1. 美国债市周度观察

2. 欧洲债市周度观察

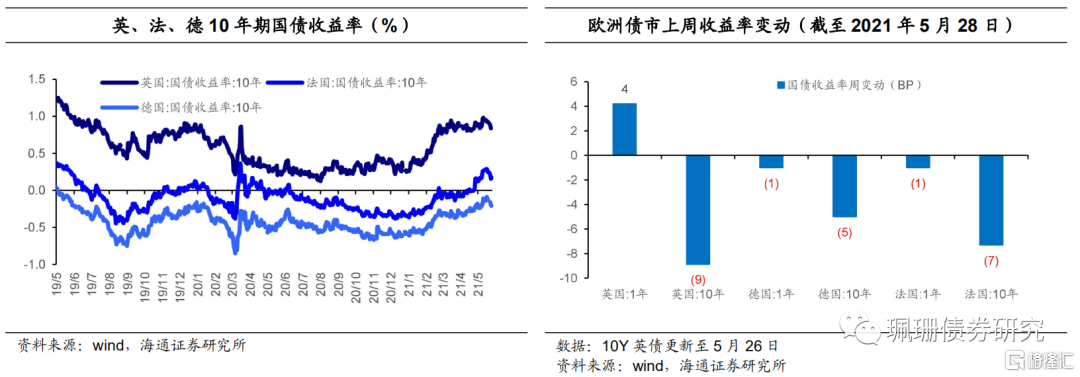

2. 1 主权债市场:英国短债下跌,法、德债市齐涨

英国5月CBI零售销售差值录得18,前值20,逊于预期。4月公共部门净借款309.62亿英镑,前值273亿英镑;政府收支短差335.64亿英镑,前值192.25亿英镑。上周英国债市分化,短债利率上行,长债利率下行。截至5月28日,英国1年国债收益率为0.05%,相比前一周上行4BP。截至5月26日,英国10年国债收益率0.84%,周度环比下行了9BP。

德国4月进口物价指数同比升10.3%,高于前值3.4个百分点;环比升1.4%,低于前值0.4个百分点。5月IFO商业景气指数为99.2,创2019年3月以来新高,前值96.8;现况指数为95.7,前值94.1。6月Gfk消费者信心指数为-7,好于前值。第一季度未季调GDP终值同比降3.4%,略低于初值0.1个百分点;季调后环比降1.8%,初值降1.7%;工作日调整后同比降3.1%,初值降3%。上周德国债市上涨,长短债利率均下行。截至5月28日,德国1年国债收益率为-0.66%,较前一周下行1BP,10年期国债收益率为-0.18%,较前一周下行5BP。

法国4月家庭消费支出同比升32%,前值升18.7%;环比降8.3%,前值降1.1%。4月PPI同比升7.3%,高于前值2.8个百分点;环比降0.3%,前值升1%。5月CPI同比升1.4%,高于前值0.2个百分点;环比由0.1%上升至0.3%;调和CPI同比由1.6%升至1.8%;环比由0.2%升至0.4%。第一季度GDP终值同比升1.2%,初值升1.5%;环比降0.1%,初值升0.4%。5月INSEE制造业信心指数为107,商业信心指数为108,消费者综合信心指数为97,均好于前值。上周法国债市上涨,长短债利率均下行。截至5月28日,法国1年国债收益率-0.64%,相比前一周下行1BP;10年国债收益率0.18%,相比前一周下行7BP。

