Market NewsEarnings Under Pressure but Funds Flow Back — Why Did Tesla’s Stock “Fall First, Then Rise”?

Market NewsEarnings Under Pressure but Funds Flow Back — Why Did Tesla’s Stock “Fall First, Then Rise”?U.S. electric vehicle giant Tesla (TSLA.US) released its third-quarter results, which initially dragged its stock lower. However, shares rebounded sharply the following day, showing a “fall-then-rise” pattern. Analysts believe that although revenue and earnings missed expectations, management’s strong emphasis on the commercial potential of Full Self-Driving (FSD) during the earnings call helped attract capital back into the stock.

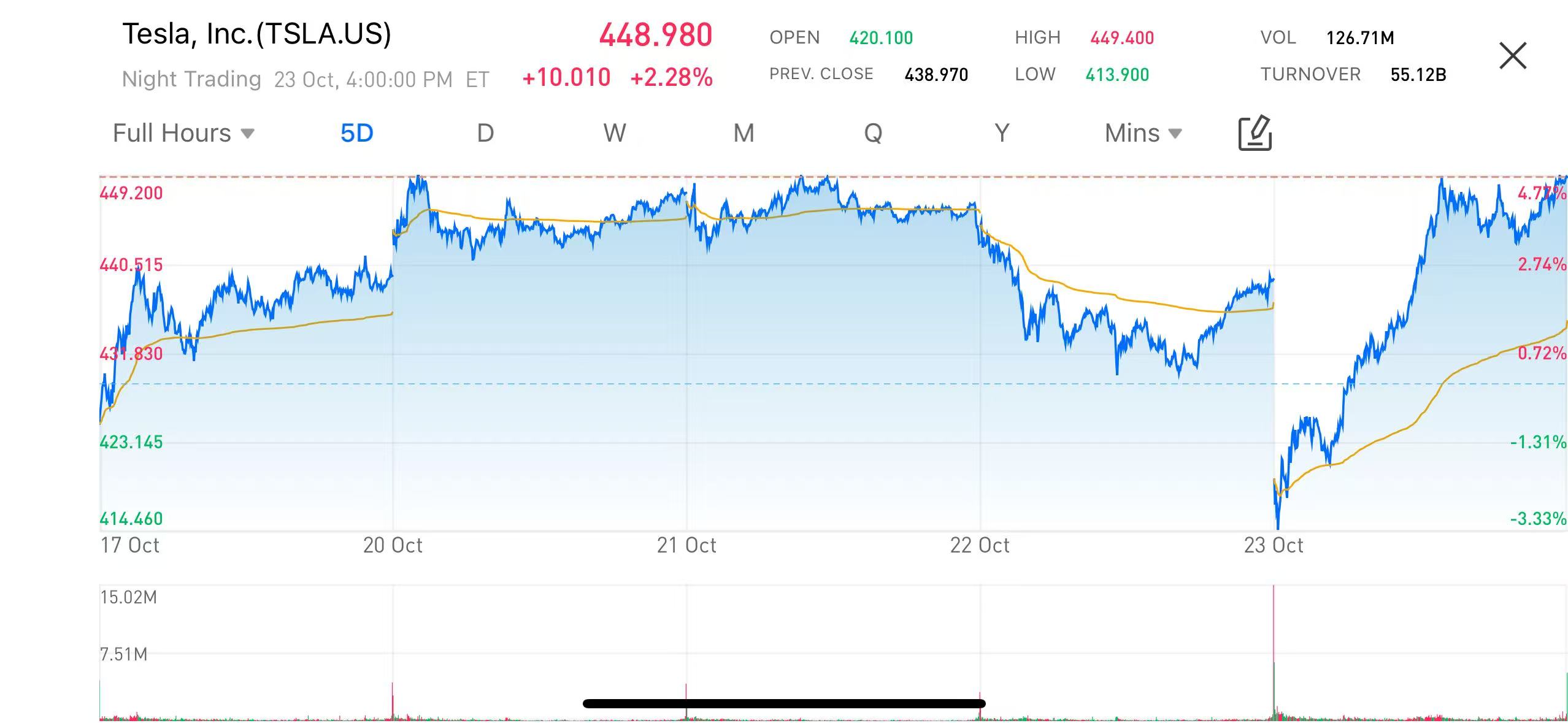

According to market data, Tesla’s share price fell to around US$414 on October 22 (earnings release day) before rebounding more than 8% the next day to an intraday high of US$448.98, signaling a notable technical recovery.

(Image source: uSMART HK app)

(Image source: uSMART HK app)

Earnings Miss Expectations, Auto Margins Still Under Pressure

Tesla’s key financial results for Q3 2025 (in USD) were as follows:

|

Financial Indicator |

第三季表現 |

市場預期 |

|

Revenue |

~US$25.17 billion |

US$25.6 billion |

|

Adjusted EPS (Non-GAAP) |

US$0.66 |

US$0.73 |

|

Automotive Gross Margin |

~18.4% |

— |

|

Free Cash Flow |

~US$660 million |

— |

(Data source: Tesla Q3 Earnings Report)

According to the report, Tesla posted revenue of about US$25.17 billion, below the expected US$25.6 billion, while adjusted EPS came in at US$0.66, missing the US$0.73 consensus. Automotive gross margin remained around 18.4%, and free cash flow dropped to US$660 million, marking a notable decline year-over-year.

Tesla cited macroeconomic weakness and high interest rates as continued headwinds for global EV demand — particularly in Europe and North America, where consumers have been delaying purchases. To stay competitive, the company maintained price cuts across major markets, further pressuring profit margins. Meanwhile, ramping up new production capacity and ongoing model updates increased R&D and capital expenditures, slowing revenue growth and triggering a short-term selloff.

