全球运动品牌史鉴:群雄逐鹿,谁主沉浮

作者:纺服丰毅团队

来源:杨仁文研究笔记

报告引言:

运动品牌无论是国内还是海外往往成为孕育优质投资标的的摇篮。

那么:

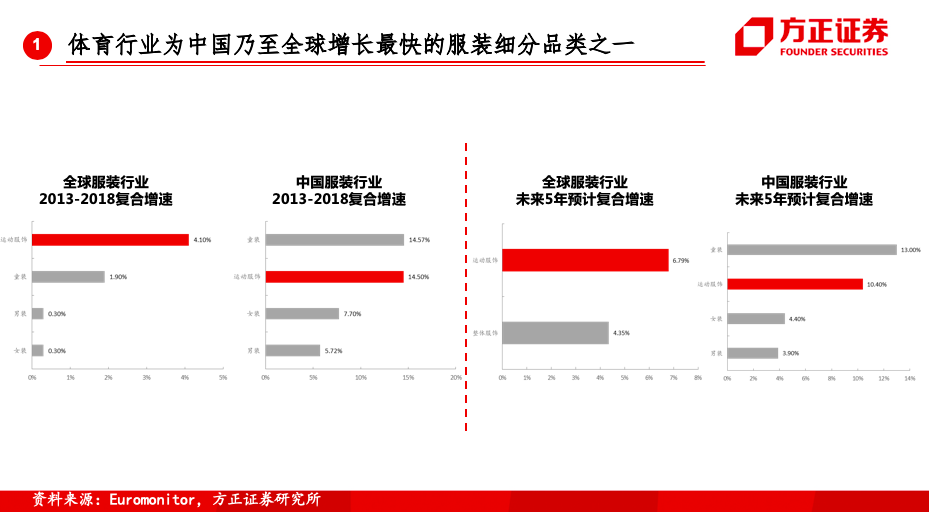

1、国内外运动鞋服在服装各细分行业中往往增速最快、集中度最高、龙头经营规模最大,原因是什么?

2、运动鞋服龙头壁垒是否真的较高?缘何全球体育史中运动品牌逆袭持续出现?运动鞋服企业核心竞争力是产品?还是营销?还是供应链?

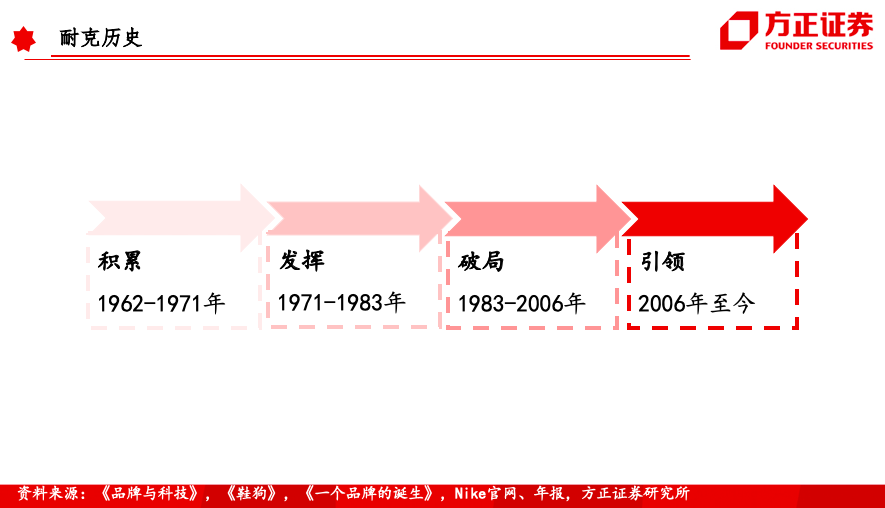

3、耐克是怎么实现超越的?阿迪是怎么实现重生的?耐克和阿迪的优势分别在哪里?

4、霍斯特、奈特、斯特拉瑟、德雷福斯、马克帕克等企业管理者,如何评判他们的功过?

5、中国的本土品牌与海外品牌竞争中处在什么位置?是否仍有投资机会?

核心观点:

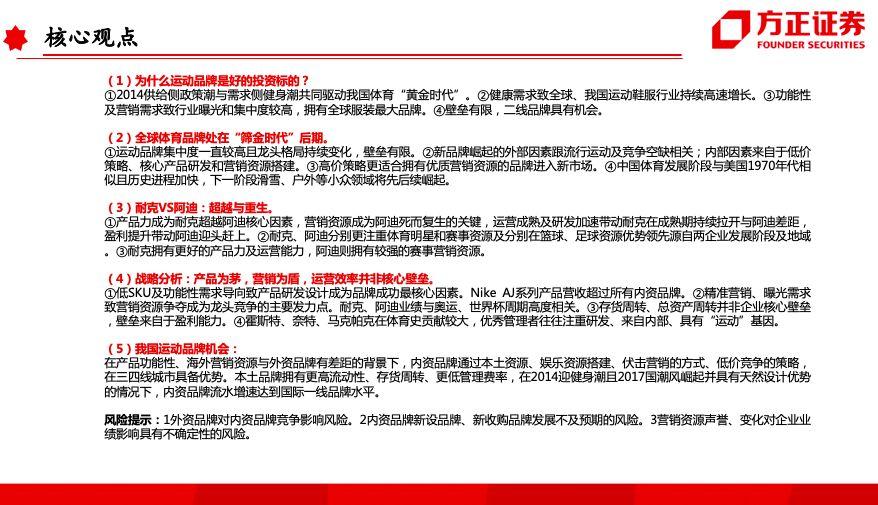

1.为什么运动品牌是好的投资标的?