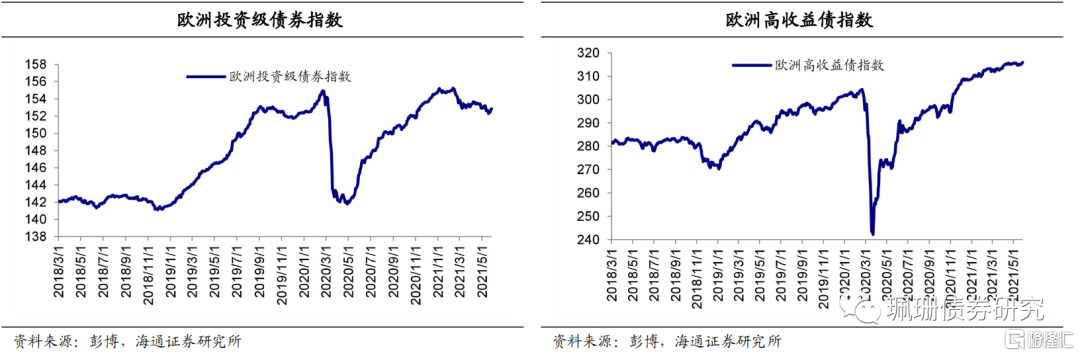

2.2 信用债市场:投资级债券指数和高收益债指数均上涨

上周欧洲投资级债券指数和高收益债指数均上涨。具体来看,投资级债指数上周上涨,整体涨幅为0.29%;高收益债指数上周上涨,整体涨幅为0.30%。

3. 亚洲债市周度观察

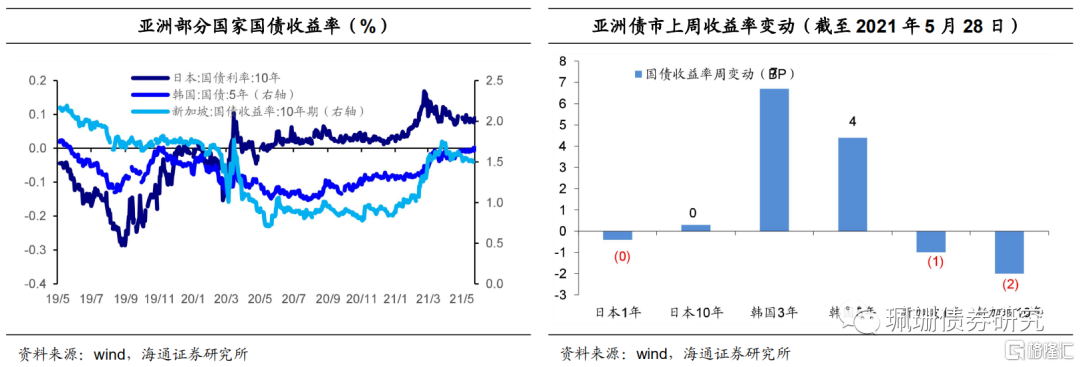

3.1 主权债市场:日本债市平稳,新加坡债市上涨

日本3月领先指标终值为102.5,前值103.2;环比升3.6%,前值升4.3%;同步指标终值为93,前值93.1;环比升3.1%,前值升3.2%。4月失业率为2.8%,较前值上升0.2个百分点。5月东京CPI同比降0.4%,前值降0.6%,降幅小于预期。上周日本债市平稳,长短债利率均持平。截至5月28日,日本1年国债收益率、10年国债收益率分别为为-0.13%、0.09%,较前一周均基本持平。

韩国央行将基准利率维持在0.5%不变,符合市场预期。上周韩国债市下跌,中短期利率均上行。截至5月28日,韩国3年国债收益率为1.16%,较前一周上行7BP,5年国债收益率为1.67%,较前一周上行4BP。

新加坡4月工业产出同比升2.1%,较前值大幅下降5.5个百分点;季调后环比升1%,前值降1.7%。第一季度GDP同比由0.2%上升至1.3%;环比由2%上升至3.1%,均好于预期。4月CPI同比升2.1%,较前值上升0.8个百分点。上周新加坡债市上涨,长短债利率均下行。截至5月28日,新加坡1年期国债收益率为0.35%,较前一周下行1BP;10年期国债收益率为1.50%,较前一周下行2BP。