Management Sends Growth Signal — FSD Commercialization in Focus

During the earnings call, CEO Elon Musk emphasized that FSD commercialization would be Tesla’s core growth driver going forward, noting the company’s transition from a manufacturing firm to one centered on AI and robotics. Musk revealed that Tesla is accelerating its FSD licensing and subscription models and may open them to other automakers, potentially generating high-margin software income.

He also highlighted that Gigafactories in Texas and Berlin are expanding capacity, and Tesla’s next-generation vehicle platform is expected to enter mass production in 2026, lowering costs further. Meanwhile, the energy storage and AI training businesses continued strong growth, with quarterly energy revenue up over 30% year-on-year.

These signals prompted investors to reassess Tesla’s growth narrative, viewing it as shifting from a hardware-centric to a software and AI-driven model. As a result, funds flowed back into the stock, driving a post-earnings rebound of over 8%, with the price reaching US$448.98.

Market Outlook: AI-Driven Valuation Re-Rating Still in Progress

In the short term, Tesla’s share price may continue to trade within the post-earnings range as investors closely monitor Q4 delivery figures and whether automotive margins can stabilize. Macroeconomic trends and pricing strategies remain key factors.

Over the medium to long term, if FSD licensing delivers stable software revenue and the energy storage and AI training businesses maintain their growth momentum, Tesla could evolve from an EV manufacturer into a mobility technology and energy platform. In that scenario, a valuation re-rating driven by AI and software compounding growth could form the core of Tesla’s next capital story.

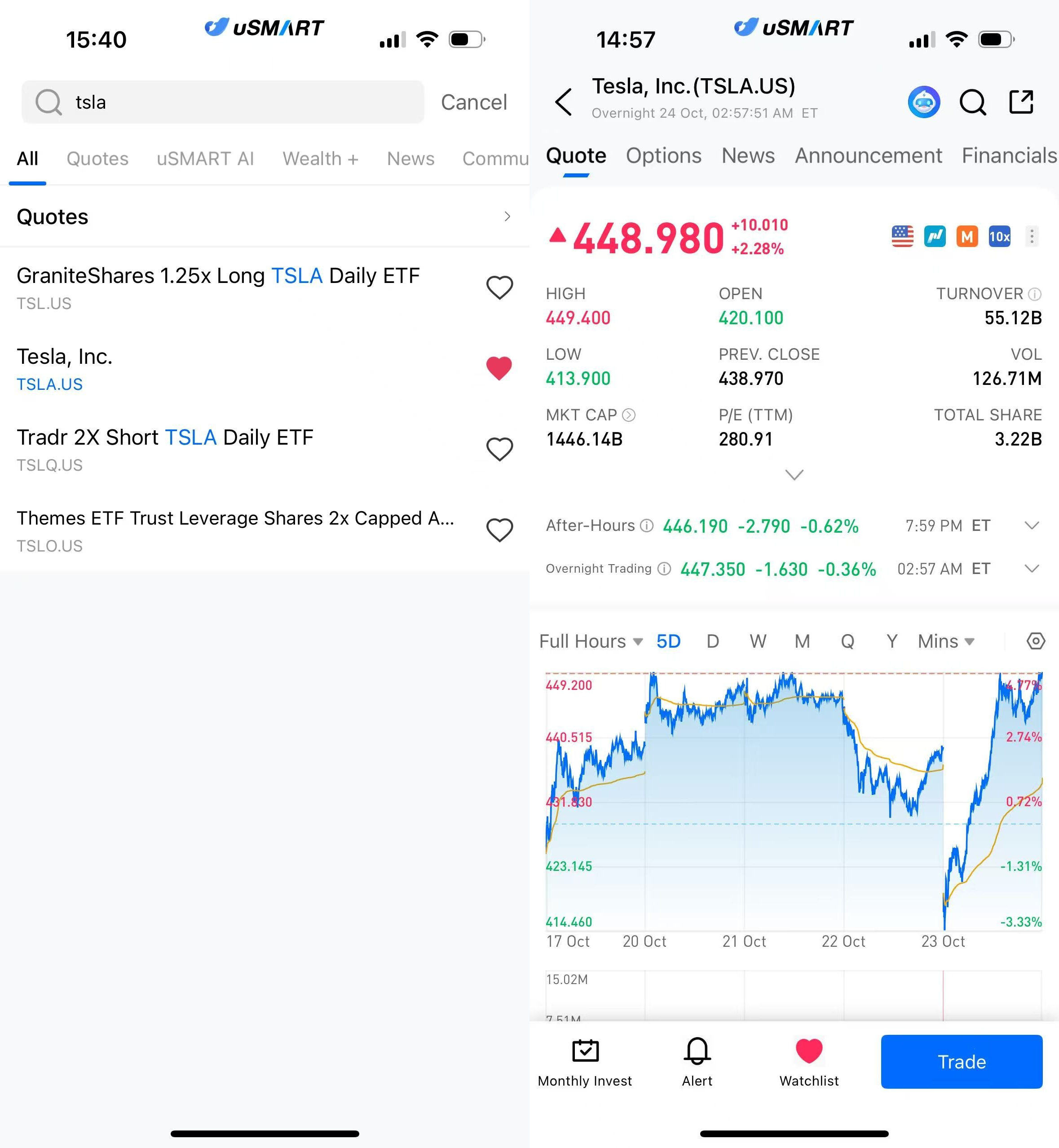

How to Buy Tesla on uSMART HK

After logging into the uSMART HK App, tap the search icon in the top-right corner, enter the stock code (TSLA.US), and open the details page to view trading and historical information. Then tap “Trade” at the bottom-right, select the order type, enter your trading conditions, and submit your order.

(Image source: uSMART HK app)

(Image source: uSMART HK app)

More Content