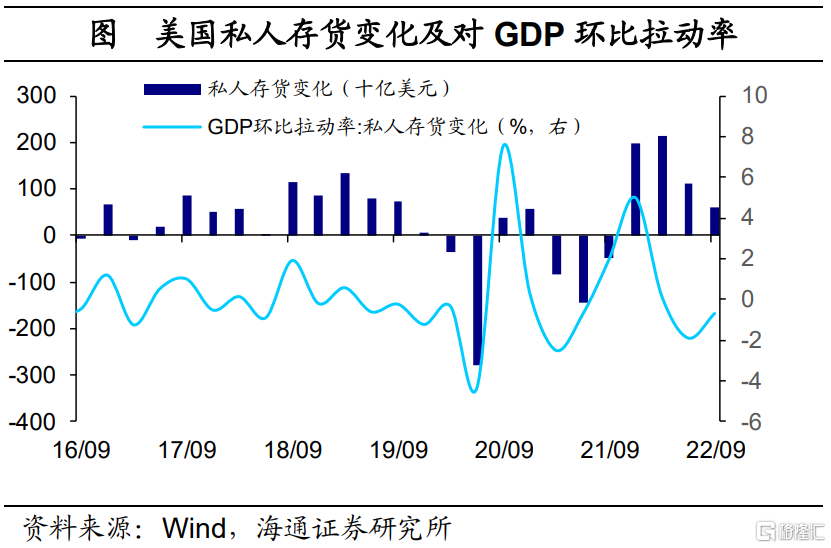

庫存投資仍處低位。美國經濟分析局3季度經濟數據報吿指出,受零售貿易下降影響,廠商補庫速度減弱,庫存投資年化環比增速為-90.1%,拖累經濟增長0.7個百分點。此外,9月美國耐用品訂單環比為0.4%,但扣除飛機和國防後的資本耐用品訂單環比僅為-0.7%,商品消費需求現疲軟態勢。

企業投資有所回暖。反映企業投資的非住投資年化環比增速由2季度的0.1%上升至3.7%,其中建築投資年化環比增速連續6個季度處於負區間,而設備投資增速由-2.1%大幅改善至10.8%。

從外貿來看,出口強、進口弱。3季度美國進口年化增速由2.3%下降至-6.9%,其中日用消費品的進口下滑較為明顯,或與美國國內商品消費持續走弱有關。

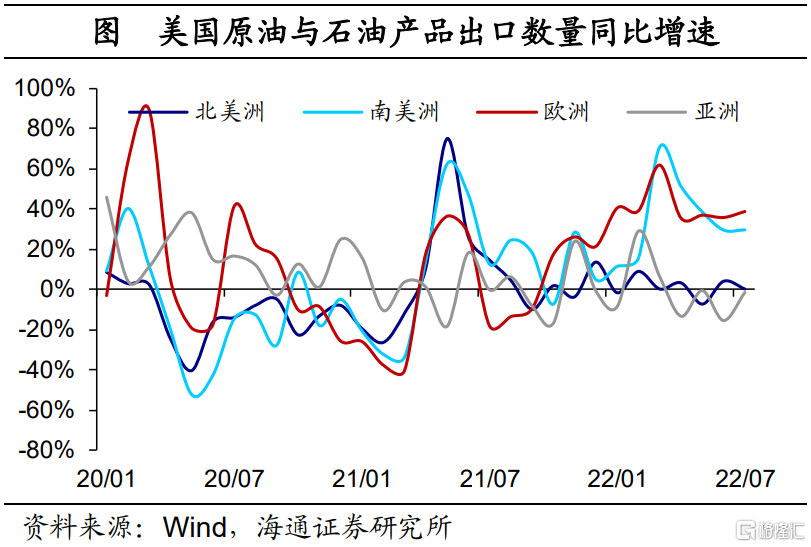

而出口年化環比增速則由2季度的13.8%提升至14.4%,連續2個季度保持高增長,尤其是商品出口增速較高。其中,工業用品和材料(特別是石油和產品以及其他非耐用品)以及非汽車資本貨物的出口貢獻最大。