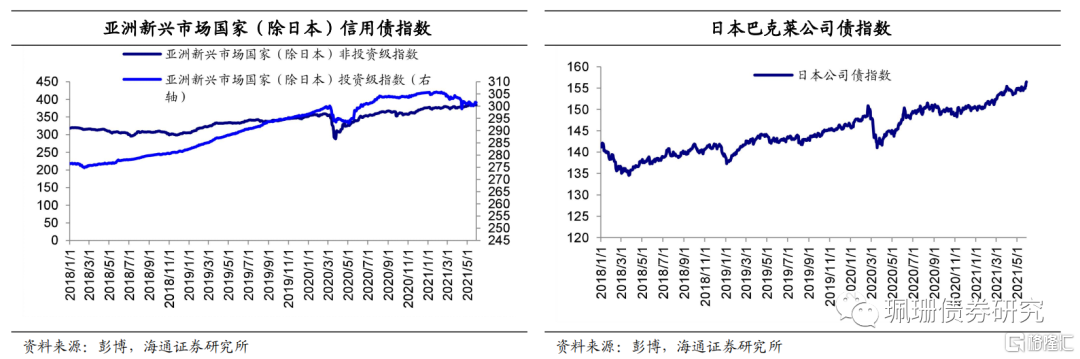

3.2 信用债市场:投资级指数和非投资级指数均上涨

上周亚洲新兴国家(除日本)投资级指数和非投资级指数均上涨。上周亚洲新兴市场(除日本)投资级指数上涨,周内整体涨幅为0.26%;非投资级指数上涨,周内整体涨幅为0.08%。

此外,日本信用债市场上周上涨。巴克莱日本公司债指数上周上涨,整体涨幅为0.93%。

4.新兴市场国家债市周度观察

4.1 主权债市场:巴西、印尼债市上涨

1)欧洲新兴市场国家:利率上行

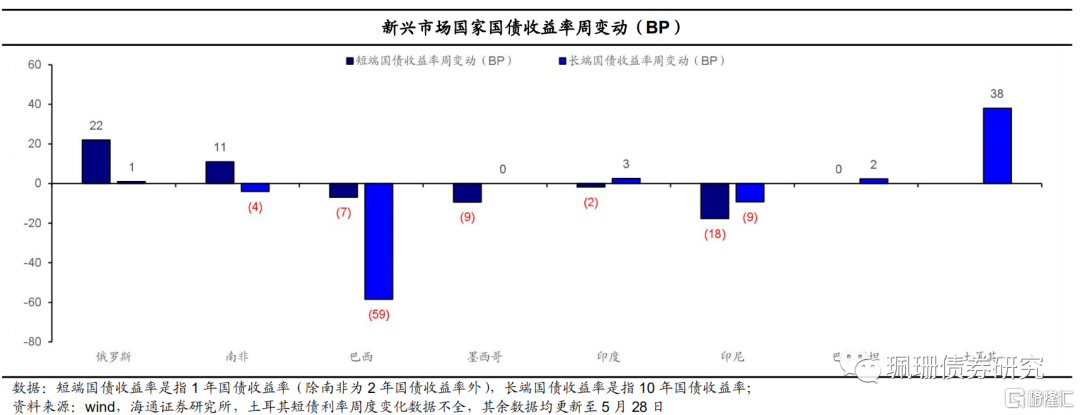

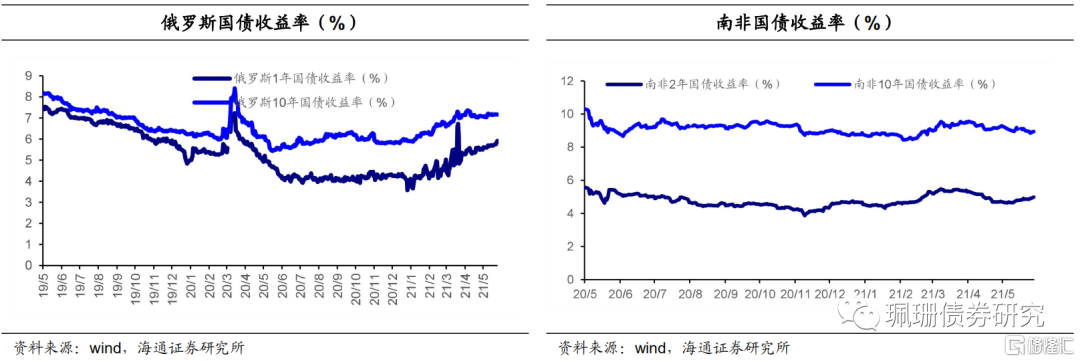

上周俄罗斯债市下跌,长短债利率均上行。截至5月28日,俄罗斯1年国债收益率为5.91%,较前一周上行22BP;10年国债收益率为7.16%,相比前一周上行1BP。