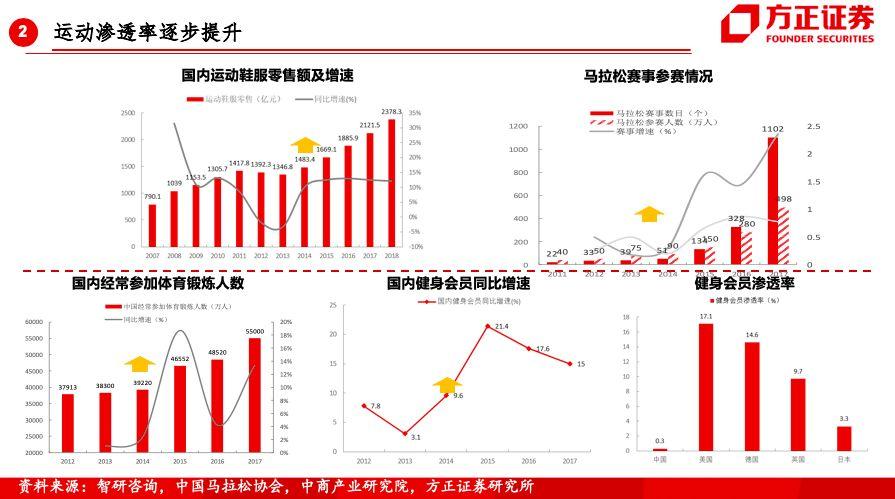

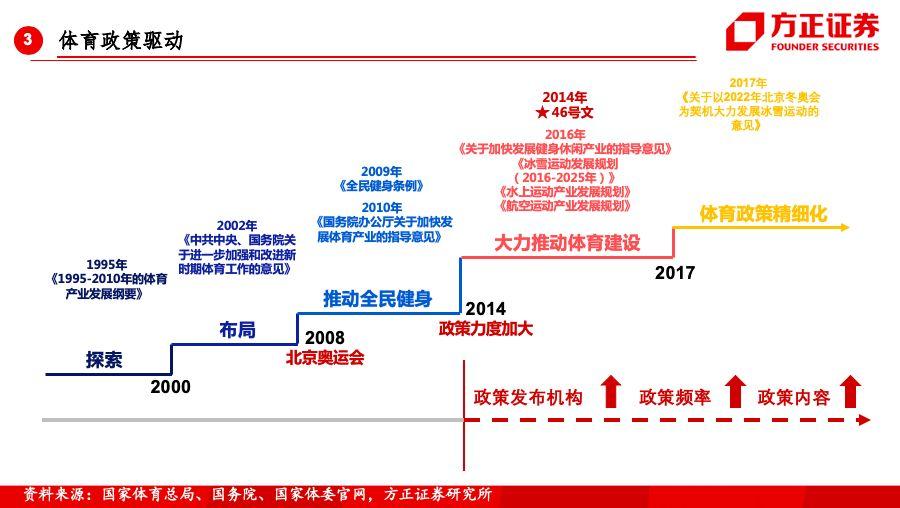

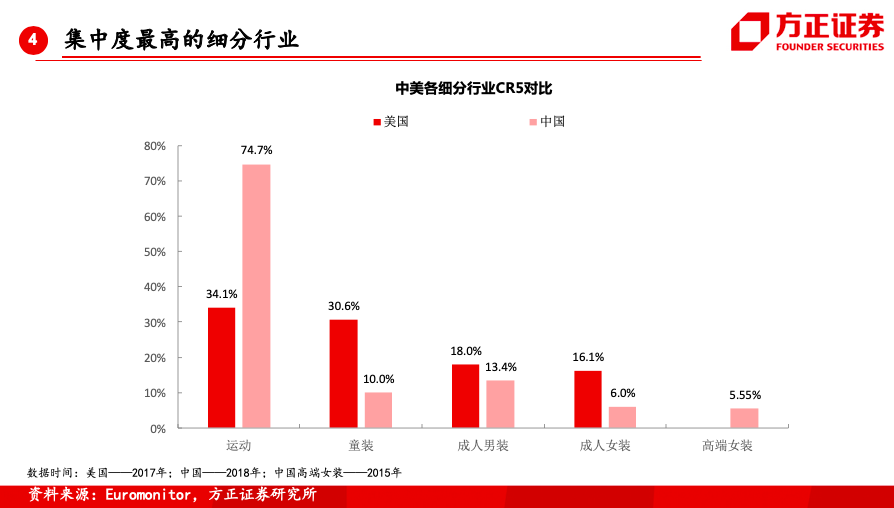

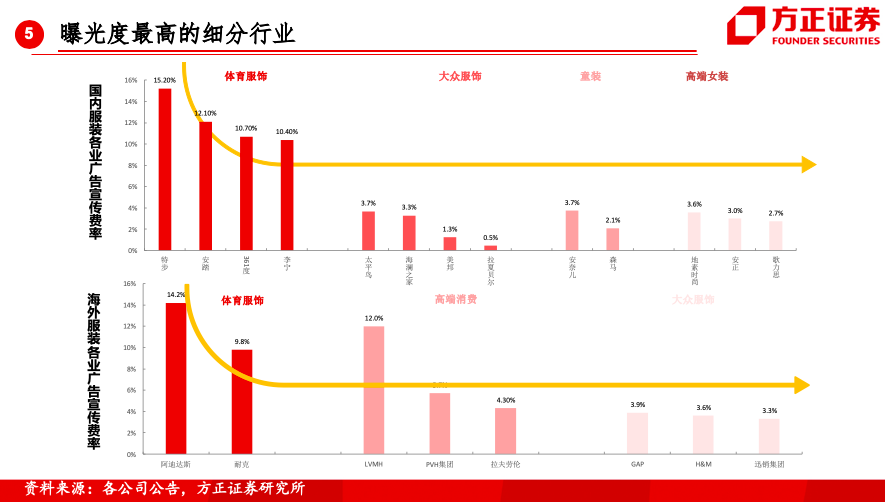

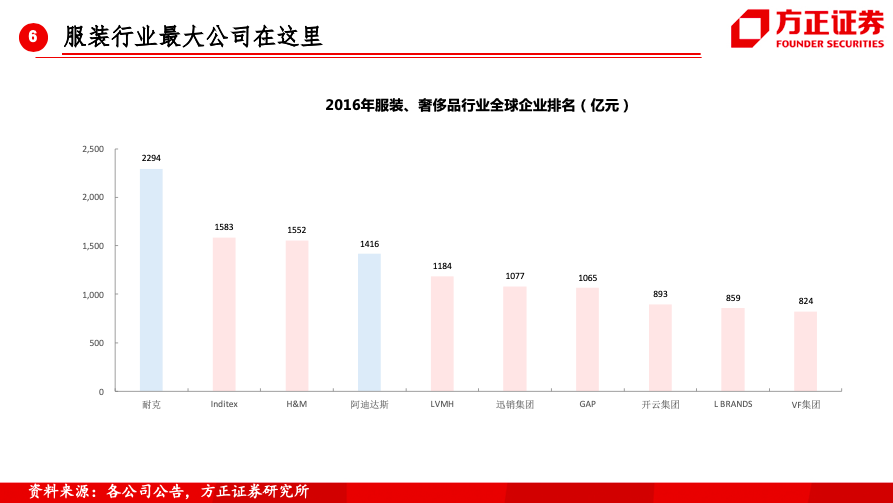

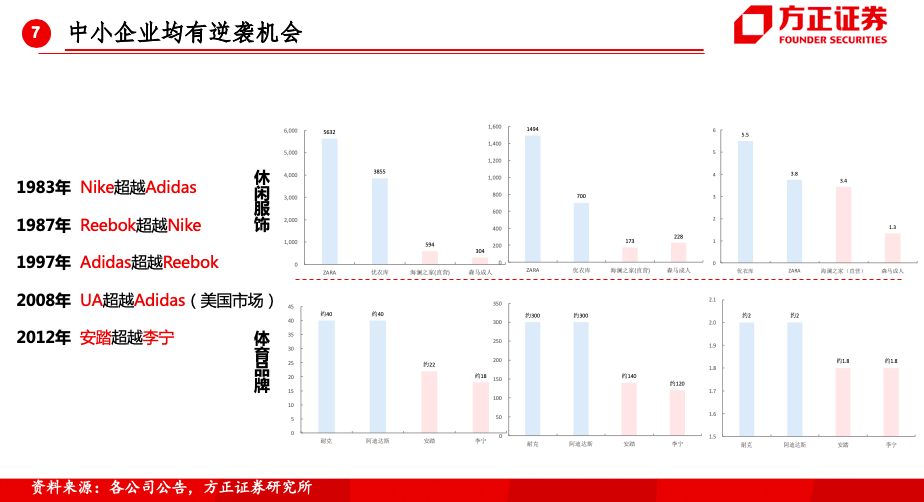

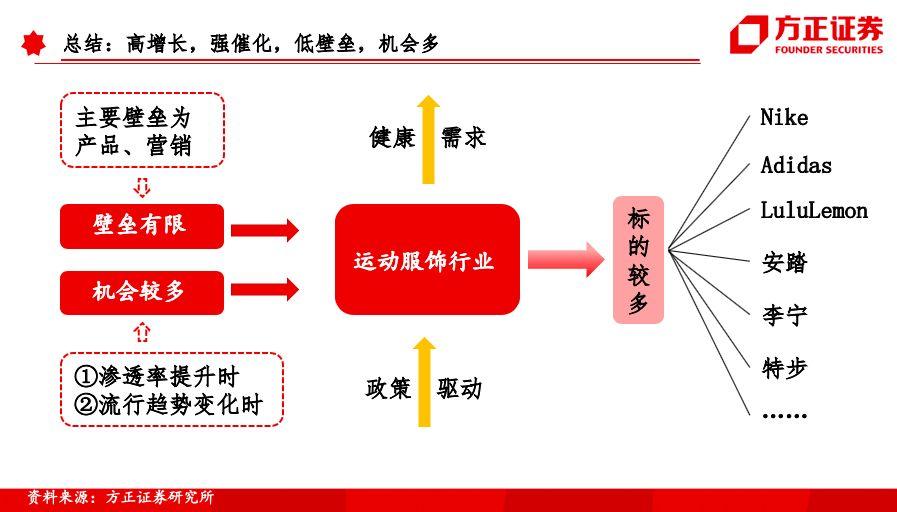

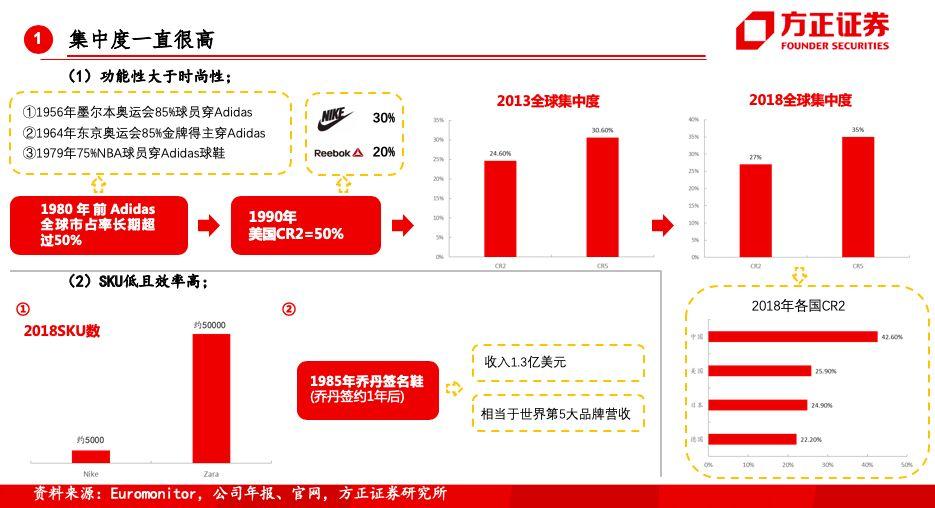

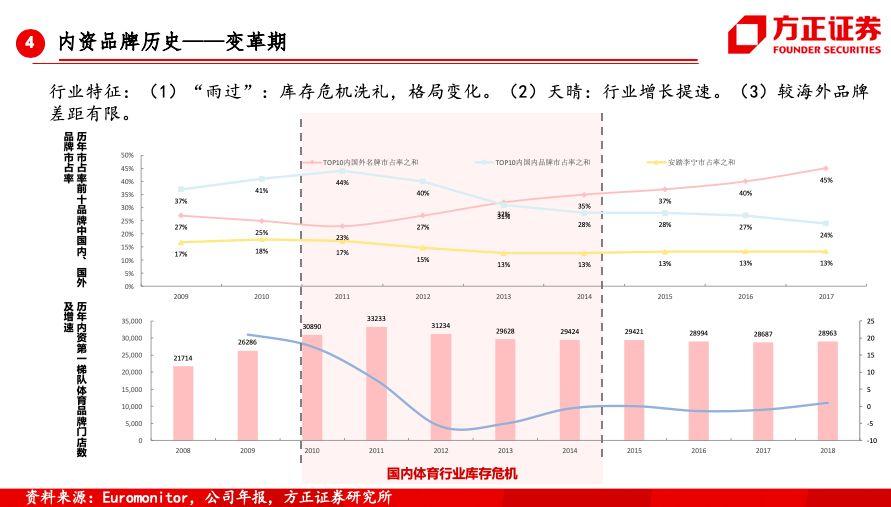

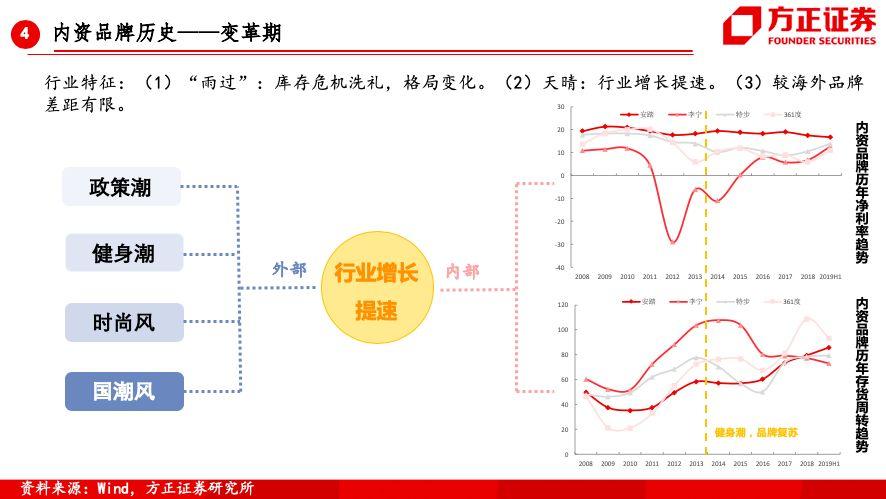

①2014供给侧政策潮与需求侧健身潮共同驱动我国体育“黄金时代”。②健康需求致全球、我国运动鞋服行业持续高速增长。③功能性及营销需求致行业曝光和集中度较高,拥有全球服装最大品牌。④壁垒有限,二线品牌具有机会。

