浙數文化收購直播平台,溢價超26倍為哪般?

近日,上交所上市公司浙數文化(600633.SH)發佈公告,公司全資子公司杭州邊鋒網絡技術有限公司(以下簡稱“邊鋒網絡”)擬以自有資金現金方式出資人民幣2.32億元收購杭州聚輪40%股權,收購完成後,杭州聚輪將納入公司合併財務報表範圍。

根據公司表示,本次收購將進一步拓展公司業務範圍,提升公司數字娛樂板塊競爭實力,增強公司整體盈利能力。受此影響,截至10月23日收盤,公司二級市場股價漲超5%,報價9.32元/股。

公司收購對象杭州聚輪成立於2015年10月,註冊資本873萬元,專注於為用户提供休閒娛樂視頻直播服務,主要產品為H5、APP、小程序和PC端的“羚萌直播”平台。其中,直播業務為核心業務,根據公告,截至2019年6月,“羚萌直播”平台註冊用户已達95.83萬。

截止上半年,杭州聚輪總資產賬面價值為9508.14萬元,總資產為9499.8萬元,淨資產為2207.98萬元,根據收益評估法總負債賬面價值為7291.82萬元。

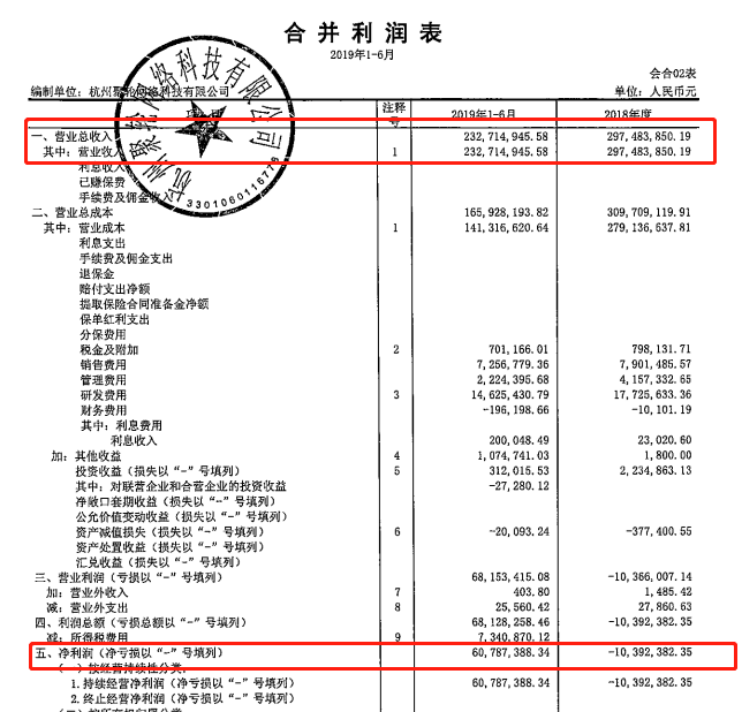

業績方面,杭州聚輪的業績波動幅度比較大。根據公告,杭州聚輪2018年的營業收入為2.97億元,淨利潤為負1039.24萬元;2019年上半年,其營業收入為2.33億元,淨利潤為6078.74萬元。

浙數文化此次收購杭州聚輪,市場上也出現了一定質疑。一方面,根據浙數文化發佈的“羚萌直播”平台月活躍用户數近百萬的數據,或存在水分。因為根據多家第三方機構發佈的直播行業相關數據顯示,虎牙、鬥魚、快手等直播平台在活躍度上處於領先位置,但都未見羚萌直播上榜。

另一方面,浙數文化此次收購標的資產評估,也飽受市場質疑,上交所也因此下發了問詢函。以2019年6月30日作為評估基準日,根據資產基礎法評估顯示,收購標的股東全部權益賬面價值為2216.32萬元,評估價值為4354.76萬元,增值額為2138.44萬元,增值率為96.49%。但根據收益法評估股東全部權益賬面價值為2216.32萬元,評估股東全部權益價值為6.19億元,增值額為5.97億元,增值率則高達2691.86%。

