惠程科技:商譽暴雷後,還有預付款存疑

格隆匯 08-25 09:28

作者 | 晨光

數據支持 | 勾股大數據(www.gogudata.com)

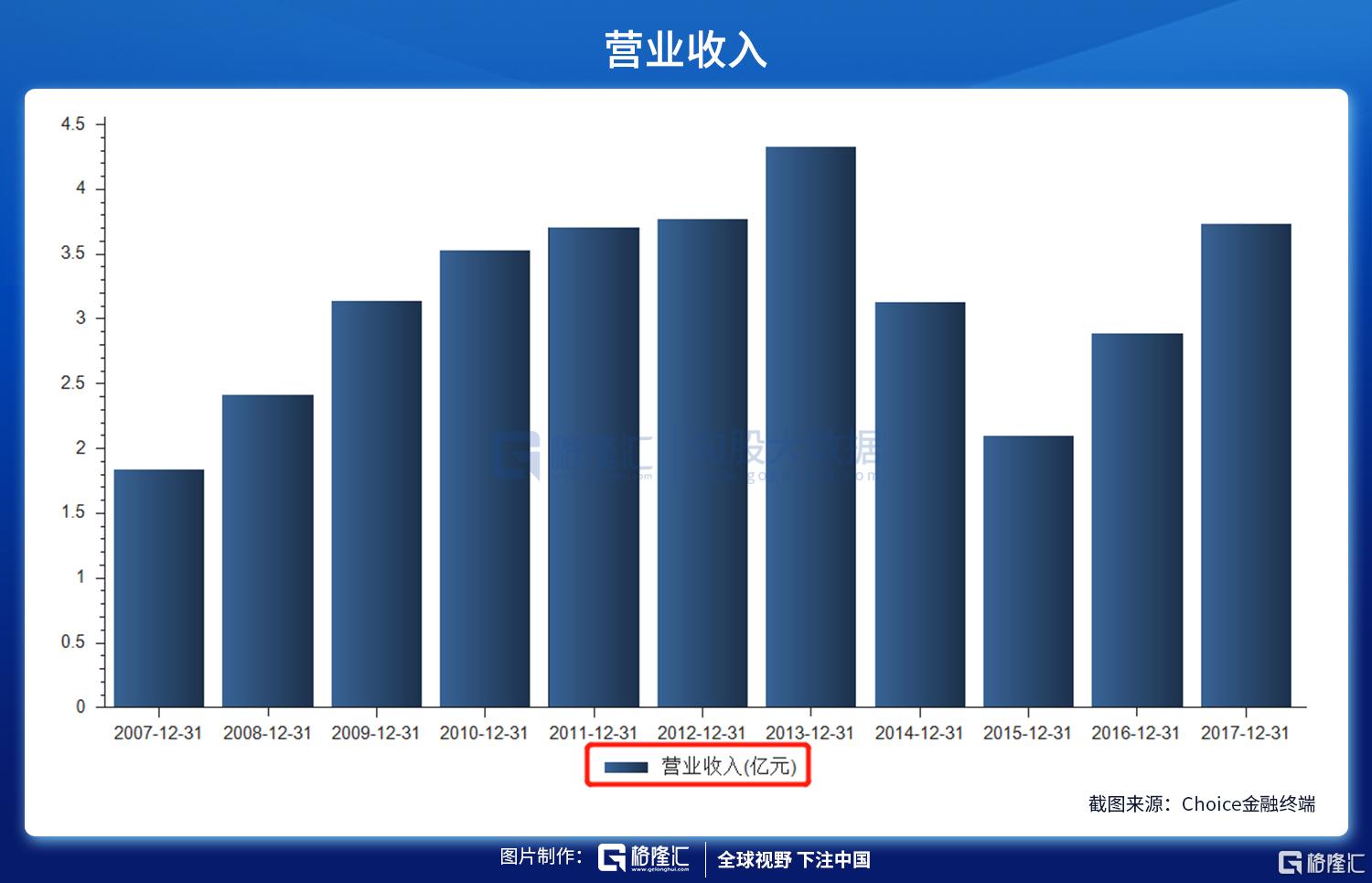

2007年9月,惠程科技登陸深交所,主營電纜分支箱類產品、硅橡膠絕緣製品、複合材料絕緣製品等主要用於城鄉電網改造與建設。上市十年(07年至17年)其營收一直不温不火,常年維持在1.8億元至4.3億元之間。

