阿里雲13年來首次盈利,中美雲計算走出差異行情

5月26日晚,阿里巴巴披露2022財年年報,阿里雲EBITA利潤從去年的虧損22.51億元大幅改善為今年的盈利11.46億元,苦守13年終於實現全年盈利。

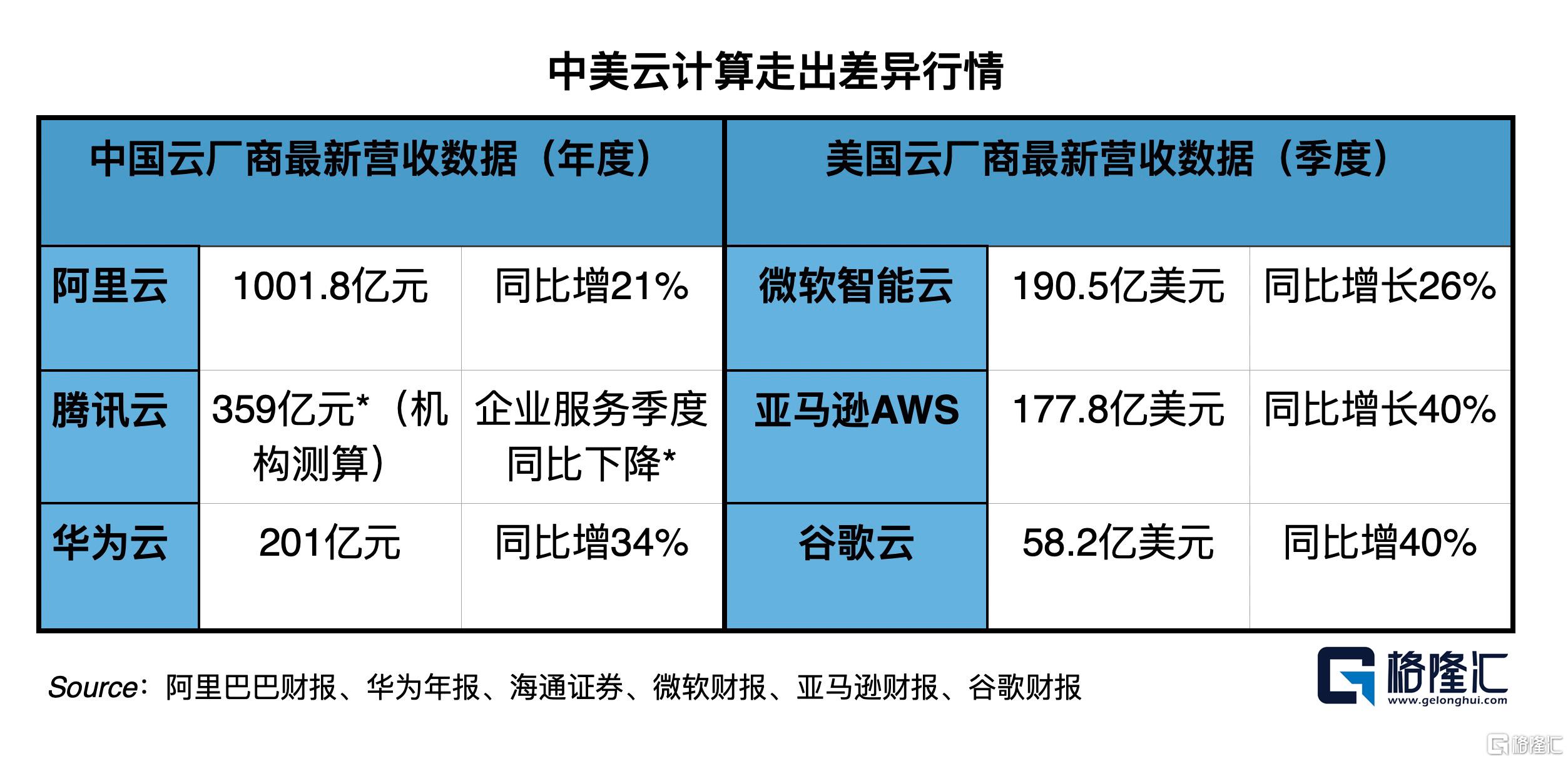

收入方面,阿里雲收入規模跨過1000億大關,財報披露其全年收入在扣除跨分部交易前為1001.8億元,同比增長21%。扣除後為745.68億元,同比增長23%。

截止目前,中國三朵雲、美國三朵雲均發佈了財報。對比中國三朵雲業務數據,中國雲計算行業出現普遍放緩,阿里雲在規模數倍於其他雲廠商的前提下,依舊實現不錯增長。但看向全球市場,中國雲增長普遍遜於美國廠商,中美雲計算走出差異行情。

具體來看,騰訊已經多個季度未單獨披露雲計算營收,最新財報中披露包括雲計算在內的企業服務收入出現同比略有下降。據海通證券估算,2021年騰訊雲總收入達359億元。

3月,華為在年報中披露2021全年雲業務營收為201億元,增速為34%。此外,在美股上市的金山雲披露2021年營收90億元,同比增長38%。

美國廠商業績普遍較強。亞馬遜在最新季度實現了40%的增速,季度收入177.8億美元。前兩年,AWS營收層一度下跌至30%以下,但自2021年開始,受到疫情後數字化需求帶動,AWS增速逐步回暖,至最新季度達到40%。

微軟智能雲增速26%,季度營收190.5億美元。谷歌雲在體量小於前兩者的情況下,增速雖較此前的5字頭有所收縮,但也達到40%。

從數據看,中美雲計算廠商走出了差異行情。過去數年間,中國雲廠商增長基本數倍於美國雲廠商,情況在去年開始出現反轉。分析認識認為,中美IT市場的成熟度有別,產業差距也一直存在,例如在軟件行業,全國35家上市公司的營收、市值、利潤綜合指標僅為微軟的3.5%——由此來看,中國雲廠商與美國雲廠商的差距已經不算過分,在Gartner最新發布的2021年全球雲計算市場數據中,前六名中美各佔三家,可以説是差距正在縮小中。