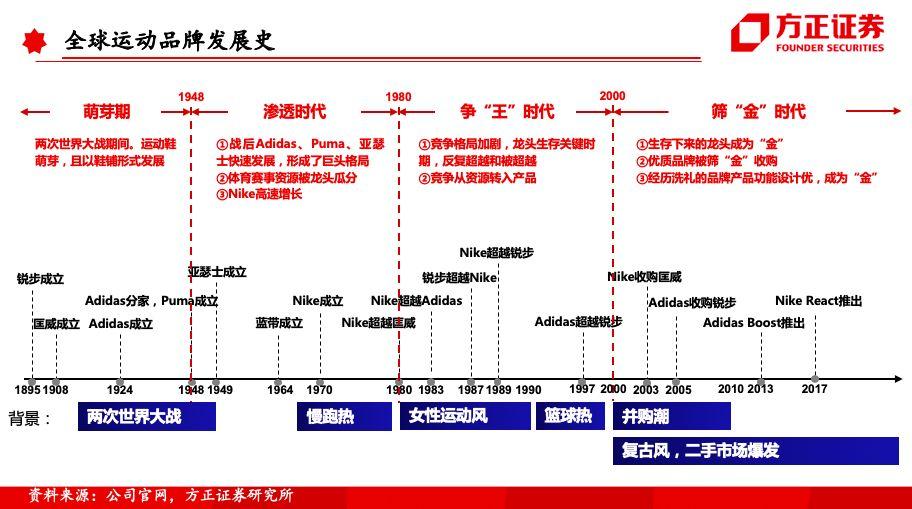

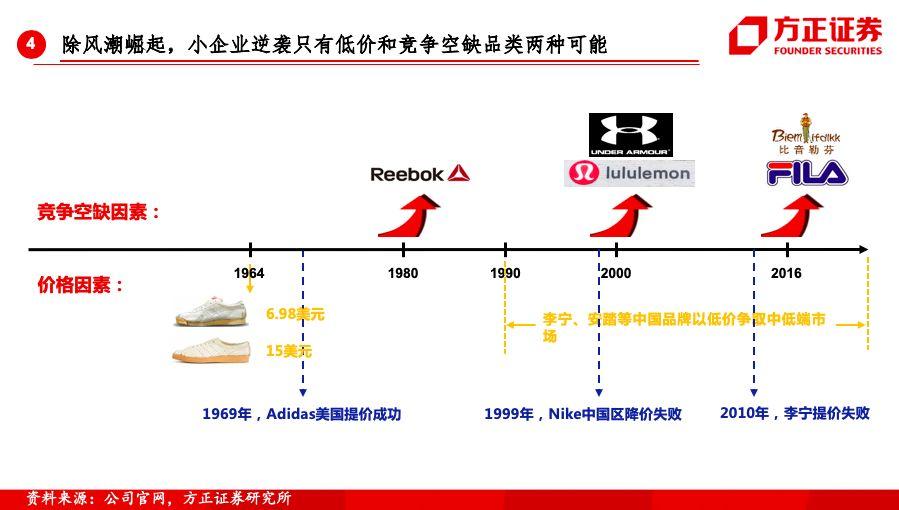

2.全球体育品牌处在“筛金时代”后期。

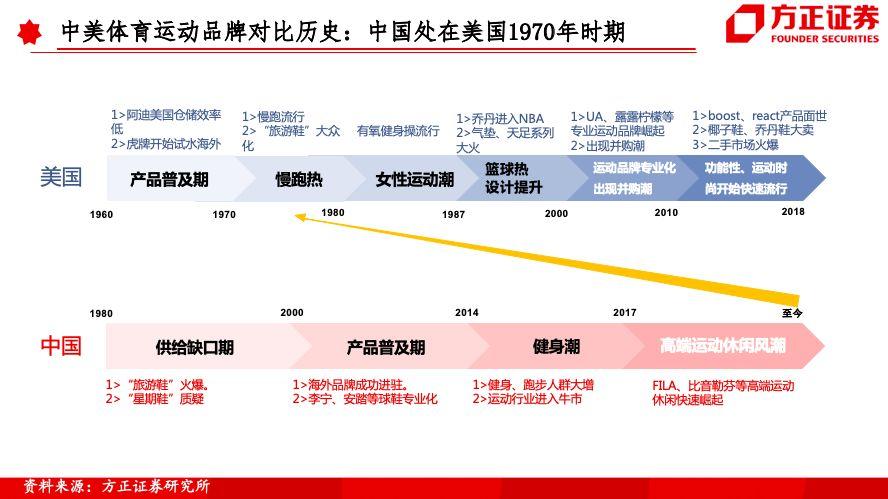

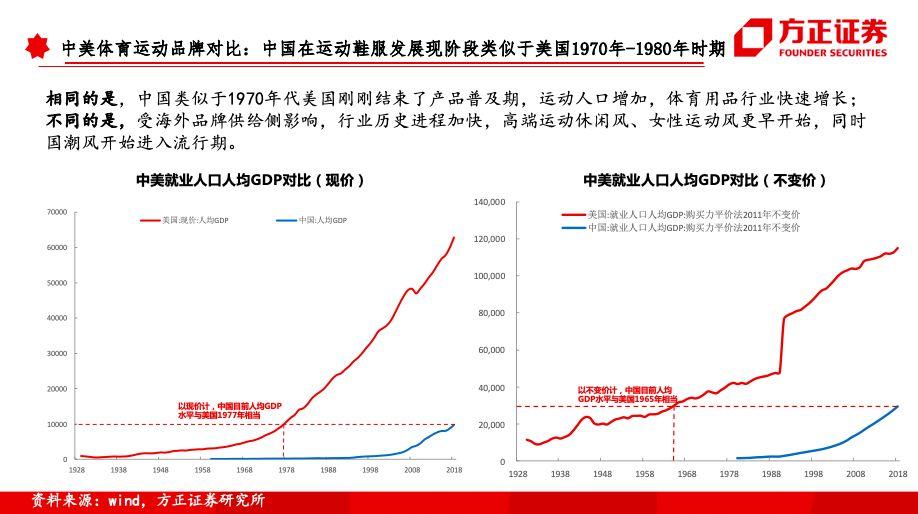

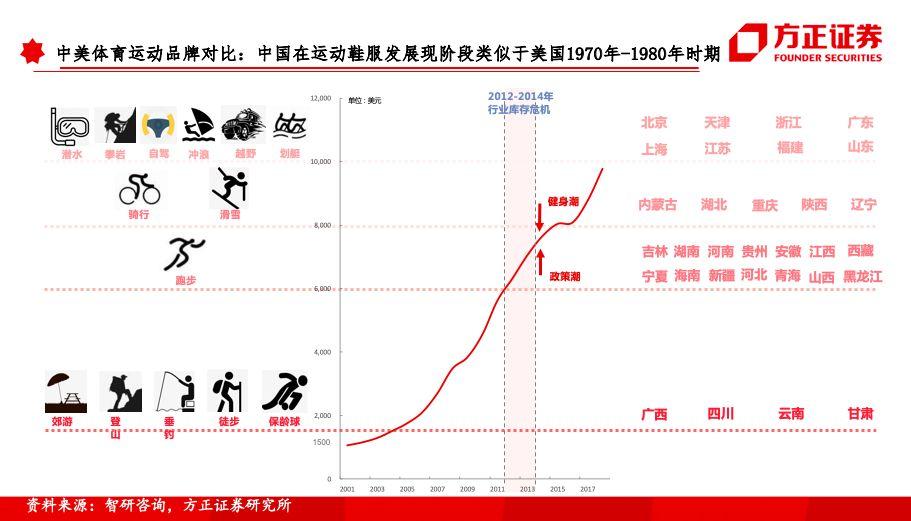

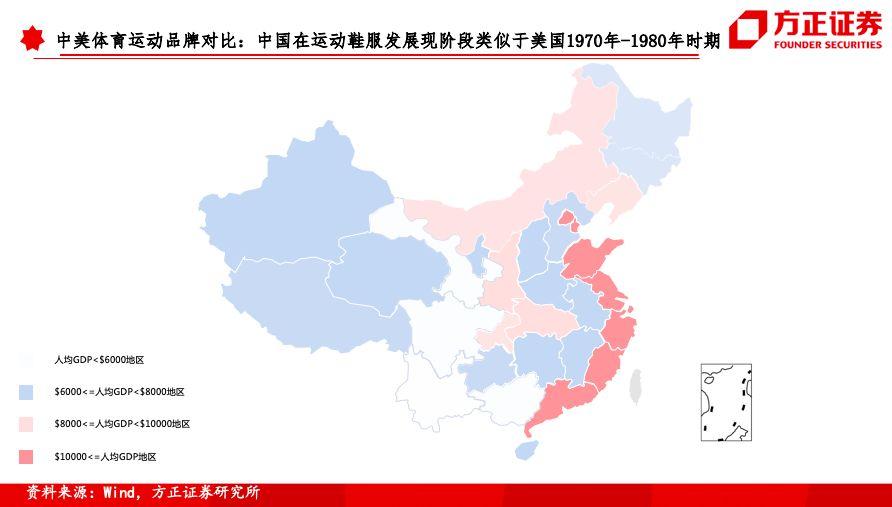

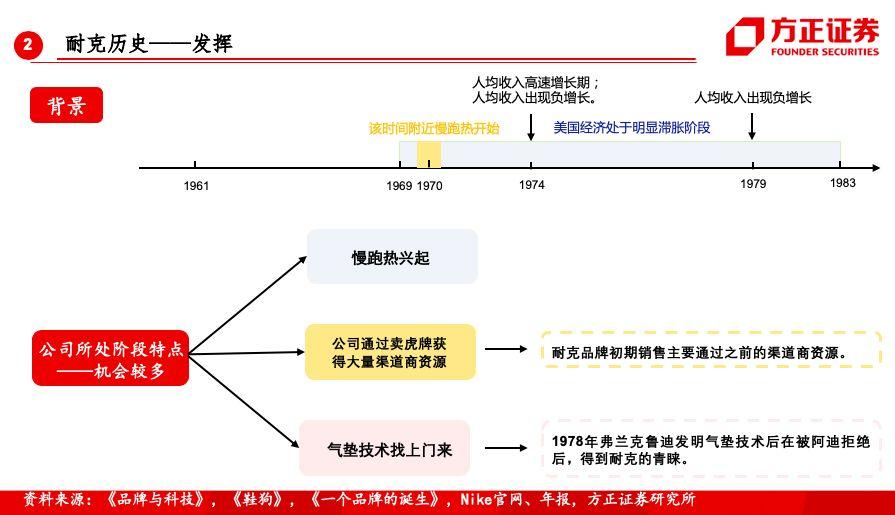

①运动品牌集中度一直较高且龙头格局持续变化,壁垒有限。②新品牌崛起的外部因素跟流行运动及竞争空缺相关;内部因素来自于低价策略、核心产品研发和营销资源搭建。③高价策略更适合拥有优质营销资源的品牌进入新市场。④中国体育发展阶段与美国1970年代相似且历史进程加快,下一阶段滑雪、户外等小众领域将先后续崛起。