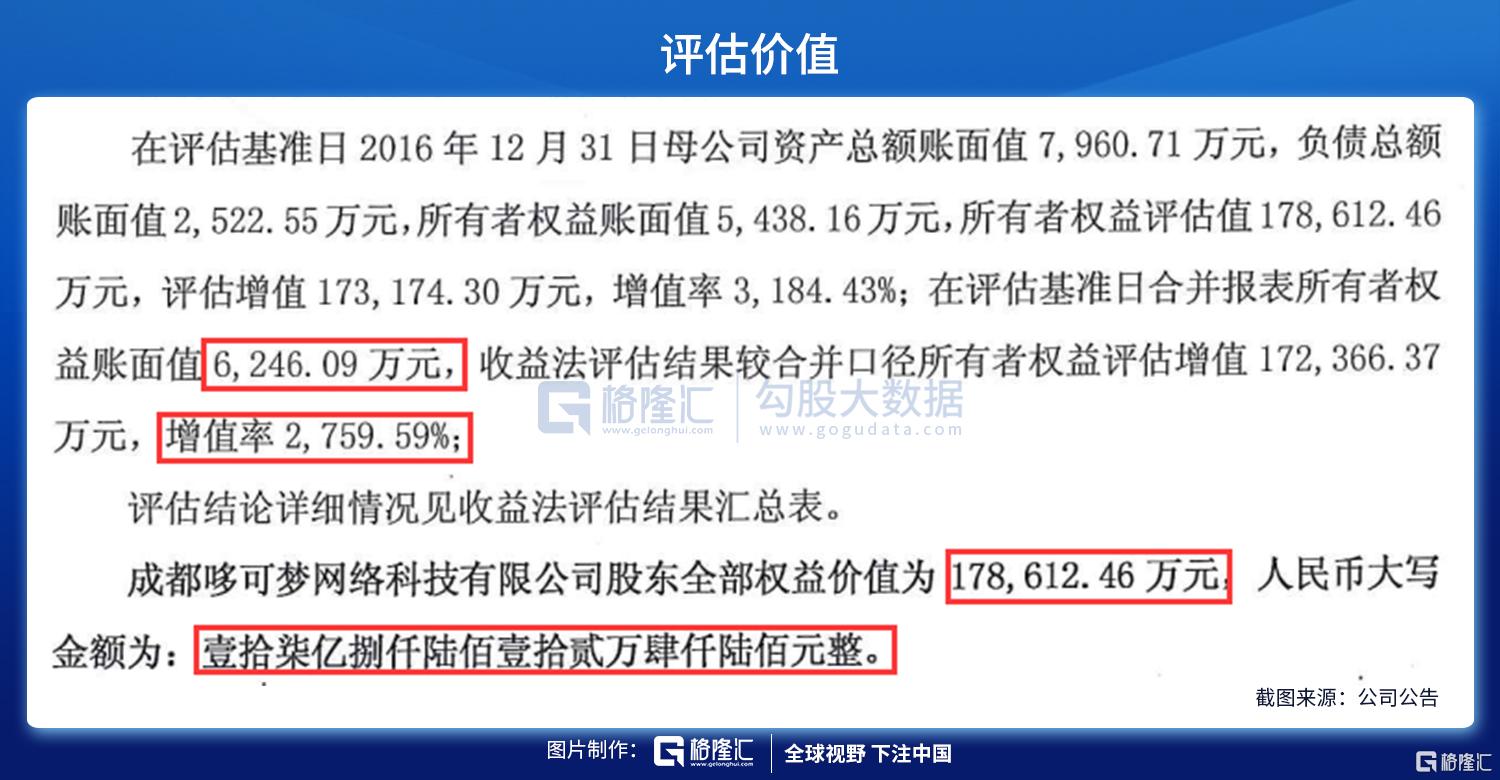

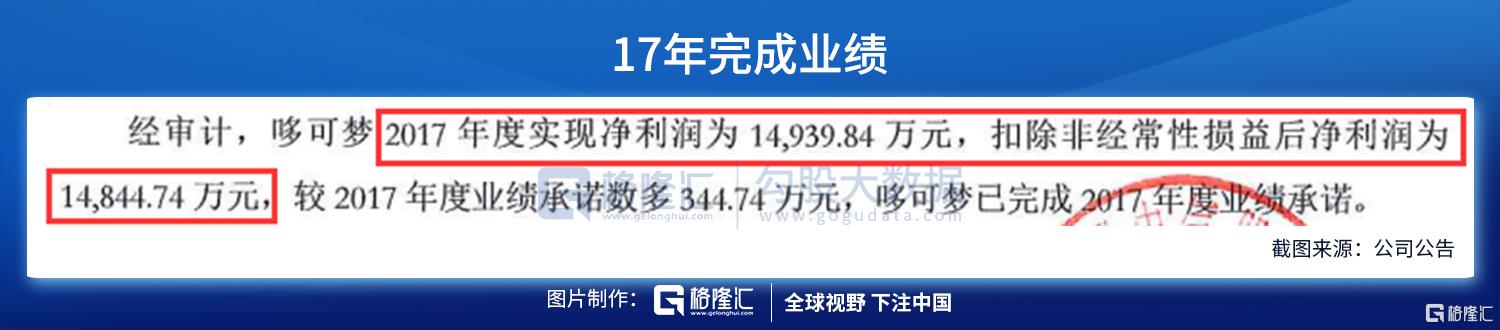

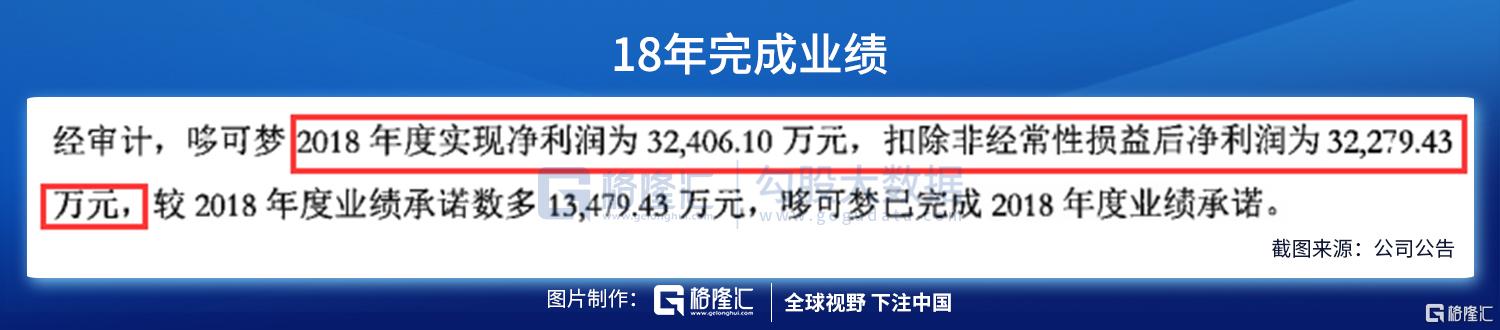

