本文來自格隆匯專欄:宏觀芝道,作者:周君芝 譚浩弘

導讀

6月美國通脹增速再度高於市場預期。非常時期下,美聯儲或將“非常加息”。投資者需關注7月美聯儲單次加息100BP的風險。

要點

6月美國總體CPI和核心CPI增速均超過市場預期。美國6月CPI同比增速+9.1%,預期+8.8%;核心CPI同比+5.9%,預期+5.7%。

本次通脹數據顯示美國正經歷嚴重的物價普漲,通脹壓力巨大。

近期汽油和天然氣等能源價格均有所回落,市場預期美國通脹增速或將在6月見頂。疊加投資者對美國經濟衰退的擔憂,長端美債利率當晚反而收跌。

我們認為,在汽車和租金通脹的帶動下,美國核心通脹或將在3季度重新上行。這意味着,未來美國總體通脹隨能源價格回落的同時,核心通脹或將接力反彈,美國高通脹擔憂難解。

面對極其頑固的高通脹環境,美聯儲或將深化“前置加息”策略, 7月有可能加息100BP。

正文

7月13日,6月美國總體CPI和核心CPI增速均超過市場預期。美國6月CPI同比增速+9.1%,預期+8.8%;核心CPI同比+5.9%,預期+5.7%。

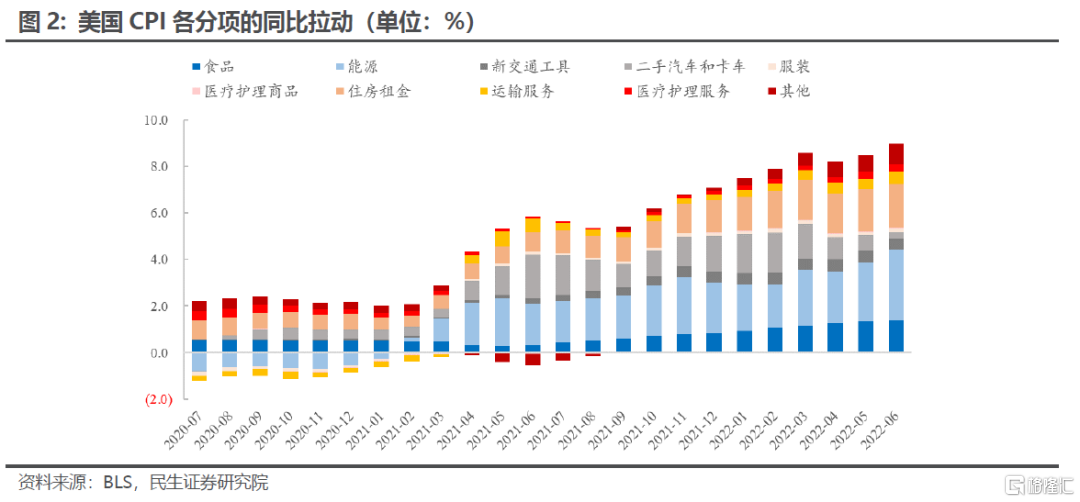

一、CPI分項顯示6月美國仍經歷較為廣泛的物價普漲

與5月份類似,6月美國各CPI分項均環比擴張。

非核心通脹方面,食品通脹環比小幅回落,能源價格全面上行。

食品分項CPI環比從5月的1.2%小幅至1.0%。受供應鏈和種植成本影響,食品通脹總體仍高企。能源方面,美國夏季出行需求增加,汽油價格6月一度觸及5美金/加侖的高位。美國CPI能源分項環比從5月的3.9%進一步上行至6月的7.5%。

核心通脹方面,除汽車通脹環比增速小幅回落,其餘分項升勢不減。

2022年6月,美國CPI新車和二手車分項環比分別錄得0.7%和1.6%,較5月的1.0和1.8%小幅下降。但6月份服裝(0.8%)、醫療服務(0.7%)、運輸服務(2.1%)等環比均較5月上行,權重最大的租金分項環比增速則為0.6%,與上月持平。

二、美國通脹見頂了麼?目前暫且不能太樂觀

7月份開始,美國汽油和天然氣價格均從高位有所回落了,美國能源項CPI同比有望在6月見頂。故市場目前有預期6月美國通脹見頂。

然而未來二手車價格同比或上行,汽車需求或仍待釋放,美國通脹還有驅動力。二手車價格因基數效應回落,壓制了2季度美國核心通脹。但進入3季度,二手車通脹將迎來低基數,這意味着同比增速或將反彈。二手車通脹的前瞻指標Manhiem二手車價格指數的同比增速已經出現止跌跡象。2022年4月,美國機動車與零部件零售庫銷比為1.28%,處於絕對低位。同時,6月中國對美汽車出口數量同比亦反彈。這反映美國汽車需求仍有韌性,制約需求的是供給不足。

房租通脹仍“如鯁在喉”,年內回落概率不高,仍驅動通脹上行。住房租金主要受兩大因素影響,房價和居民收入。美國房價增速通常領先租金1-2年,當前美國房價仍處於歷史最高水平,疊加同樣高企的工資增速,年內美國租金通脹恐繼續上行。

這意味着,未來美國總體通脹隨能源價格回落的同時,核心通脹或將接力反彈,美國高通脹擔憂難解。

三、非常時刻非常加息,7月會議100BP加息正在醖釀

三重因素疊加,美債長端利率在通脹“爆表”之夜不漲反跌。CPI數據公佈後,10年期美債利率短暫衝高,但最終收跌4BP至2.94%。這與三個因素有關,一是市場預期通脹將在6月見頂;二是經濟衰退的擔憂;三是成功“預測”美聯儲6月加息75BP的華爾街日報記者Nick Timiraos撰文表示美聯儲7月或加息75BP。

面對頑固通脹,美聯儲7月加息100BP的概率正不斷提高。5月和6月分別加息50和75BP後,美國通脹依然高燒難退。美聯儲當務之急是讓通脹環比增速掉頭,這意味着美聯儲或將深化“前置加息”策略, 7月有可能加息100BP。聯邦基金期貨顯示,當前市場定價7月加息100BP,概率已經升至82%。

另外,美聯儲內部或正醖釀修改政策框架,時機在8月的JacksonHole會議。通脹擔憂持續導致美國政策環境高度不確定,美債利率同樣難言見頂。

風險提示

海外央行加息節奏超預期;海外地緣政治風險;美國通脹失控風險。

More Content