從評估結果來看,兩種估值差異較大,但浙數文化最終選用收益法評估結果作為評估結論。這也直接導致公司此次收購被媒體公開報道,認為存在欠缺商業方面的合理性,或涉嫌利益輸送。

因為這種差異性的存在,公司也受到上交所的問詢函,要求公司補充收益法評估的具體情況,並結合標的資產經營情況、行業情況、可比公司情況、近期可比交易情況,説明本次收購評估增值較大的依據和合理性,以及此次評估是否審慎。

和高溢價收購相反的,杭州聚輪的業績承諾卻一年比一年低,其中,2019年的業績承諾為扣非淨利潤不低於約1.08億元,而2020年承諾的扣非淨利潤為不低於約8821萬元,明顯低於2019年承諾淨利潤。

公司本次以自有現金方式出資2.32億元收購杭州聚輪網絡公司的40%股權,杭州聚輪兩年完成全部業績承諾總共為1.96億,以此計算,浙數文化近兩年享有收益僅為0.78億元。而從業績承諾來看,一年比一年低,也顯示出收購標的對未來業績沒有足夠的底氣。

其實,這次收購只是浙數文化擴張的一個縮影。浙數文化原本為浙江日報報業集團借殼上市,但在2017年啟動重大資產重組,將報業資產剝離,逐步向數字娛樂業轉型,目前主要聚焦數字娛樂產業、大數據產業和數字體育產業三大業務。

而從公司目前的主營業務,都是頻頻通過投資及收購進行產業擴張的結果。2012年公司耗資34.9億元收購盛大網絡旗下的杭州邊鋒、上海浩方100%股權,進軍手遊產業。隨後,公司還相繼收購了夢啟科技40%股權、杭州遊卡31%股權等多家公司股權。

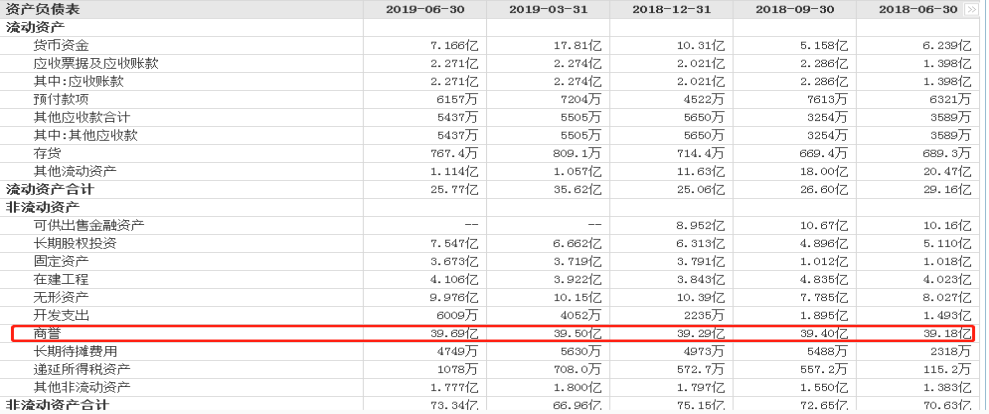

正因為公司熱衷於頻繁併購,公司目前商譽高企,截止2019年6月30日,公司商譽規模高達39.69億元。而根據公司半年報顯示,公司總資產為99.11億元,商譽佔總資產比例超過40%。

綜合來看,浙數文化此次併購網絡直播平台作為新業務,前景並不明朗。網絡直播平台經歷野蠻生長後,儘管目前仍具有一定市場熱度,但行業亂象也往往引發各類監管,而羚萌直播也並不屬於直播平台的頭部企業,或也面臨中小直播平台面臨的資金困難等問題,這對未來的浙數文化也形成考驗。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.