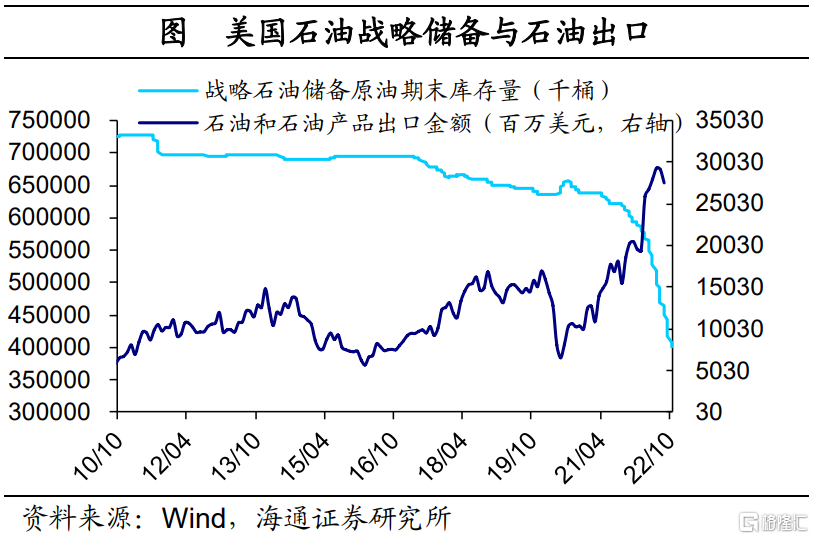

石油出口強勁或與國際石油短缺和美國釋放戰略石油儲備有關。一方面,在地緣衝突下國際能源供應緊張,美國向歐洲出口的石油數量有所上升;另一方面,為緩解高油價問題,3月美國宣佈未來六個月將從美國戰略石油儲備中每天釋放100萬桶石油、累計釋放1.8億桶,或也一定程度上推高了石油出口。

但當前美國國內原油與石油庫存已下降至低位,未來石油出口或面臨一定的回落壓力,淨出口對美國GDP貢獻的可持續性仍待觀察。

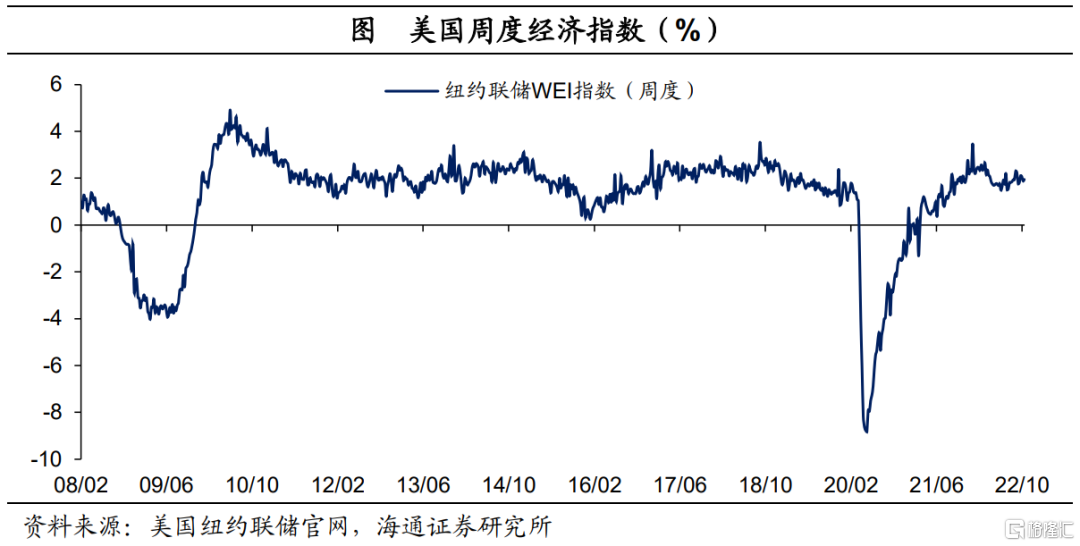

美國經濟仍有韌性。儘管在貨幣政策的持續收緊下,高通脹和高利率的環境對經濟的總量產生了一定的影響,但當前美國就業依然強勁,失業率仍保持在歷史低位;居民可支配收入增速仍維持高位,為消費韌性提供支撐;加之,美國生產仍較為強勁。我們認為美國經濟短期仍有韌性。例如,10月中旬,美國周度經濟指數年化增速仍在2.0%附近,仍好於疫情前水平。

美聯儲或難放緩加息。美國當前經濟仍有韌性,高通脹仍是當前的核心矛盾,美聯儲的目標依然是解決通脹問題。在核心通脹沒有明顯回落跡象的背景下,我們認為,美聯儲或難放緩加息。

More Content