珠江鋼琴(002678.SZ):財務估值模型

勾股大數據-珠江鋼琴財務估值模型(點擊下載)

廣州珠江鋼琴集團股份有限公司成立於1956年,是一家集鋼琴、數碼樂器、音樂教育、文化傳媒、互聯網科技協同發展的綜合樂器文化企業,是國內首家實現A股整體上市的樂器文化集團。鋼琴年產銷量超過16.5萬架,已累計產銷鋼琴超過230萬架,2018年全球市佔率高達30%。

公司已形成三大業務板塊、四大產業基地的國際化運營格局,形成了實質的跨國運營企業、多元業務聯動發展的綜合樂器文化平台。

珠江鋼琴旗下擁有愷撒堡公司、京珠公司、德華公司、舒密爾公司(16年收購90%股權)四大鋼琴製造產業基地,營銷和服務網絡覆蓋全球112個國家和地區,其中國內市場形成以省會及地級城市為中心,向周邊城市輻射的營銷服務網絡,全國擁有300多個直接經銷商,1000餘家銷售網點;國際以亞洲、歐美為核心,形成銷售服務網點200多個。

本財務估值模型將以珠江鋼琴歷史財務、業務數據作為預測基礎。

業務預測的思路如下:

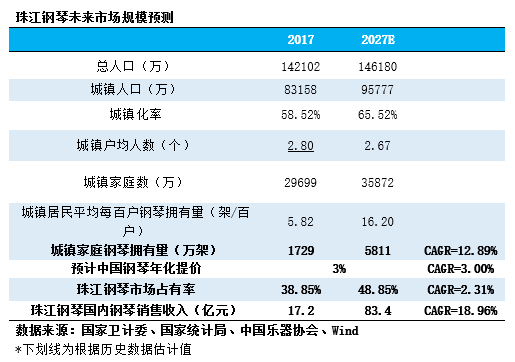

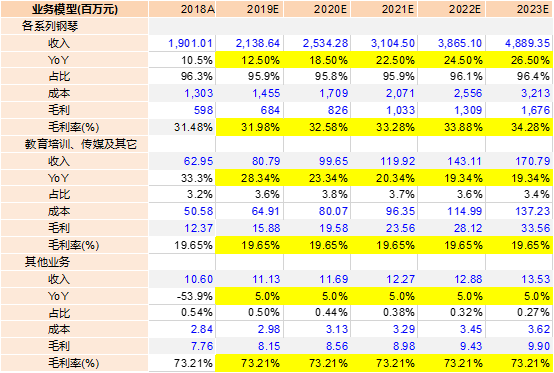

(1)各系列鋼琴:我國城鎮居民家庭2017年的滲透率僅為5.82架/百户,如果算上農村居民,我國居民鋼琴滲透率不足5架/百户,對標歐美、日本、中國香港等地區的20架/百户,我國鋼琴滲透仍有5倍左右空間。珠江鋼琴作為全球產銷龍頭,2018年在國內的市佔率已經達到38.85,%,隨着行業需求的迸發,市佔率有望進一步提升。我們預計,隨着珠江鋼琴龍頭地位的穩固,有望重新拉昇鋼琴毛利率、綜合淨利率。

(2)教育培訓、傳媒及其他:2017中國樂器行業年市場規模為405億元,而音樂教育培訓產業市場規模為792億元,培訓行業規模約為樂器銷售兩倍。珠江鋼琴這部分業務2018年的營收佔比僅3.2%,近年均維持較高增速,我們預計隨着公司的全國文化藝術教育中心建設項目、廣州文化產業創新創業孵化園項目今明兩年建成落實,該部分業務有望成為公司利潤的新增長點。預計公司未來3年,業務增速不低於20%,毛利維持20%水平。

(3)其他業務:該部分業務18年佔比僅0.54%,預計公司其他業務維持個位數增長,毛利保持歷史高水平。

珠江鋼琴未來市場規模預測如下(詳見之前的《珠江鋼琴個股研究》):

珠江鋼琴各項業務假設如下:

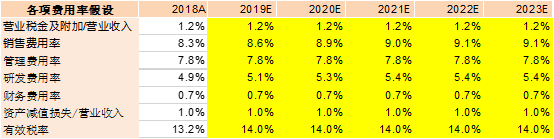

公司未來幾年將繼續加大銷售投入,研發投入提升市佔率,各項費用率假設情況如下:

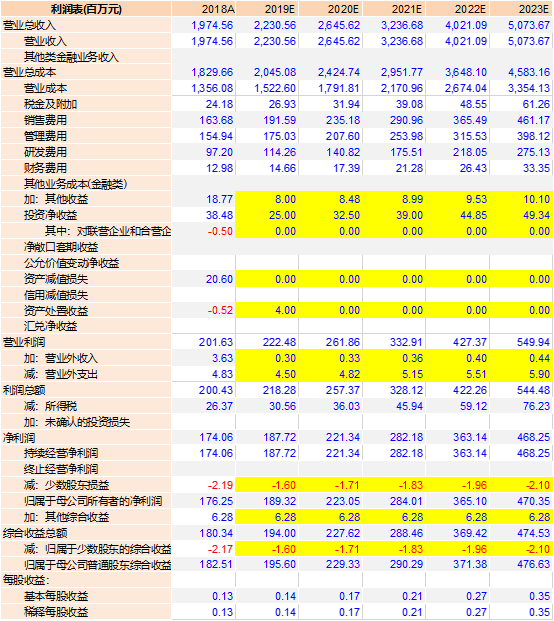

綜上,預計公司2019-2023年收入22.3/26.5/32.4/40.2/50.7億元,對應增速為13.0%/18.6%/22.3%/24.2%/26.2%,歸母淨利潤為1.89/2.23/2.84/3.65/4.70億元,對應增速為7.4%/17.8%/27.3%/28.6%/28.8%。

公司預測利潤表如下:

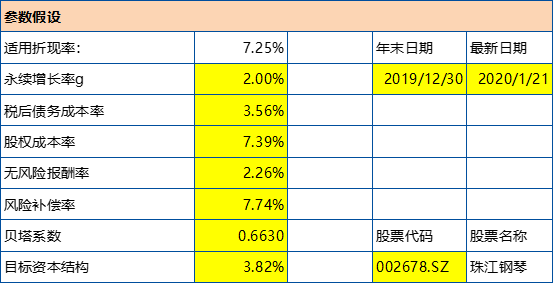

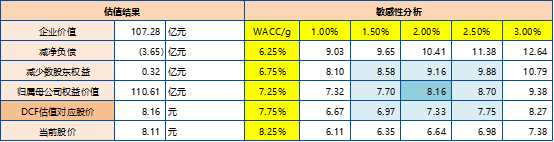

DCF估值假設:永續增長率為2.0%,無風險報酬率為2.26%,風險補償率為7.74%,則WACC為7.25%。根據敏感性分析得出估值區間為6.97-9.88元,對應2019年預測收益為48.42倍-68.61倍PE,截至2020年1月21日最新收盤價8.11,珠江鋼琴內在價值相對其目前股價的溢價率為0.56%。

本模型展示了我們對於珠江鋼琴未來發展的一種理解,不作為任何投資依據。各位用户可根據自己對公司發展的推測,自行設置參數調整估值模型。

利益聲明:本文所有分析僅為分享交流,並不構成對具體證券的買賣建議,不代表任何機構利益,同時可能存在觀點有偏情況,僅供參考。各位讀者需慎重考慮文中分析是否符合自身特定狀況,自主作出投資決策並自行承擔投資風險。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.