2)非洲新兴市场国家:利率分化

上周南非债市分化,短债利率上行,长债利率下行。截至5月28日,南非2年和10年期国债收益率分别为4.98%、8.95%,较上一周分别上行11BP,下行4BP。

3)美洲新兴市场国家:利率下行

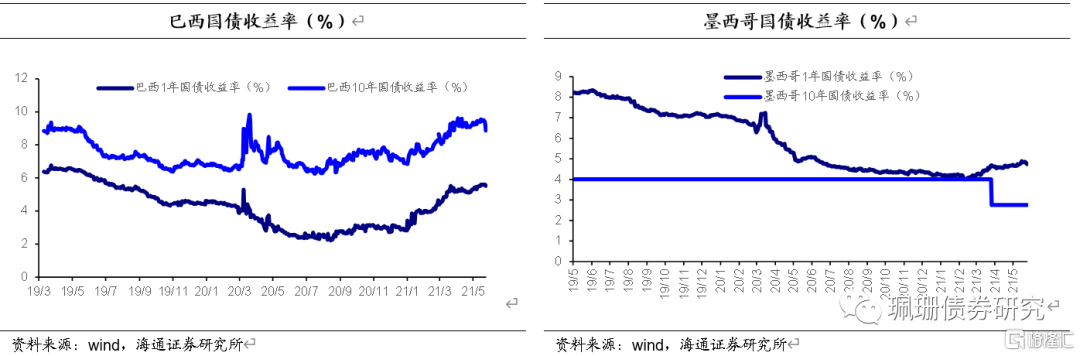

上周巴西债市上涨,长短债利率均下行。截至5月28日,巴西1年期国债收益率为5.53%,相比前一周下行7BP,10年期国债收益率为8.87%,相比前一周下行59BP。

上周墨西哥债市上涨,短债利率下行,长债利率持平。截至5月28日,墨西哥1年国债收益率为4.75%,相比前一周下行9BP,10年国债收益率为2.75%,相比前一周基本持平。

4)亚洲新兴市场国家:利率分化

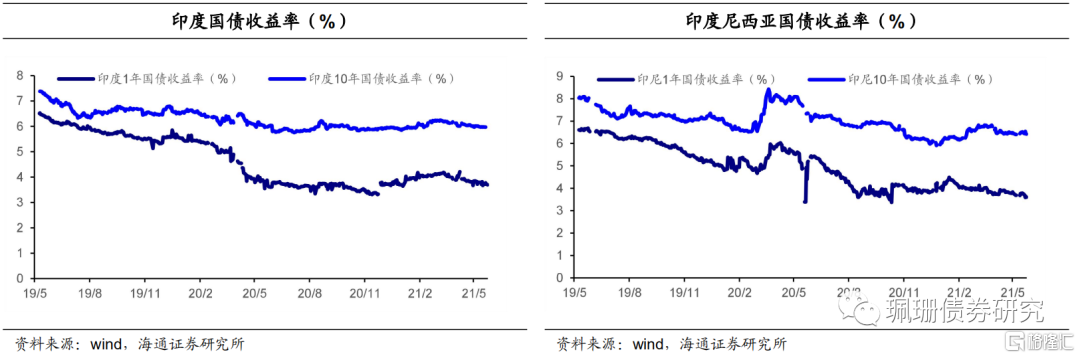

上周印度债市分化,短债利率下行,长债利率上行。截至5月28日,印度1年和10年国债收益率分别为3.70%、6.00%,相比前一周分别下行2BP、上行3BP。

印尼央行将7天逆回购利率维持在3.5%不变,符合预期。上周印尼债市上涨,长短债利率均下行。截至5月28日,印尼1年和10年国债收益率分别为3.61%、6.43%,相比前一周分别下行18BP、下行9BP。

