Market NewsAMD Reports Strong Q3 Earnings Beating Expectations, Data Center and AI Chip Growth Drive Share Price Higher

Market NewsAMD Reports Strong Q3 Earnings Beating Expectations, Data Center and AI Chip Growth Drive Share Price HigherSanta Clara, California – November 5, 2025 — U.S. semiconductor manufacturer Advanced Micro Devices (AMD.US) announced its financial results for the third quarter of 2025, delivering earnings that exceeded market expectations. Driven by robust demand for data center and AI chips, AMD achieved significant revenue and profit growth. Following the release of its results, AMD’s stock rose sharply, closing at US$256.33, up 2.51% on November 5.

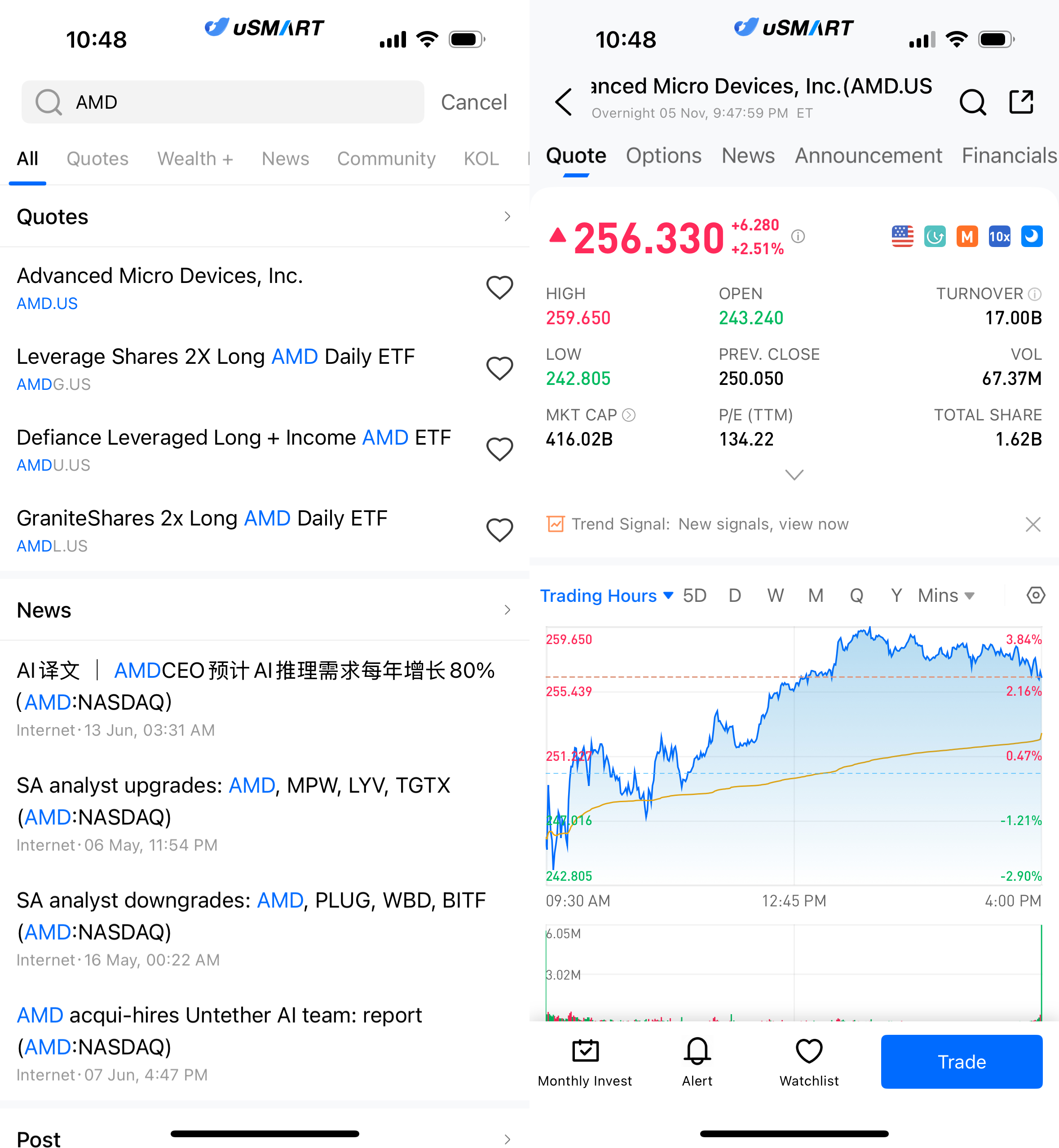

(Image source: uSMART HK app)

Revenue and Profit Surpass Market Expectations

AMD reported third-quarter revenue of US$9.246 billion, a 36% year-on-year increase. On a non-GAAP basis, net income reached US$1.965 billion, with earnings per share (EPS) of US$1.20, both surpassing market consensus. GAAP gross margin came in at 52%, while non-GAAP gross margin improved to 54%, reflecting continued optimization in product mix.

|

Indicator |

Q3 2025 |

YoY Change |

vs. Market Expectation |

|

Revenue |

US$9.246B |

+36% |

Above expectation |

|

Non-GAAP Net Income |

US$1.965B |

+39% |

Above expectation |

|

EPS |

US$1.20 |

+38% |

Above expectation |

|

Gross Margin (Non-GAAP) |

54% |

+2pts |

Stable improvement |

(Image source: AMD Q3 Earnings Report)

Data Center Leads Growth; High-Performance Computing as Key Driver

Revenue from the data center segment reached US$4.3 billion, up 22% year over year, mainly driven by solid demand for EPYC server processors and Instinct accelerators. The client and gaming segment reported revenue of US$4.0 billion, a robust 73% increase, reflecting strong shipments of Ryzen CPUs and gaming GPUs. The embedded segment saw a slight decline due to export restrictions to China.

Management expects fourth-quarter revenue to range between US$9.3 billion and US$9.9 billion, higher than the average analyst forecast of around US$9.1 billion.

Investor Sentiment Improves as AI Cycle Remains Strong

Following the upbeat results and raised guidance, multiple institutions upgraded AMD’s price targets, signaling a recovery in investor confidence. According to FactSet data, over 80% of analysts covering AMD rate the stock as “Buy” or “Overweight,” citing the ongoing expansion of AI infrastructure as a key growth catalyst. Analysts forecast that global AI chip investment will maintain double-digit growth through 2026, with AMD expected to continue benefiting from its diversified product lineup and steady shipment momentum, further consolidating its position in AI and high-performance computing.

Future Growth Drivers: AI and Data Center Remain Core Engines

Looking ahead, AMD expects growth to continue being driven by three main pillars — AI accelerators, data center CPUs, and high-end client products. The Instinct MI300 series is anticipated to become the company’s fastest-growing product line in the coming quarters. Meanwhile, the EPYC server processor continues to gain market share among cloud computing clients, potentially narrowing the gap with major competitors by 2026.

Despite ongoing export restrictions and cyclical industry risks, most institutions believe that the AI infrastructure buildout remains in an upward phase. AMD is seen to have 6–8 quarters of sustained volume growth potential, while management noted that the company has expanded its presence in non-restricted markets to maintain a steady supply of AI GPUs and CPUs.

How to Buy AMD on uSMART

After logging into the uSMART HK App, tap the search icon in the top-right corner, enter the stock code (AMD.US), and open the details page to view trading and historical information. Then tap “Trade” at the bottom-right, select the order type, enter your trading conditions, and submit your order.

(Image Source: uSMART HK app)

More Content