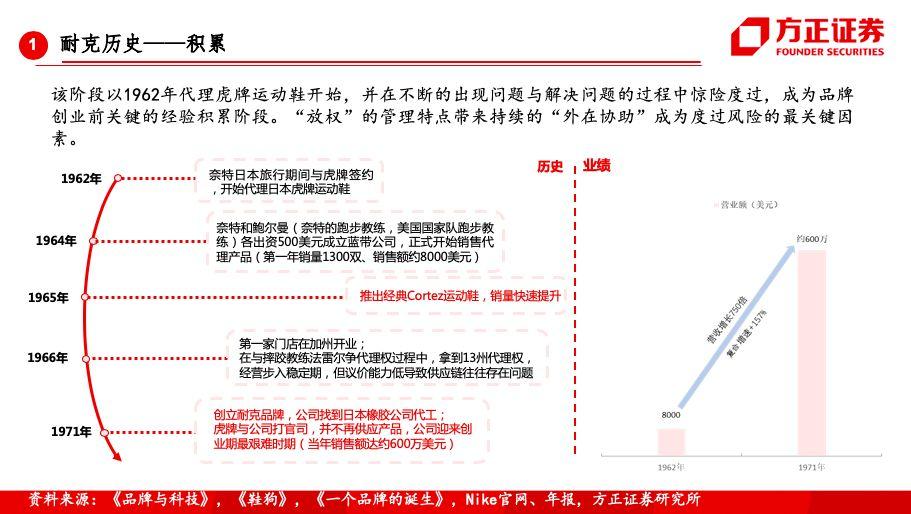

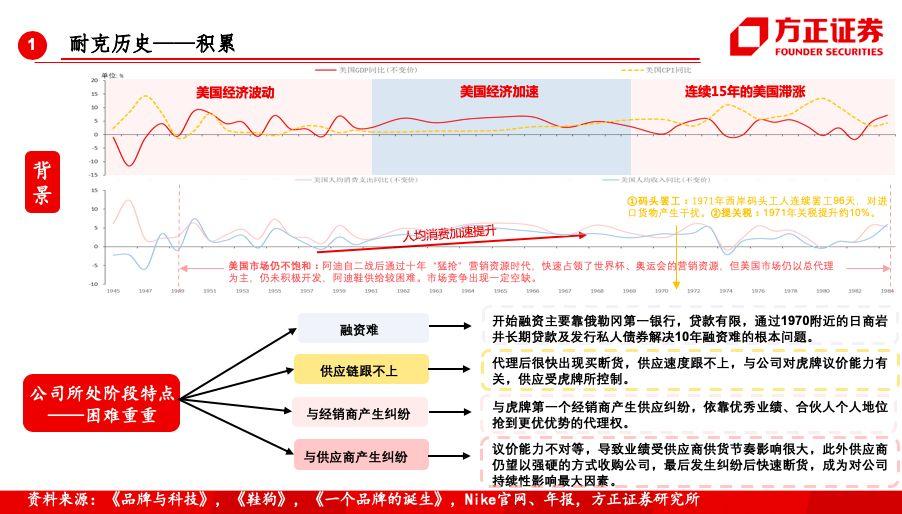

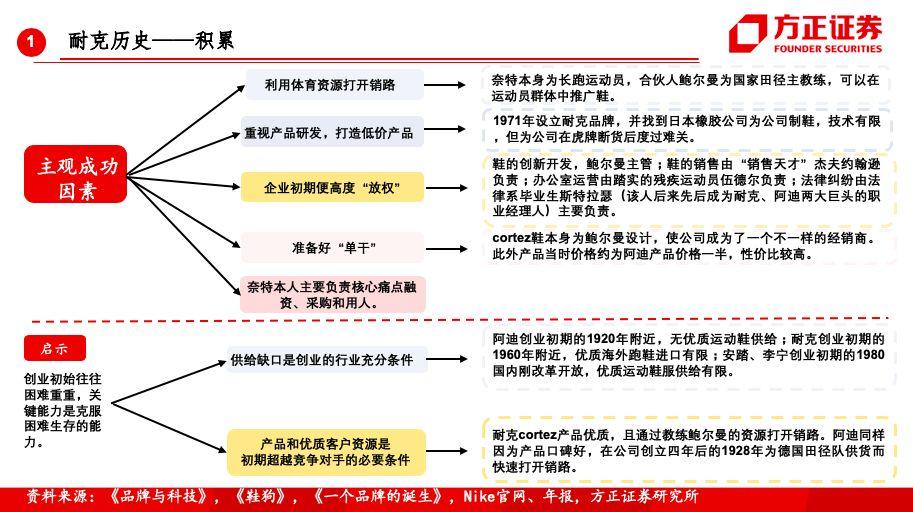

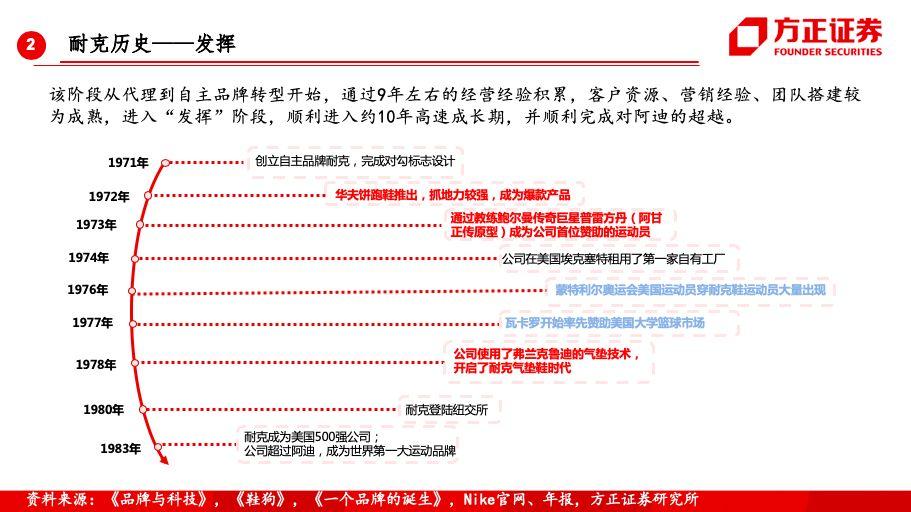

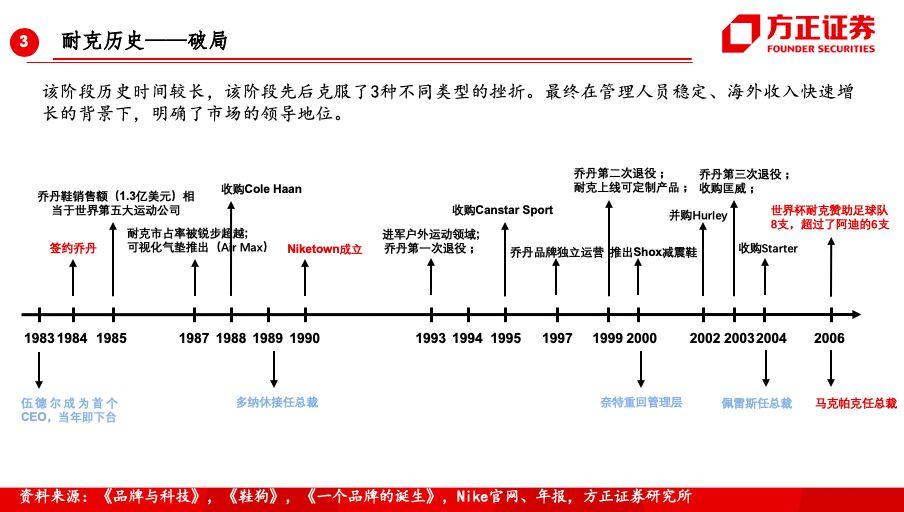

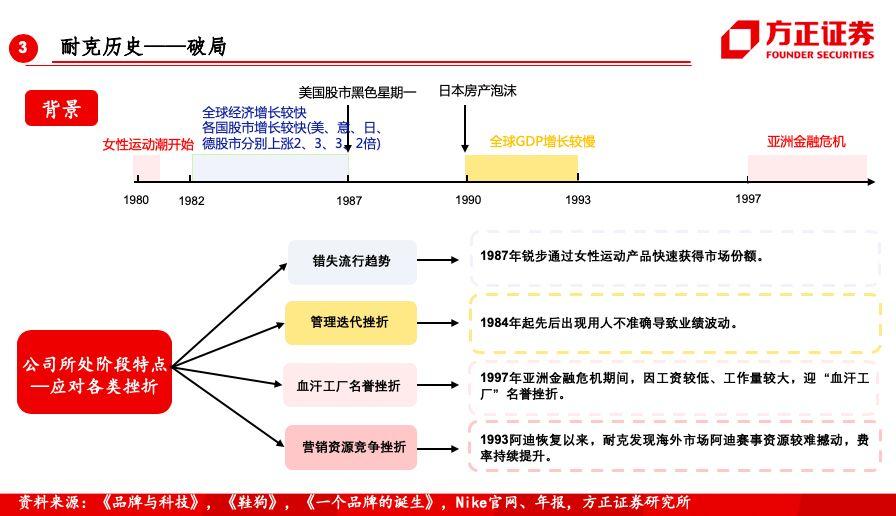

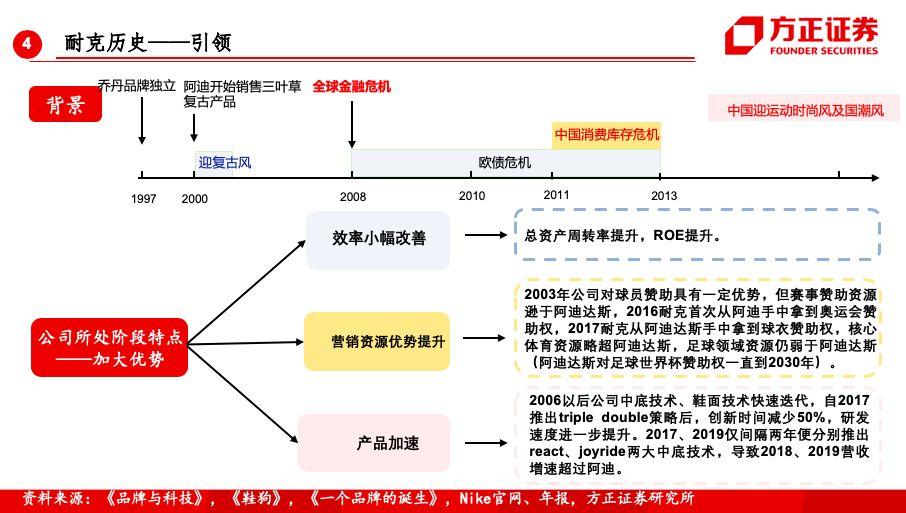

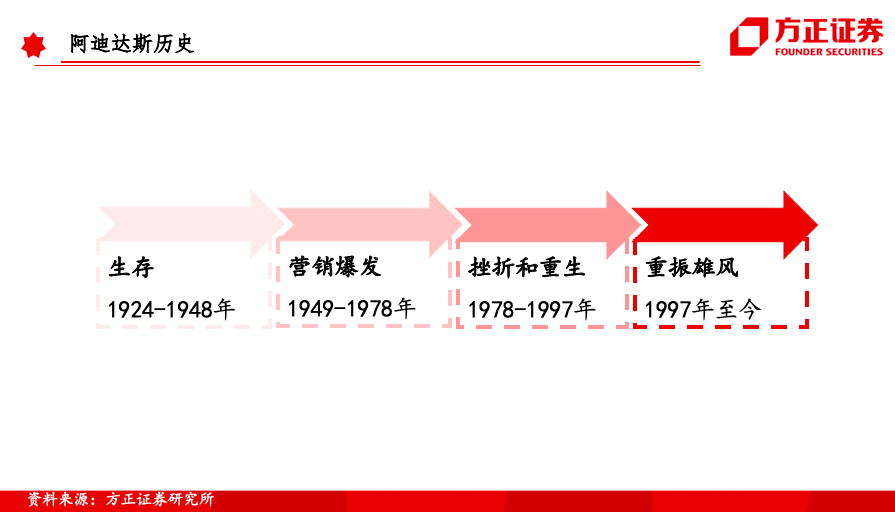

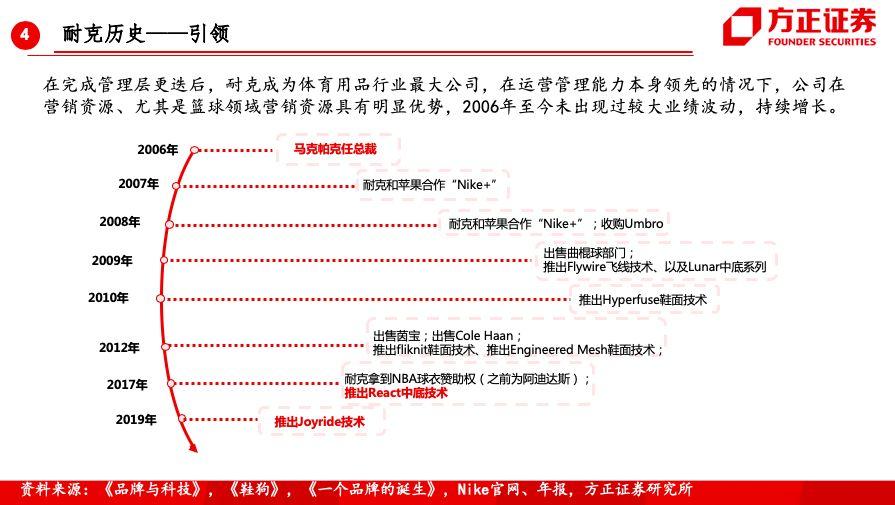

