國藥控股(1099.HK):前景平淡,催化劑有限;維持持有評級,目標價27.5 港元

機構:銀河證券

評級:持有

目標價:27.5 港元

■ 國藥控股 2019 年三季度業績基本符合預期。

■ 我們認為公司 2020/2021 年的盈利可見度低於 2019 年,因為其核心藥品分銷業務的收 入增長正面臨更大壓力,且財務成本上升,這些因素也將拖累盈利。

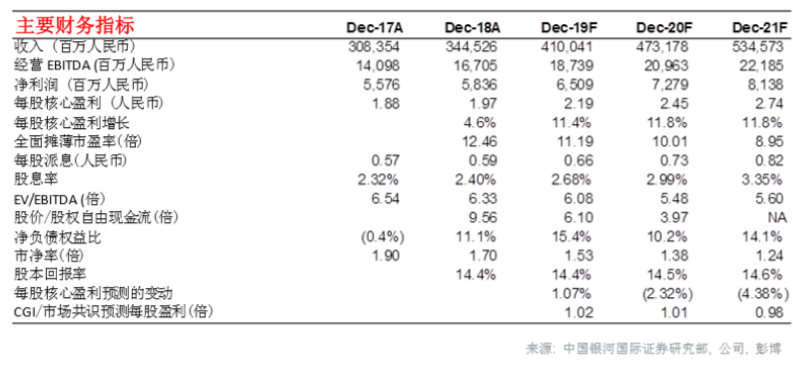

■ 我們將 2019 年淨利潤預測上調了 1.1%以反映三季報數據,我們亦將 2020/2021 年淨利 潤預測下調了 2.3%/4.4%,以反映公司即將面對的壓力。

■ 我們將基準年推移至 2020 年。目標價從 28.9 港元(12 倍 2019 年市盈率)調整為 27.5 港元(10 倍 2020 年市盈率)。下調目標估值是為了反映 2020/2021 年的增長前景較弱 和盈利可見度較低。維持「持有」評級。

2019 年三季度業績符合預期;銷售及行政費用控制相對得宜,但應收賬款 天數延長,負債率增加

從季度數據看,2019 年三季度淨利潤為 16.2 億元人民幣,同比增長 22.8%(一季度: 同比增長 28.4%;二季度:-4%)。2019 年首三季淨利潤佔我們及市場共識對 2019 全年預測的 71.4%/ 72.6%(2018 年首三季:70.6%),即大致符合預期。

此外,我們注意到三季度公司控制銷售及行政費用相對較好,銷售及行政費用/收入比 從 2018 年三季度的 4.3%降至 4.0%。

2019 年三季度的應收賬款天數增加了 10 天( 116 天,對比 2018 年三季度為 106 天), 這是由於公司向醫院的直銷增加所致。截至 2019 年 9 月 30 日,計息負債淨額權益比 為 17.3%(2018 年底:11.1%),部分是由於 2019 年三季度財務成本激增(同比增 長 28%至 11.7 億元人民幣)。

藥品分銷業務收入將受壓

2019 年首三季收入同比增長 24.7%至 3,130 億元人民幣。管理層表示,在 2019 年首九個 月,藥品分銷/零售(包括 DTP 藥房)/醫療設備分銷業務實現了約 22%/28%/40%的同比 收入增長。藥品分銷業務的 22%增長中,有 2–2.5 個百分點是來自併購,其餘約 20 個百分 點(明顯高於行業平均的高單位數增長至低雙位數增長)主要是由於“兩票制”推動行業整 合併導致公司取得份額所產生。但是展望未來,我們預計帶量採購的範圍將擴大,並覆蓋更 多普藥,這將對該細分市場的收入增長構成壓力。

毛利率前景平平

整體毛利率從2018年首三季的9%下降至2019年首三季的8.7%,我們認為這主要是由於: 1)帶量採購對藥品分銷業務利潤率構成壓力;2)直接面向病人(DTP)藥店快速發展(其 平均利潤率僅 5–6%)。我們預計,這兩個因素在未來將繼續拖累公司的毛利率。

2020/2021 年盈利可見度下降

因此適宜給予較低的目標估值 展望未來,我們認為公司的盈利可見度將下降,主要由於:1)醫保報銷標準更為嚴格,且 疾病診斷相關分組(DRG)要求醫生更嚴格地控制處方;2)帶量採購逐步擴大並覆蓋更多 普藥;(3)帶量採購政策推進高價值醫療耗材的發展,這將打擊醫療設備業務的毛利率。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.