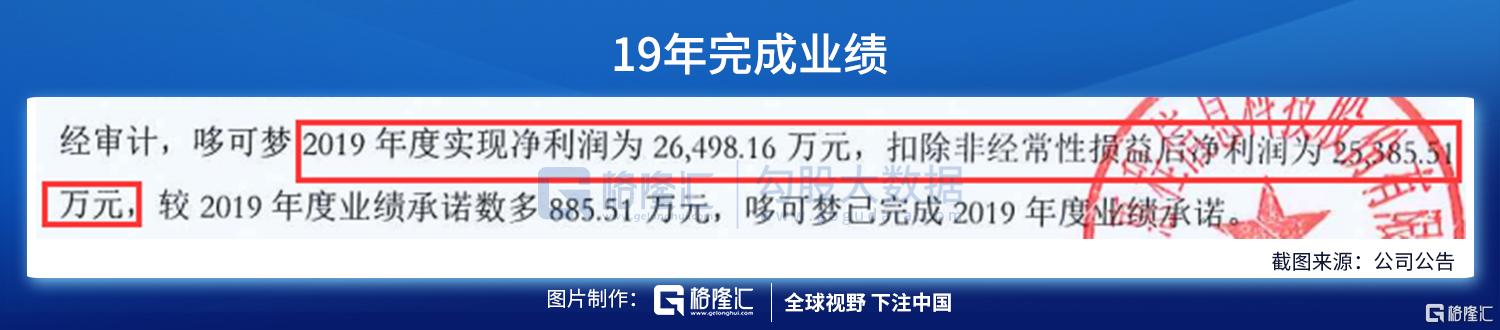

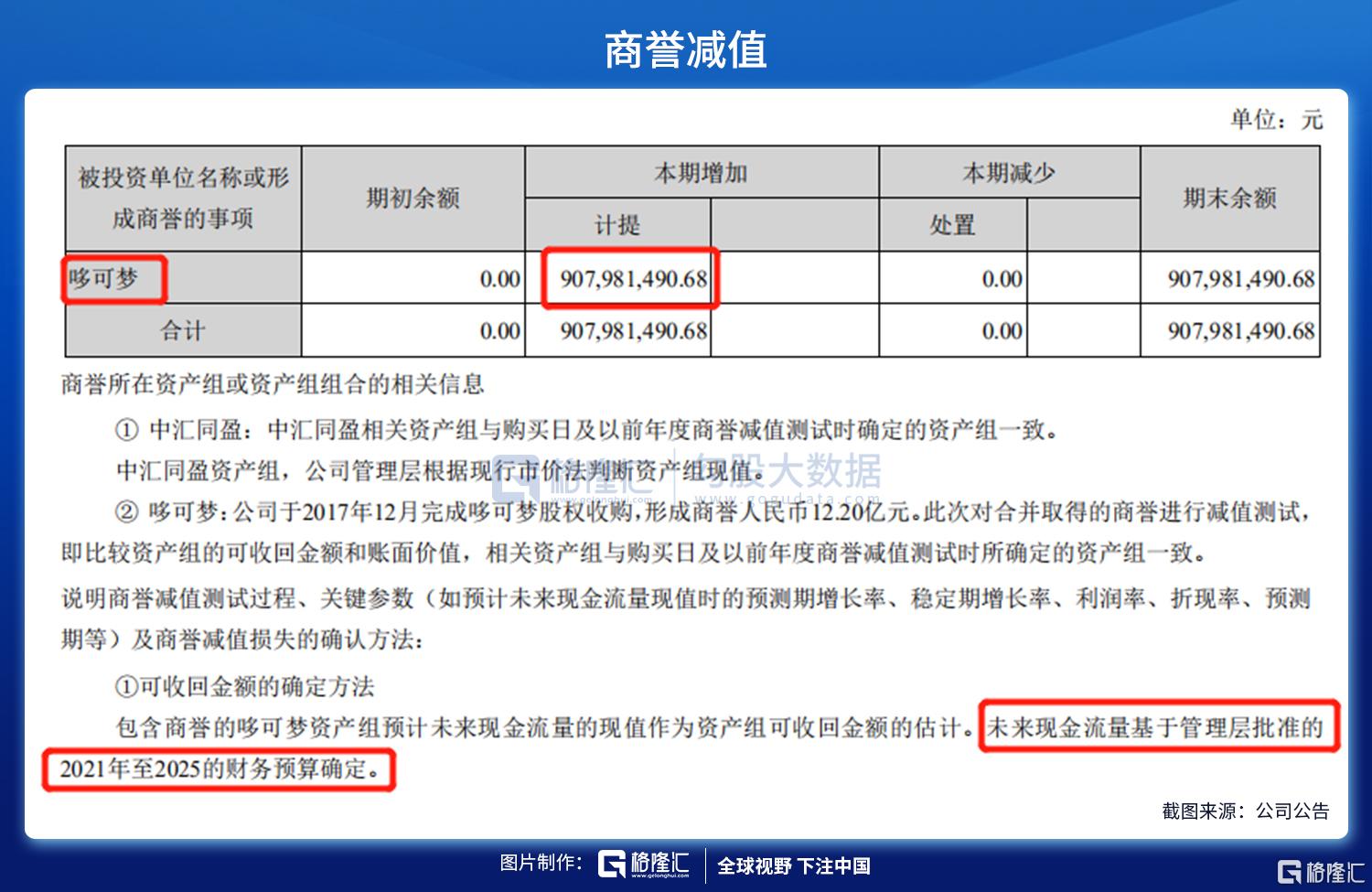

哆可夢,溢價27倍存疑

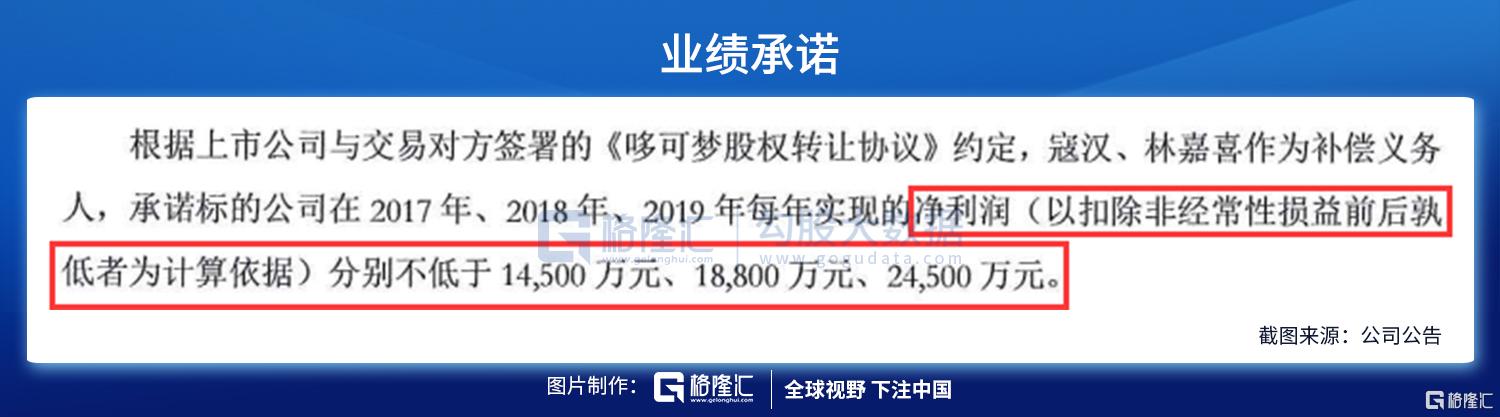