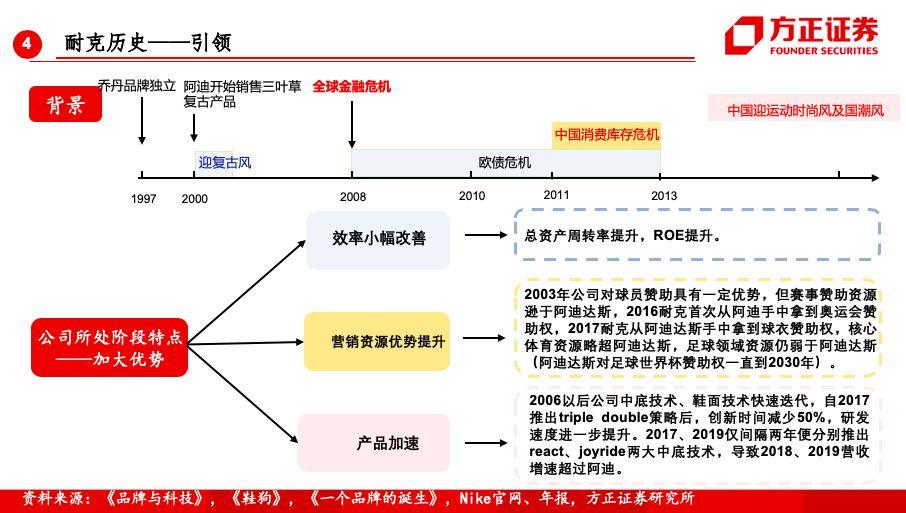

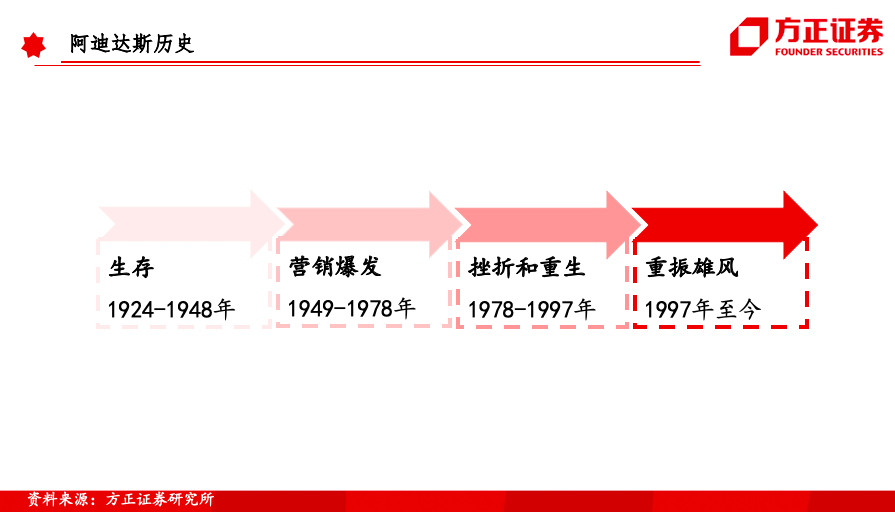

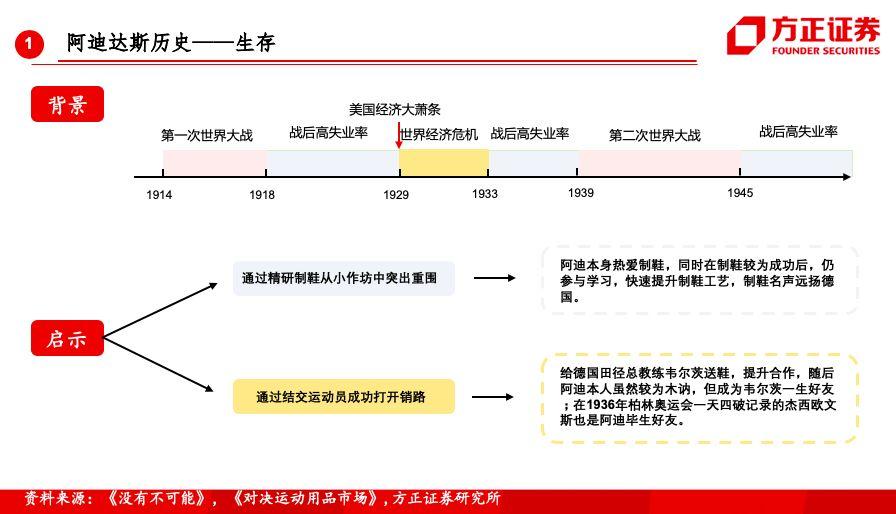

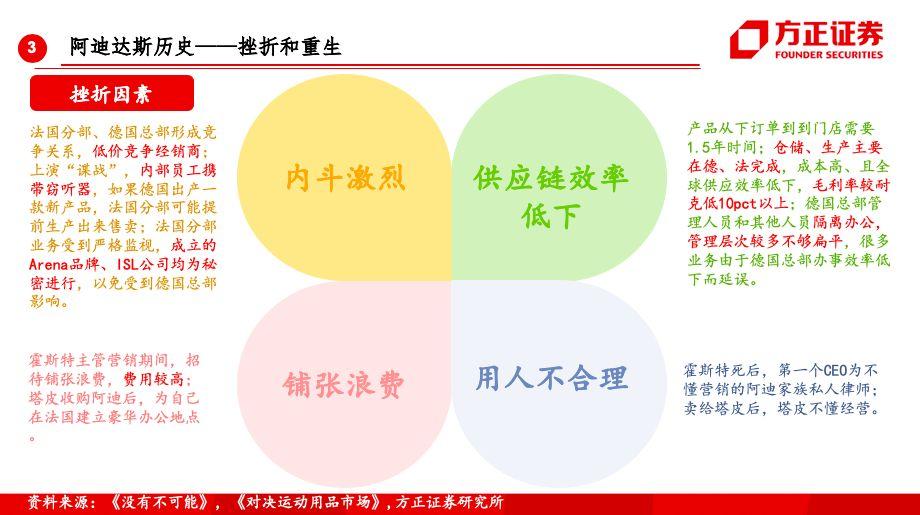

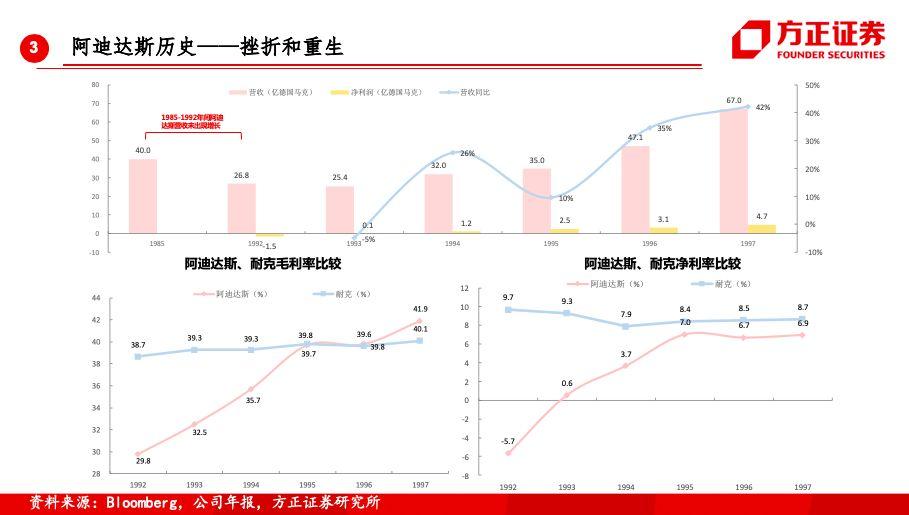

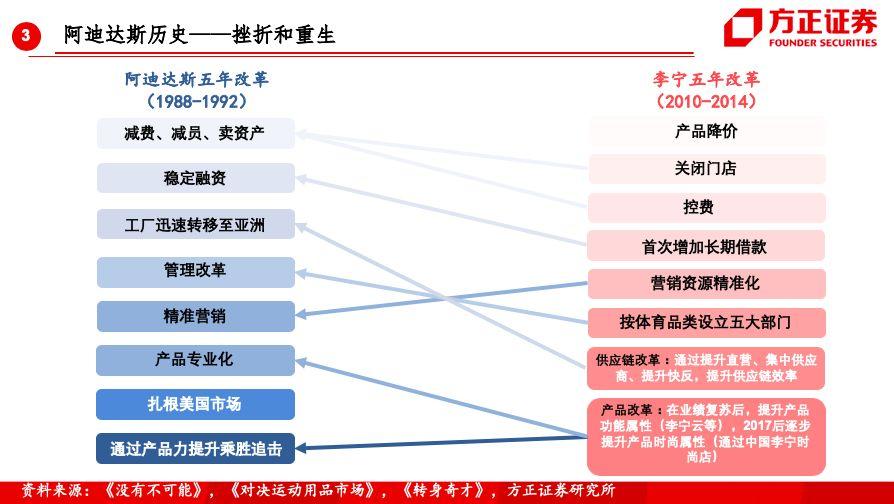

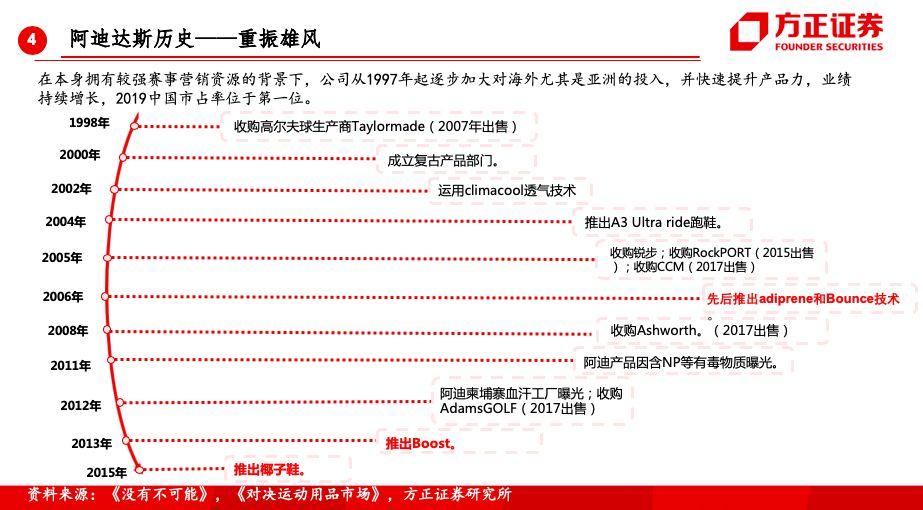

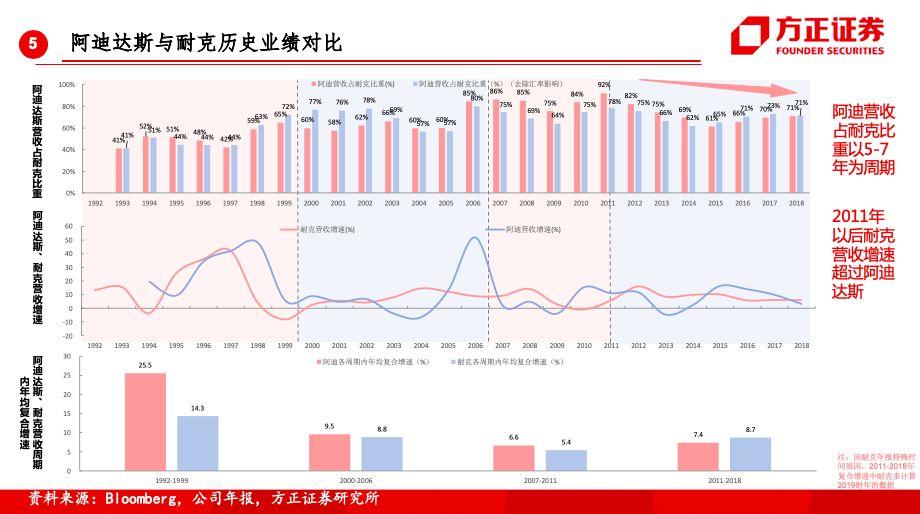

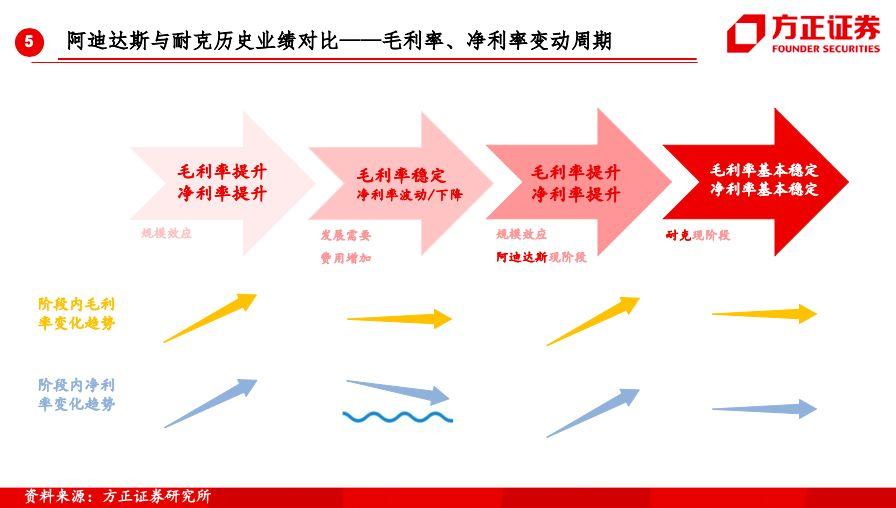