上周巴基斯坦债市下跌,短债利率持平,长债利率上行。截至5月28日,巴基斯坦1年国债收益率为7.75%,较前一周基本持平;10年期国债收益率为9.69%,较前一周上行2BP。

上周土耳其债市下跌,长债利率上行。截至5月28日,土耳其10年国债收益率为17.86%,较前一周上行38BP。

4.2 信用债市场:投资级非主权债指数和高收益债指数均上涨

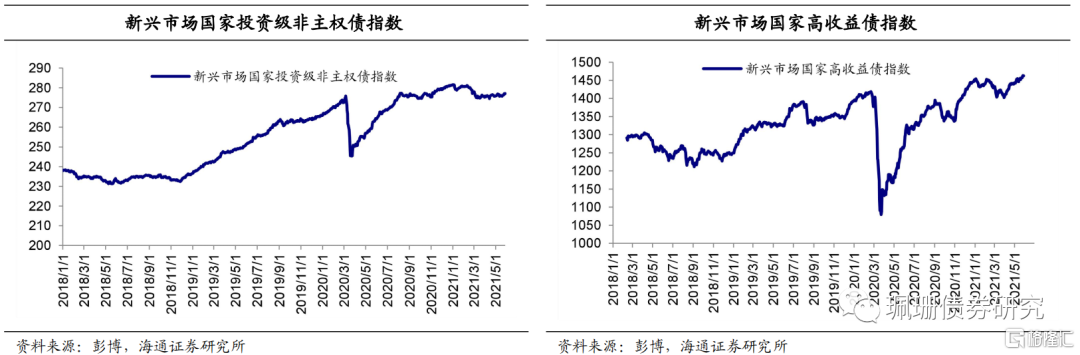

上周新兴市场国家投资级非主权债指数和高收益债指数均上涨。具体来看,新兴市场国家投资级非主权债指数上涨,周内整体涨幅0.37%;新兴市场国家高收益债指数以涨为主,周内整体涨幅为0.17%。

4.3 中资美元债收益率平均下行

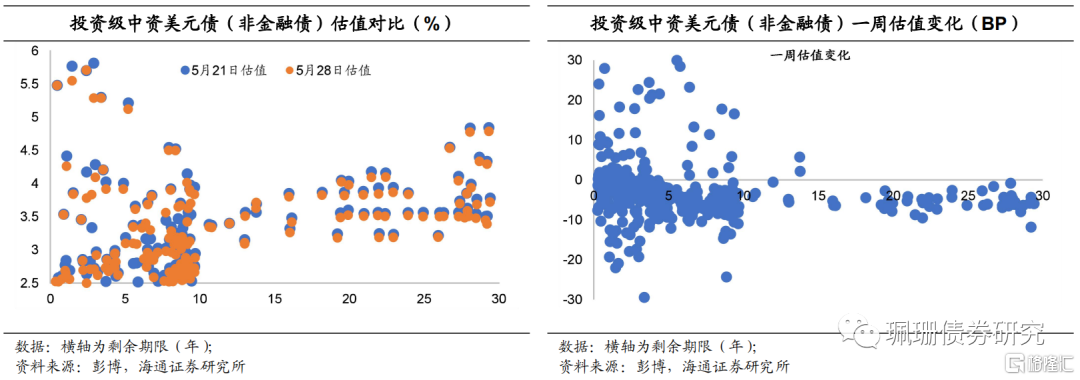

上周中资美元债收益率平均下行。根据我们的样本库,上周投资级中资美元债(非金融债)收益率下行为主。具体来看,投资级中资美元债收益率平均下行10.64BP,其中3年期及以下债券收益率平均下行13.40BP,3-5年期债券收益率平均下行6.18BP,7年期及以上期限的债券收益率平均下行10.20BP。

More Content