2019年,實現扣非淨利潤2.65億元,較19年業績承諾數多885.51萬元。

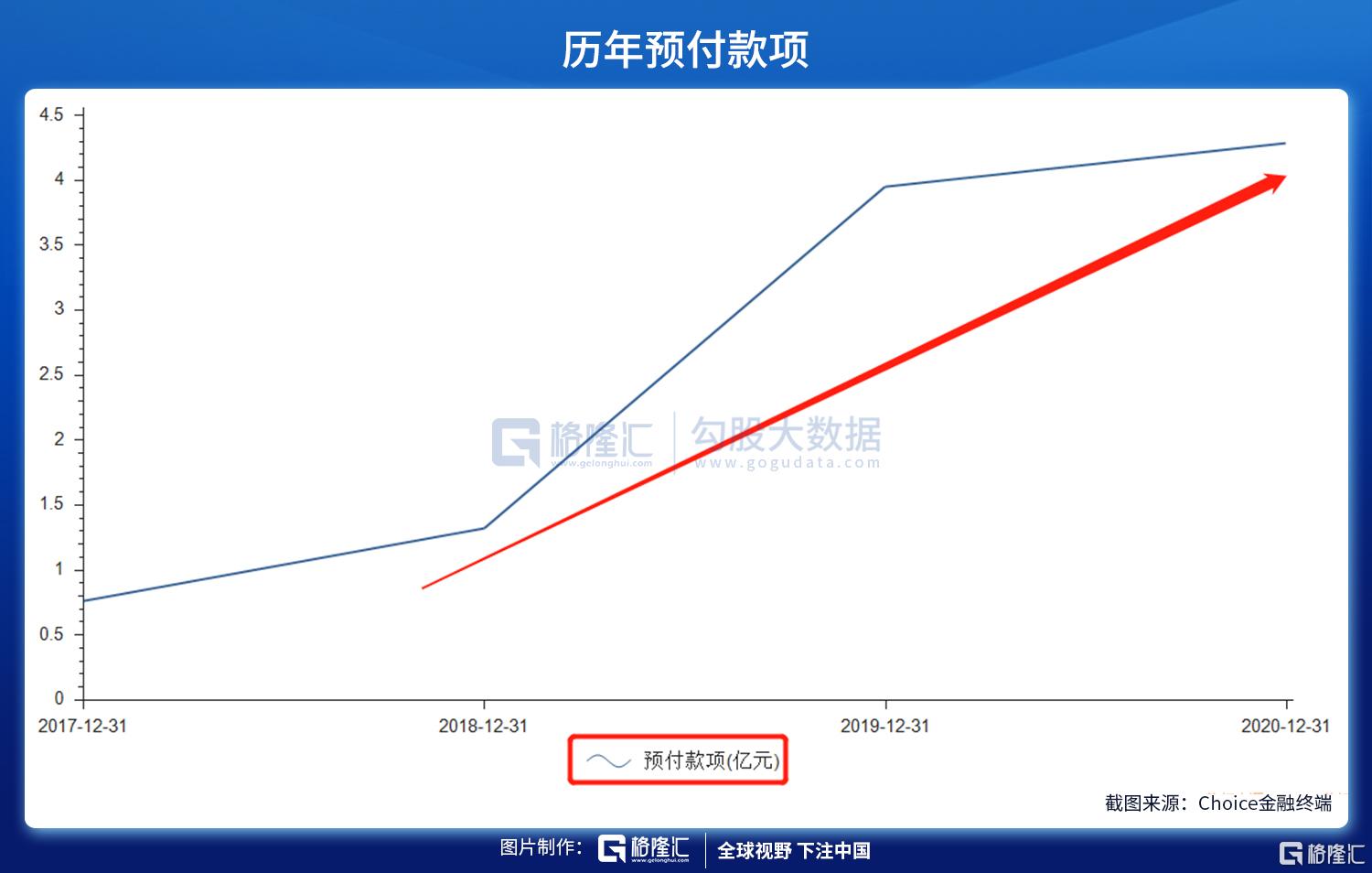