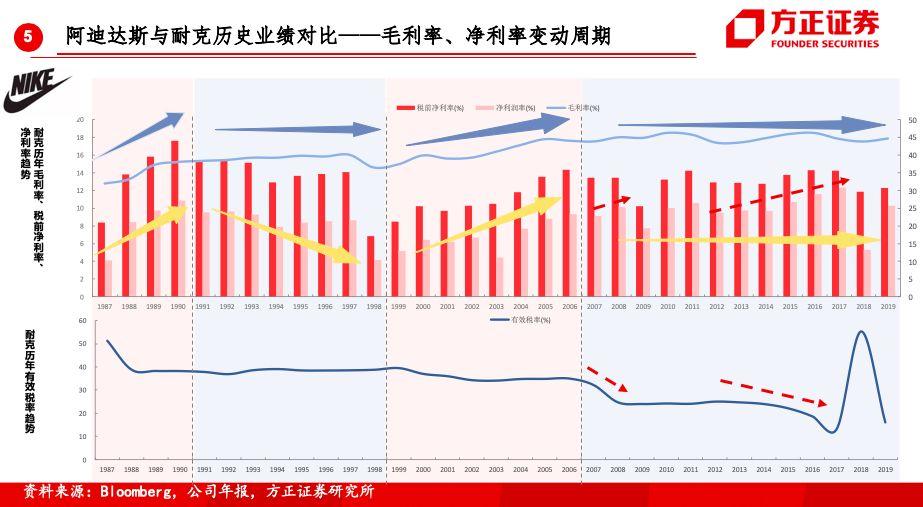

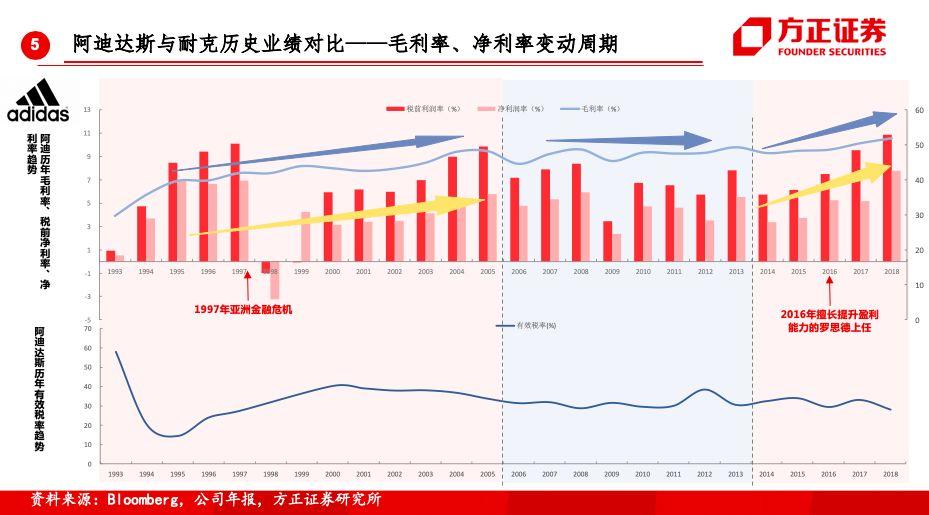

3.耐克VS阿迪:超越与重生。

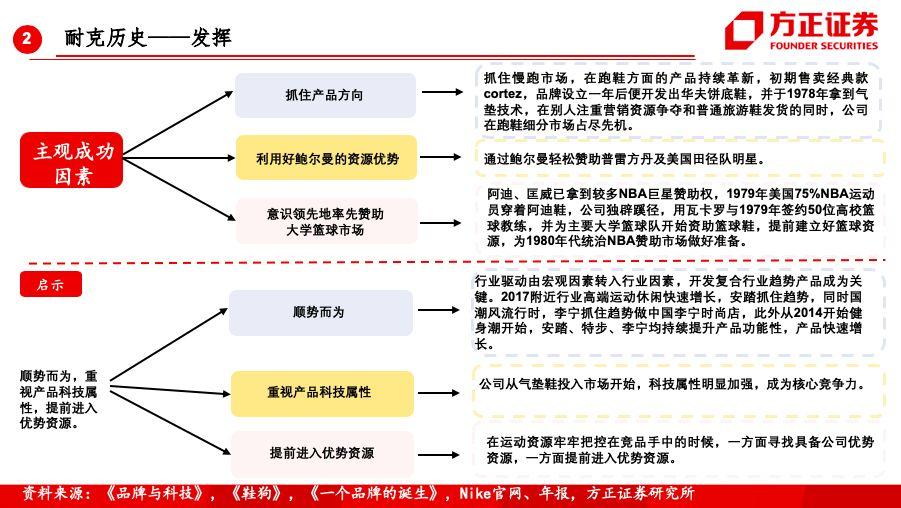

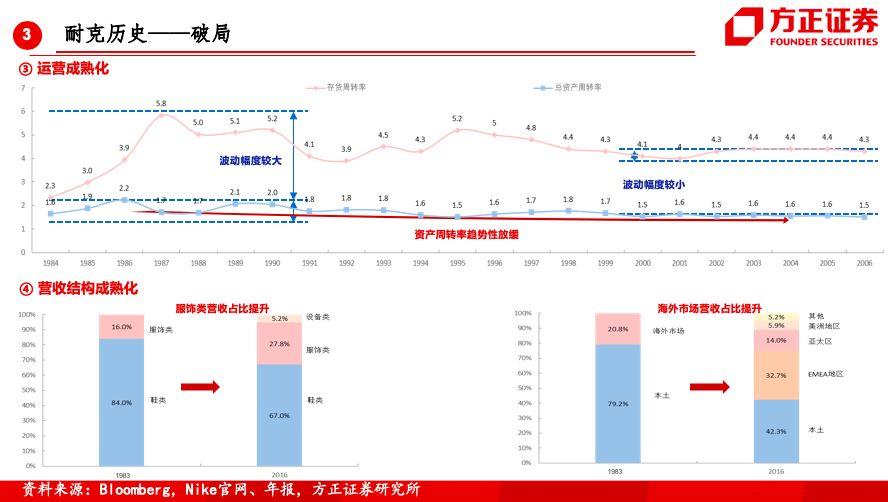

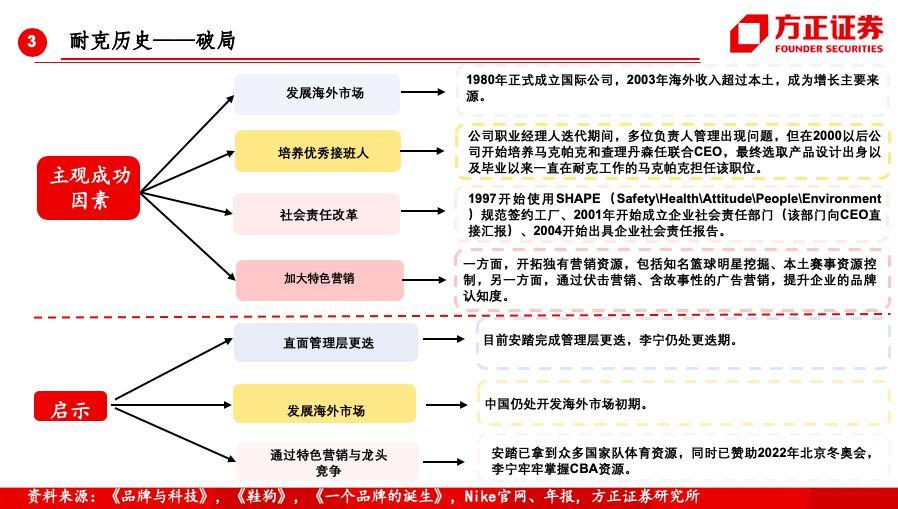

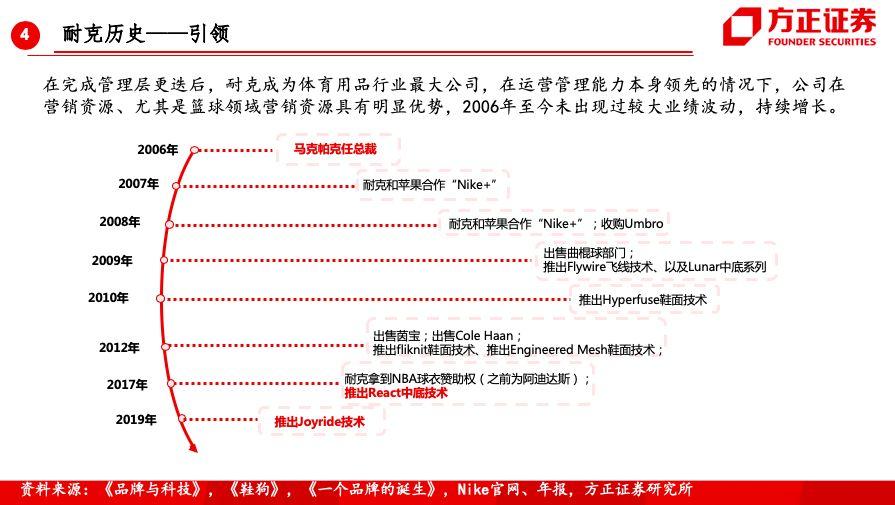

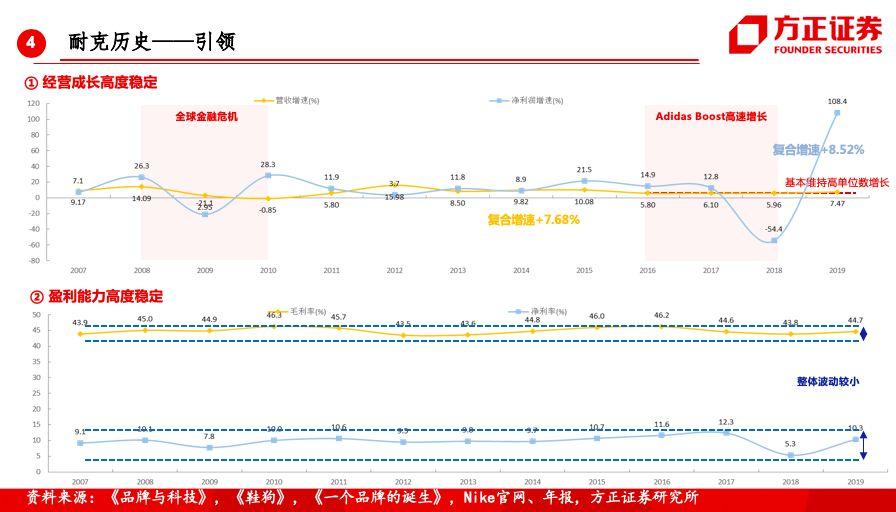

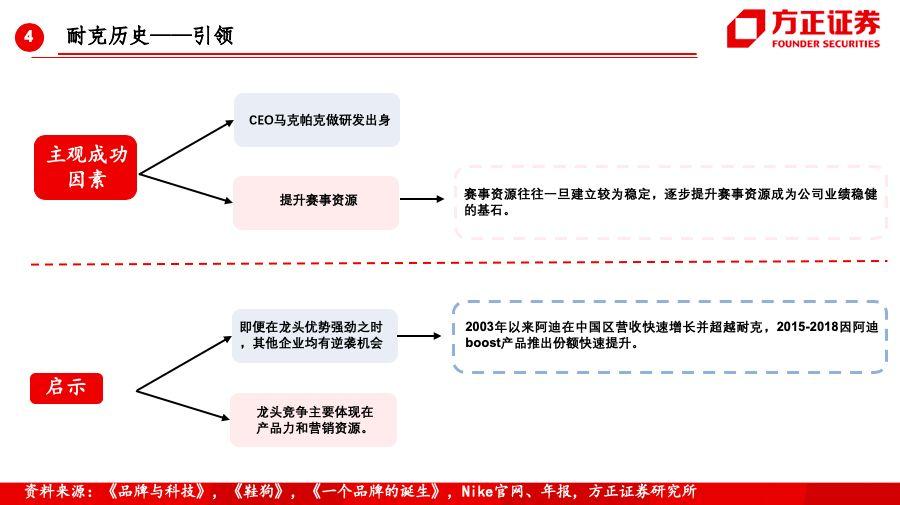

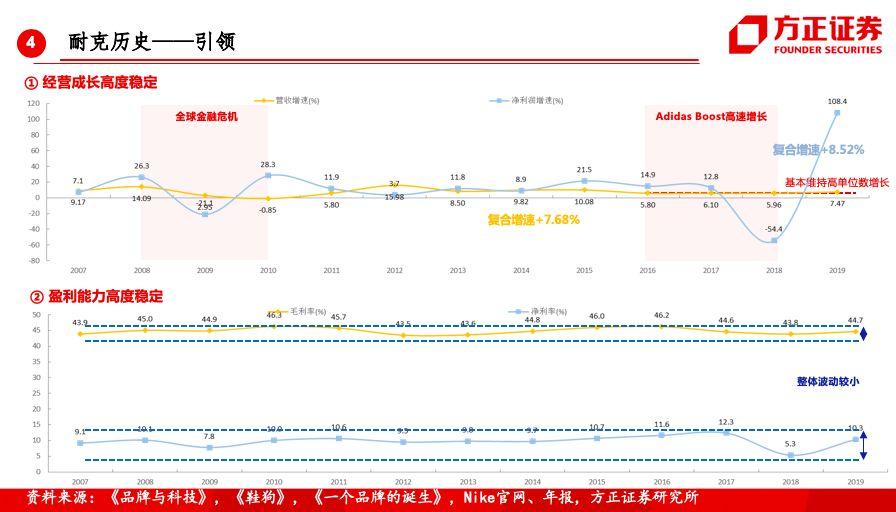

