高鎳龍頭還能走多遠?

前段時間廣汽的“石墨烯電池“消息一公開,一度將廣汽股價推上高位,但深挖之後可知,”8分鐘快充“的理念其實跟電池高能量密度相違背,兩者魚和熊掌,不可兼得。廣汽股價之後的接連跳水也是意料之中。

撇開快充,固態電池的量產可能只是五年甚至更遠的遠期夢想,固態下正極體系不會有革命性的變化,當下分庭抗禮的仍然是磷酸鐵鋰和三元電池。2020年國內第四季度動力電池13Gwh的裝機量裏,磷酸鐵鋰佔比第一次超過三元,達到53%。在磷酸鐵鋰的強勢猛攻下,是不是三元的路會越走越窄呢?

不盡然,今天我們來聊聊三元高鎳龍頭公司——容百科技(688005.SH)。

這是一家怎樣的公司?

容百科技成立於2014年,於2019年登陸科創板,主營三元正極及前驅體,是國內首家實現高鎳 NCM811 大規模量產的正極材料企業,並在全球範圍內率先將高鎳 NCM811 產品應用於車用動力電池,技術大幅領先同行。

由於前驅體技術壁壘高,NCM811工藝難度大,單體能量密度可以達到 260wh/kg,成組可以達到 180wh/kg,相較 NCM523 產品能量密度可以提升25%,高鎳三元成為主流車企的選擇,各大主機廠的加入進一步推動高鎳趨勢。

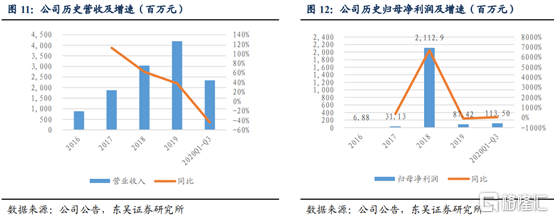

2020 年上半年容百受國內外疫情影響較大,20H1 實現營業收入 12.3 億元,同比下降 36.80%。但是三季度經營明顯好轉,20Q3 營業收入 11.14 億,環比增長 92.4%;歸母淨利潤 0.59 億,同比增長 33.59%,環比增長 103.4%,四季度大概率可以恢復到正常水平。

圖表來源:東吳證券

需求量和出貨量如何?

從需求端來看,鑑於全球長期電動化趨勢不變,高鎳正極需求會持續上漲。預計2021年全球正極需求為68萬噸,其中三元正極材料需求為43萬噸,複合增速達到 35+%。撇開海外27萬噸三元正極需求,國內需求為15萬噸。

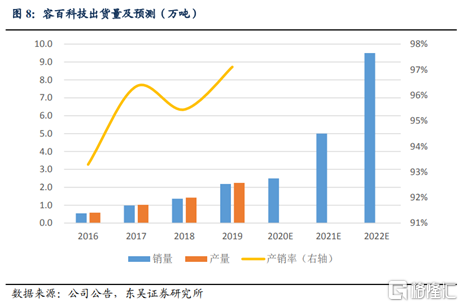

從自身供給端,2017年-2019年容百出貨量一直穩定增長,分別為0.98/1.36/2.19 萬噸,增速 80%/38%/61%。受疫情拖累,預計 20 全年出貨預計 2.5 萬噸左右,同比增速 10-15%。21年產能與訂單同步落地,預計產能10萬噸,出貨分別可達 5萬噸,同比增長 101%。

圖表來源:東吳證券

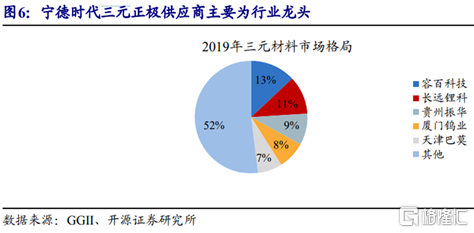

從市佔率來看,容百與當升科技、長遠鋰科處於正極材料第一梯隊,19 年國內三元材料市佔率第一,佔比13%,核心產品NCM811市佔率超過 50%。隨着需求量增加和產能釋放加速,三元行業會變得更加集中,CR5的市佔率有望進一步加強。

圖表來源:開源證券

大客户有哪些?

容百19 年前五客户佔比達到 80.9%,客户集中度提升28%。目前公司第一大客户為寧德時代,另外力神、中航鋰電、孚能、億緯鋰能、SK 等均為重要客户。

合作關係中,容百深度綁定寧德,獲得超越行業的增速。公司 2016 年通過寧德時代認證,實現小批量供貨。由於技術實力強,寧德時代 NCM811 正極唯一供應商是容百科技。預計出貨佔比超過 60%,20 年供貨預計在 1.5 萬噸以上。

21 年寧德預計NCM811出貨20Gwh,對應三元正極需求3.2 萬噸。

公司全面覆蓋國內一二線客户,並開始滲透海外主流電池企業,客户的快速擴產將使容百充分受益。

小結

磷酸鐵鋰的趨勢回潮促使新能源汽車電池的技術改進加速,無論是現有的技術還是未來可能出現的技術,行業競爭只會越來越激烈。高鎳電池能夠提供更多的能量密度,緩解消費者的續航焦慮,它仍然是長期趨勢。2021年NCM811電池滲透率會進入加速提升階段,公司作為三元高鎳龍頭,目標已經十分明確。

預計2020-2022年預計歸母淨利1.8/5.5/9.1億,同比增長107%/205%/64%,對應 PE 為 132x/43x/26x。容百科技現在市值300億,還有很大的上升空間。公司 21 年新增產能爬坡完成,且新增海外訂單增量較大。公司定位中高端,技術領先,長期競爭力強勁。儘管近期A股調整,短期的市場波動並不會影響龍頭公司的發展,容百科技值得持續關注。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.