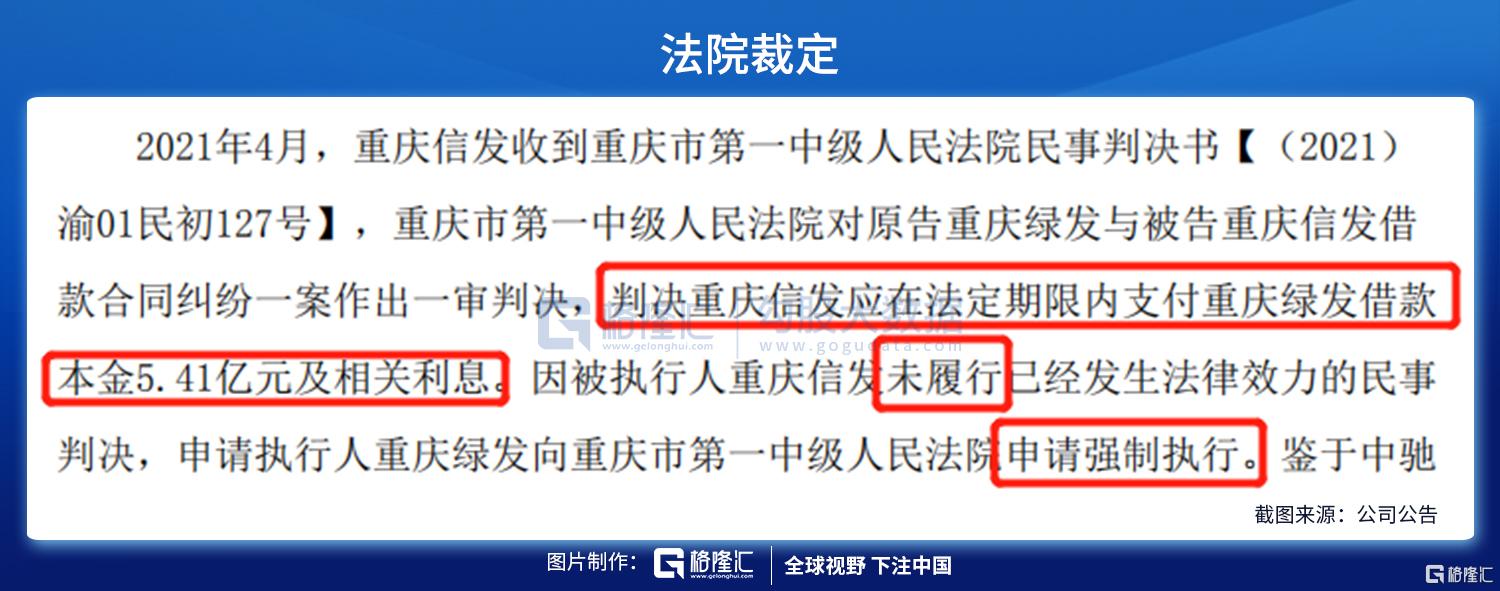

預付款之謎

結語

Follow us

Find us on Facebook, Twitter , Instagram, and YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.

More Content

CS Hotline: +852 3018 4526

Trading days: 24 hours | Non-trading days: 9:00-18:00