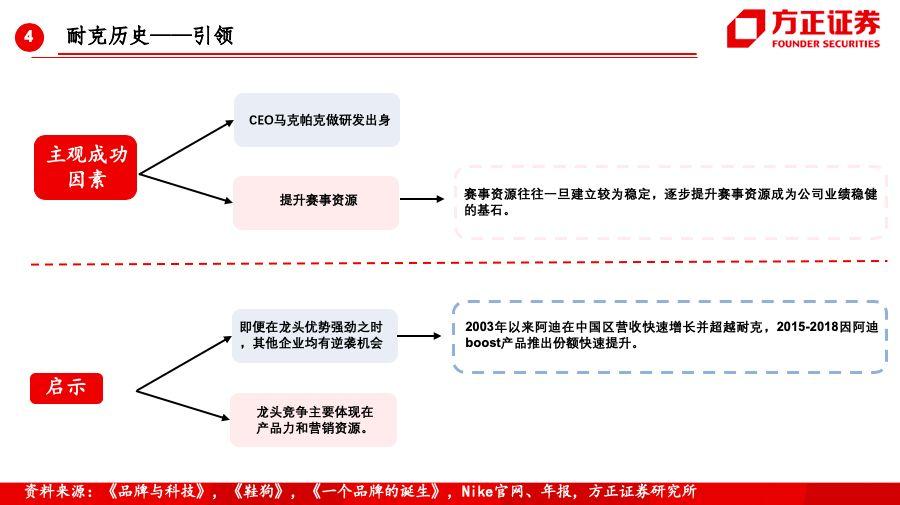

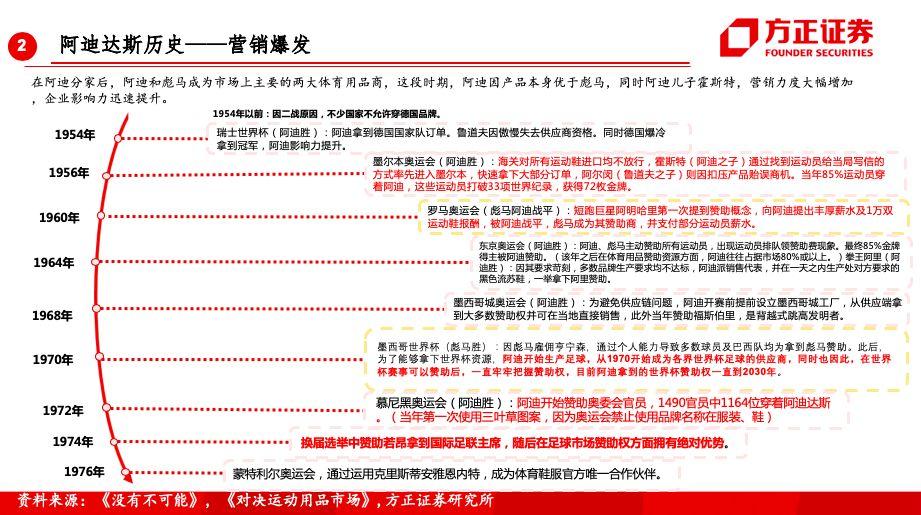

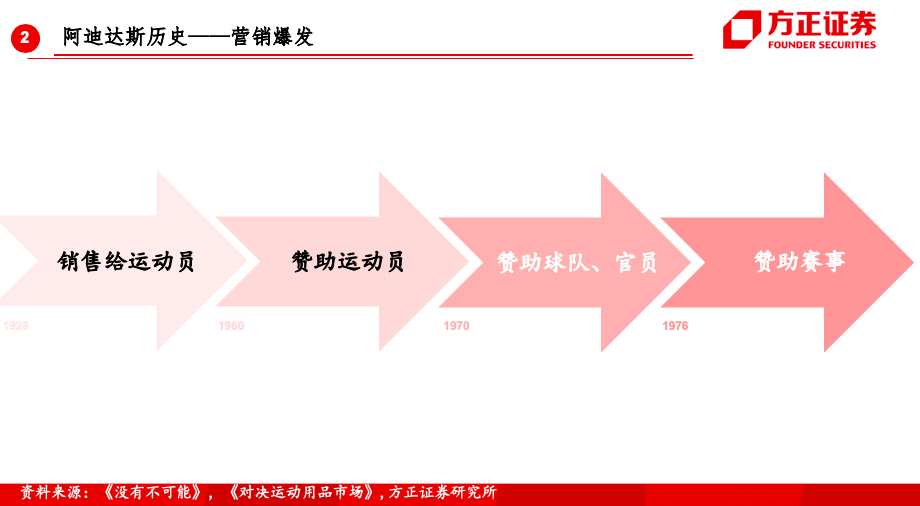

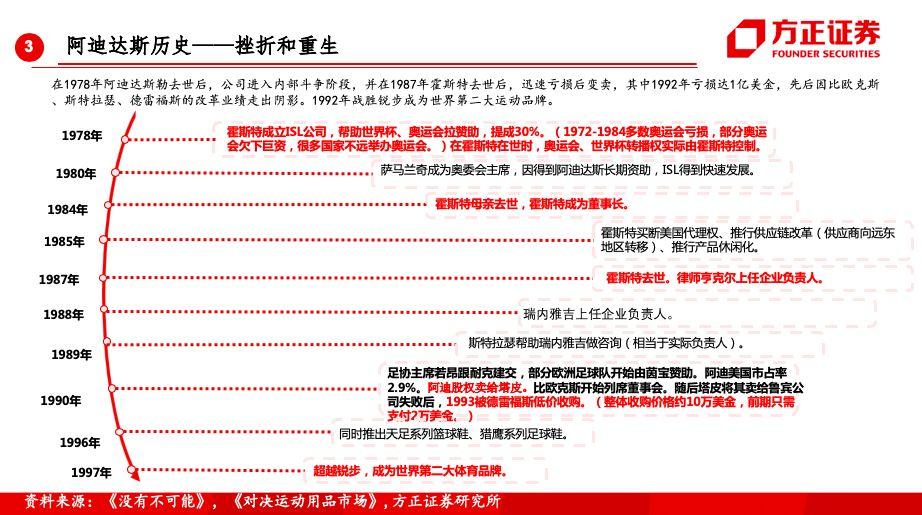

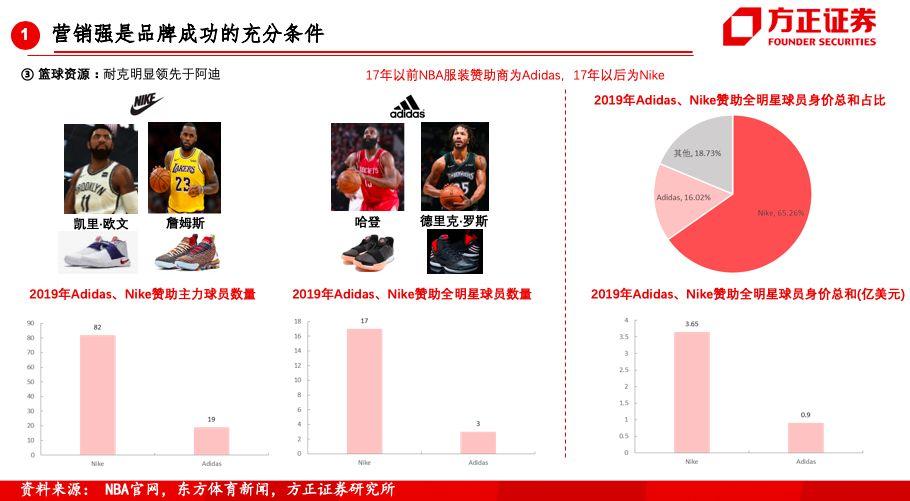

①产品力成为耐克超越阿迪核心因素,营销资源成为阿迪死而复生的关键,运营成熟及研发加速带动耐克在成熟期持续拉开与阿迪差距,盈利提升带动阿迪迎头赶上。②耐克、阿迪分别更注重体育明星和赛事资源及分别在篮球、足球资源优势领先源自两企业发展阶段及地域。③耐克拥有更好的产品力及运营能力,阿迪则拥有较强的赛事营销资源。