迴歸基本盤看,中國雲廠商在技術能力上與美國廠商十分接近,甚至部分領域能實現並駕齊驅和領先。例如阿里雲的自研飛天操作系統能夠實現從芯片到操作系統、大數據的全棧自研,技術水平在全球一直處於前列。在Gartner、Forrester等權威機構的評估中,阿里雲甚至能在部分領域拿下最高分,騰訊、華為技術也在進入榜單前列。

從佈局來看,當前,中國雲廠商仍在研發、佈局上持續投入。阿里財報中披露,去年的研發投入達到1200億元,可以推想,這其中大部分是用於雲計算的技術研發。自研芯片、服務器、計算架構等算力領域的技術突破,也可視為上述投入的可見成果。

同時,幾家雲廠商也在加速全球化的佈局,阿里雲近期新增了德國、泰國的幾座數據中心,騰訊雲去年也在印尼啟動了首個數據中心。近年來,中國雲廠商正在東南亞各個國家紮根,馬來西亞、泰國、印尼等國家,中國雲廠商份額都已超過30%,且再持續增長。在這些國家市場日漸紮根,也將為中國雲廠商帶來新的增量。

值此時刻,不應以過激情緒動搖市場信心,對中國雲企業進一步唱衰、施壓,而應給予一定耐心和信心。雲計算的發展與IT市場整體環境息息相關,與美國更為成熟的IT市場條件相比,中國數字化市場還在發展中,許多數字化轉型項目還需要通過"堆人力"的項目制完成,在當前階段,增速下滑也並非意外。

但長期來看,數字經濟是大勢所趨,傳統企業正在加速上雲。中國雲廠商在持續技術投入的同時,也在探索合作、被集成、PaaS新界面等針對中國IT市場特色的新模式。

加以時日,隨着數字化轉型速度加快,自動駕駛、XR等新興高算力市場出現,中國雲廠商的發展勢必出現回暖,不僅能縮小與美國廠商的產業差距,也將走出獨特的雲計算模式。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.