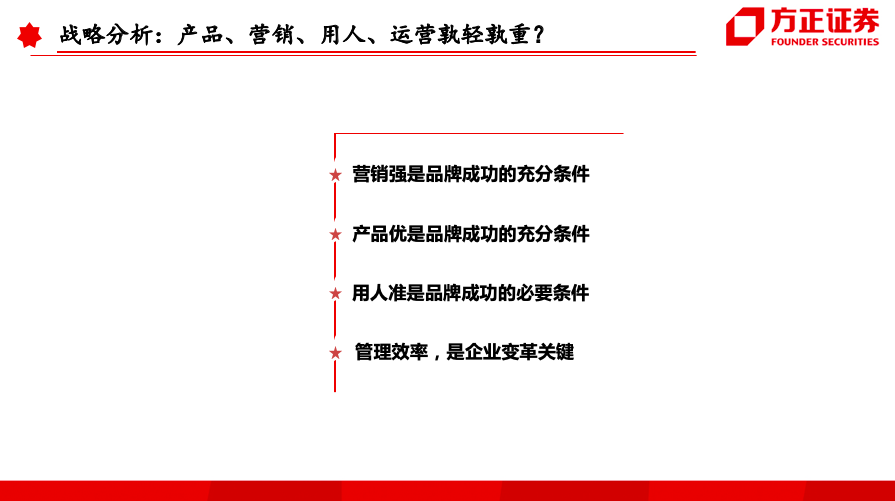

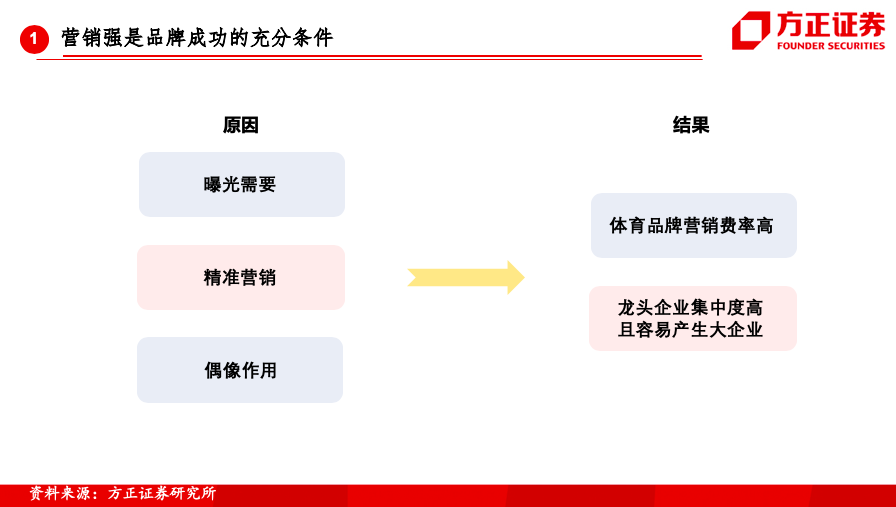

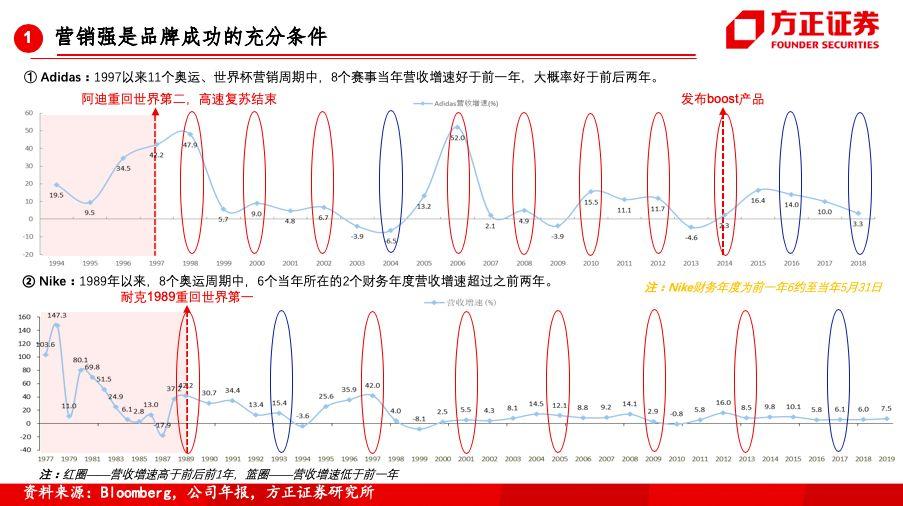

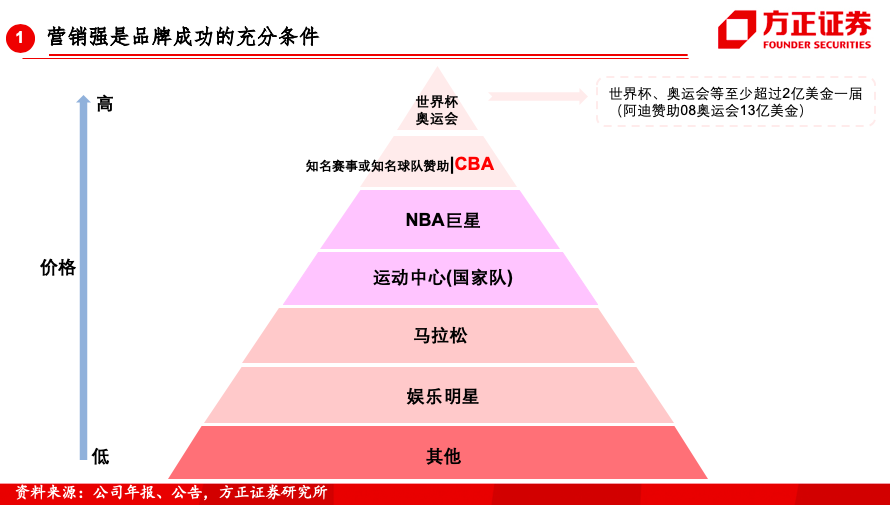

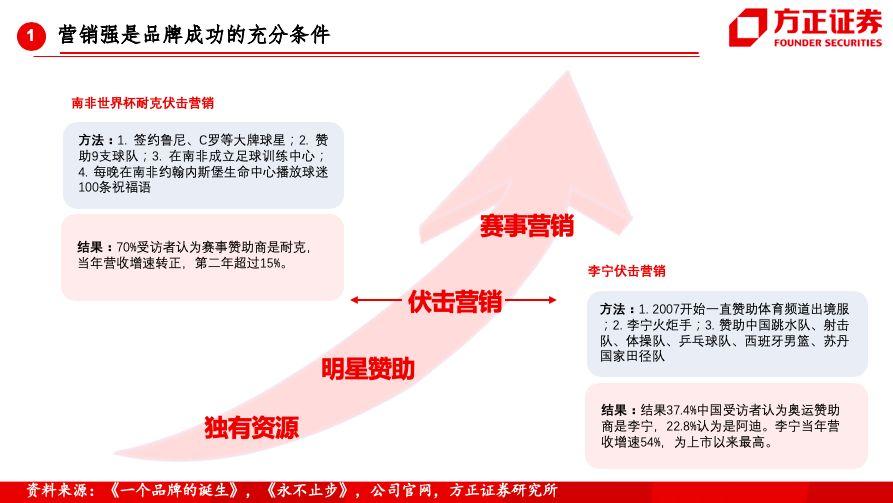

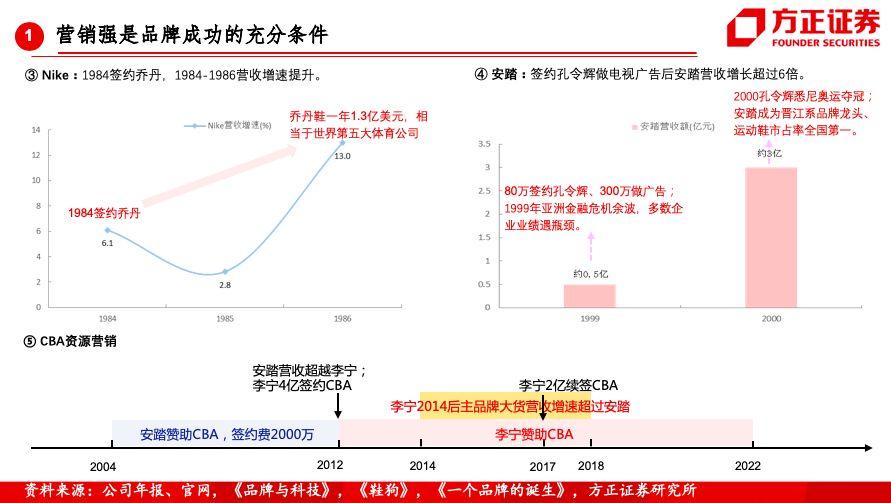

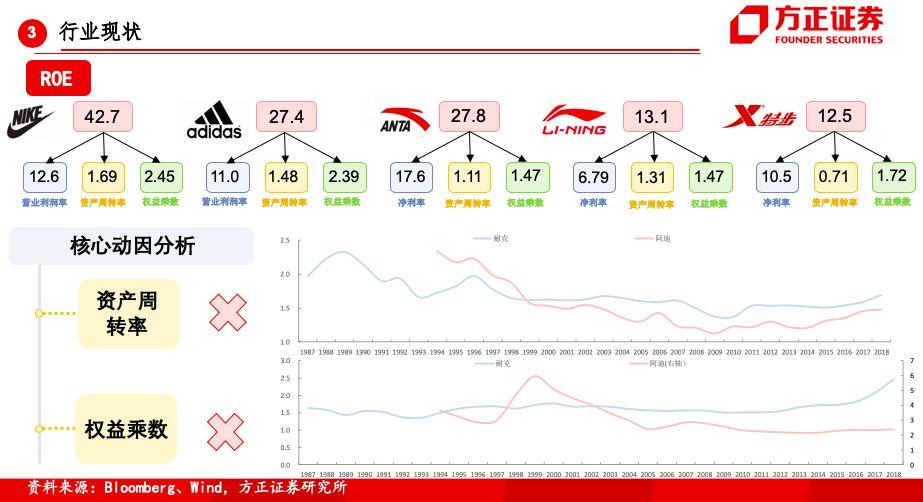

4.战略分析:产品为茅,营销为盾,运营效率并非核心壁垒。

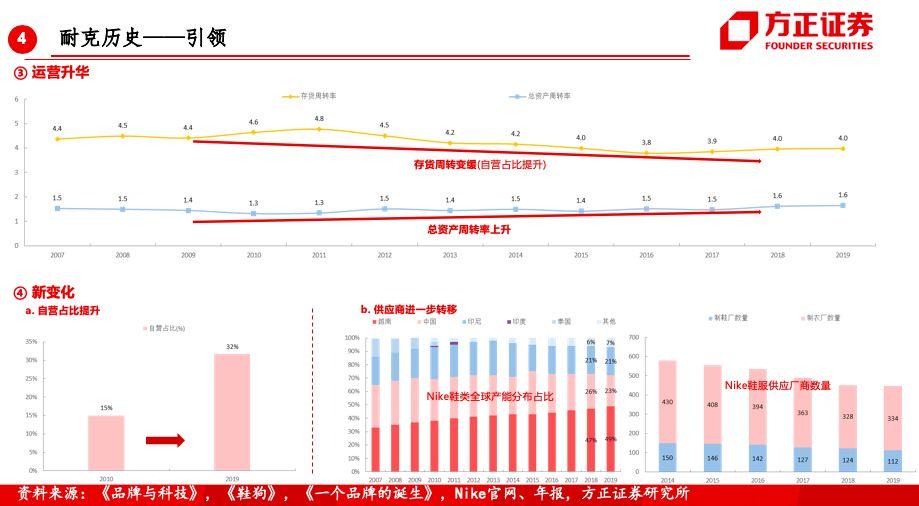

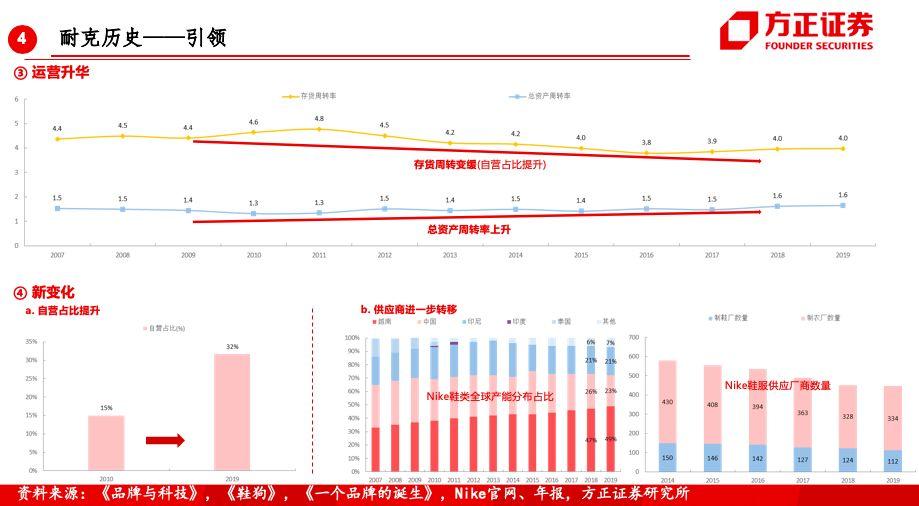

①低SKU及功能性需求导向致产品研发设计成为品牌成功最核心因素。Nike AJ系列产品营收超过所有内资品牌。②精准营销、曝光需求致营销资源争夺成为龙头竞争的主要发力点。耐克、阿迪业绩与奥运、世界杯周期高度相关。③存货周转、总资产周转并非企业核心壁垒,壁垒来自于盈利能力。④霍斯特、奈特、马克帕克在体育史贡献较大,优秀管理者往往注重研发、来自内部、具有“运动”基因。

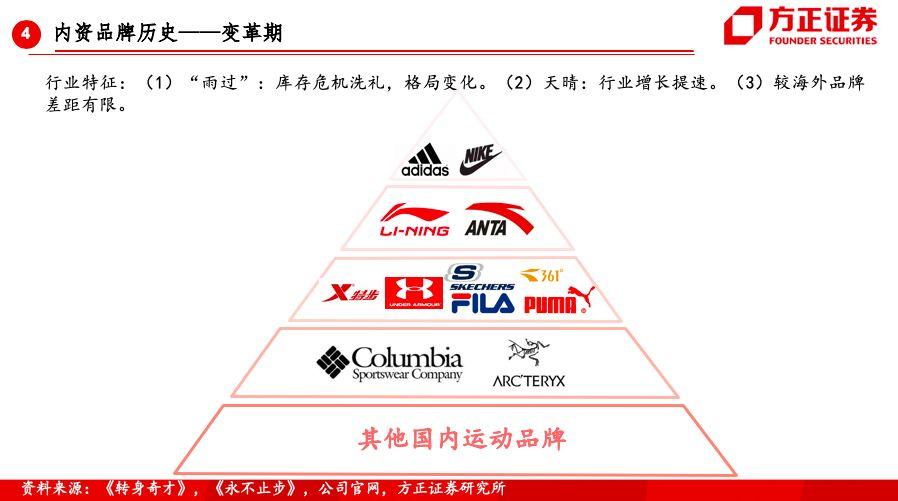

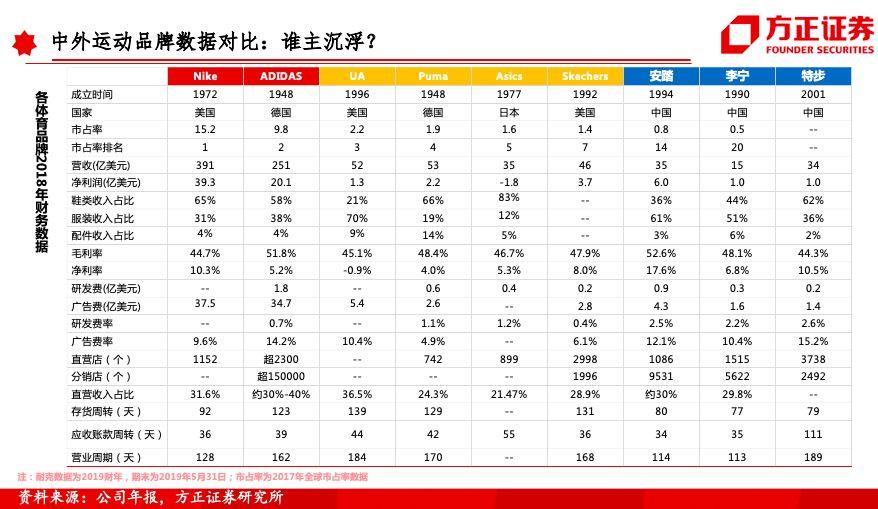

5.中国运动品牌机会:安踏、李宁、特步。

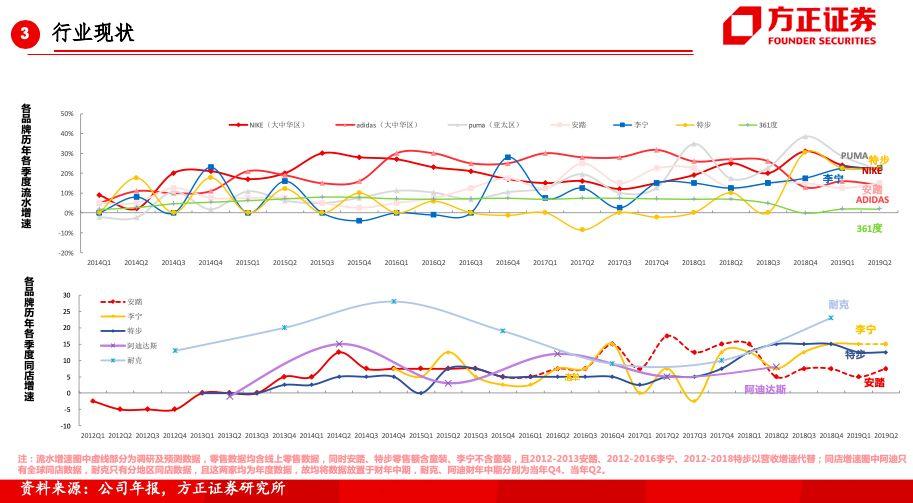

在产品功能性、海外营销资源与外资品牌有差距的背景下,内资品牌通过本土资源、娱乐资源搭建、伏击营销的方式、低价竞争的策略,在三四线城市具备优势。本土品牌拥有更高流动性、存货周转、更低管理费率,在2014迎健身潮且2017国潮风崛起并具有天然设计优势的情况下,内资品牌流水增速达到国际一线品牌水平。

风险提示:1、外资品牌对内资品牌竞争影响风险。2、内资品牌新设品牌、新收购品牌发展不及预期的风险。3、营销资源声誉、变化对企业业绩影响具有不确定性的风险。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.