無緣無故就跌了。

隔夜,美股三大指數全線下挫,道指跌0.77%,標普500跌1.11%,納指一度跌逾2%,最終收跌1.49%。

令人疑惑不解跌是,昨夜並沒有發生什麼值得美股如此下跌的事情。

在新聞、數據和交易都清淡的當下,華爾街將矛頭指向了全球資產定價錨——10年期美債收益率。

1

美股下跌的矛頭

週五,美國10年期國債收益率升至4.629%,接近7個月高點。12月至今,該收益率已累計上升逾40個基點。

在美聯儲12月18日的議息會議前,美股今年已經創下了58次新高,但正是這次會議給狂熱的美股潑了一盆冷水,同時也刺激10年期美債收益率持續攀升。

美聯儲12月會議暗示明年的降息步伐或將放緩,點陣圖對2025年降息指引從此前的4次下修到2次。當天,納指下跌3.56%,標普500下跌2.95%、道指下跌2.58%。

Bespoke Investment Group聯合創始人Paul Hickey表示,如果未來幾天10年期美債收益率升破4.70%關口,可能會繼續對美股造成衝擊。

2

美股遭資金拋售?

資金也似乎改變態度了。

自11月5日特朗普贏得總統大選後,資金瘋狂流入美股,11月近1400億美元流向美國股票基金,推動11月創下自2000年以來資金流入最高的單月紀錄。

但花旗集團數據顯示,在聖誕節前的一週內,美國股票基金則流出總計266億美元,大部分來自美國交易所交易基金(ETF),遭遇387億美元的淨贖回。

美國銀行的數據也可互為佐證,過去一週,美國股市出現了約350億美元的資金外流,是自2022年12月以來的最高單週資金流出量。

另外,高盛交易部門估計,鑑於股票和債券的走勢,美國養老金將出售210億美元的美國股票。

當下,標準普爾指數股息率遠低於10年期美債收益率,上一次達到如此懸殊的對比還是2007年。

對此,市場人士提出了一個問題:在如此少股息的情況下實現年度增長的情況並不常見,2025年還能繼續嗎?

對此,貝萊德認為美股明年有望持續受益於人工智能等顛覆性趨勢的影響,加上美國經濟增長依然強勁、各領域企業盈利能力增強,這些都有望支撐美股在2025年實現跑贏全球其他市場。

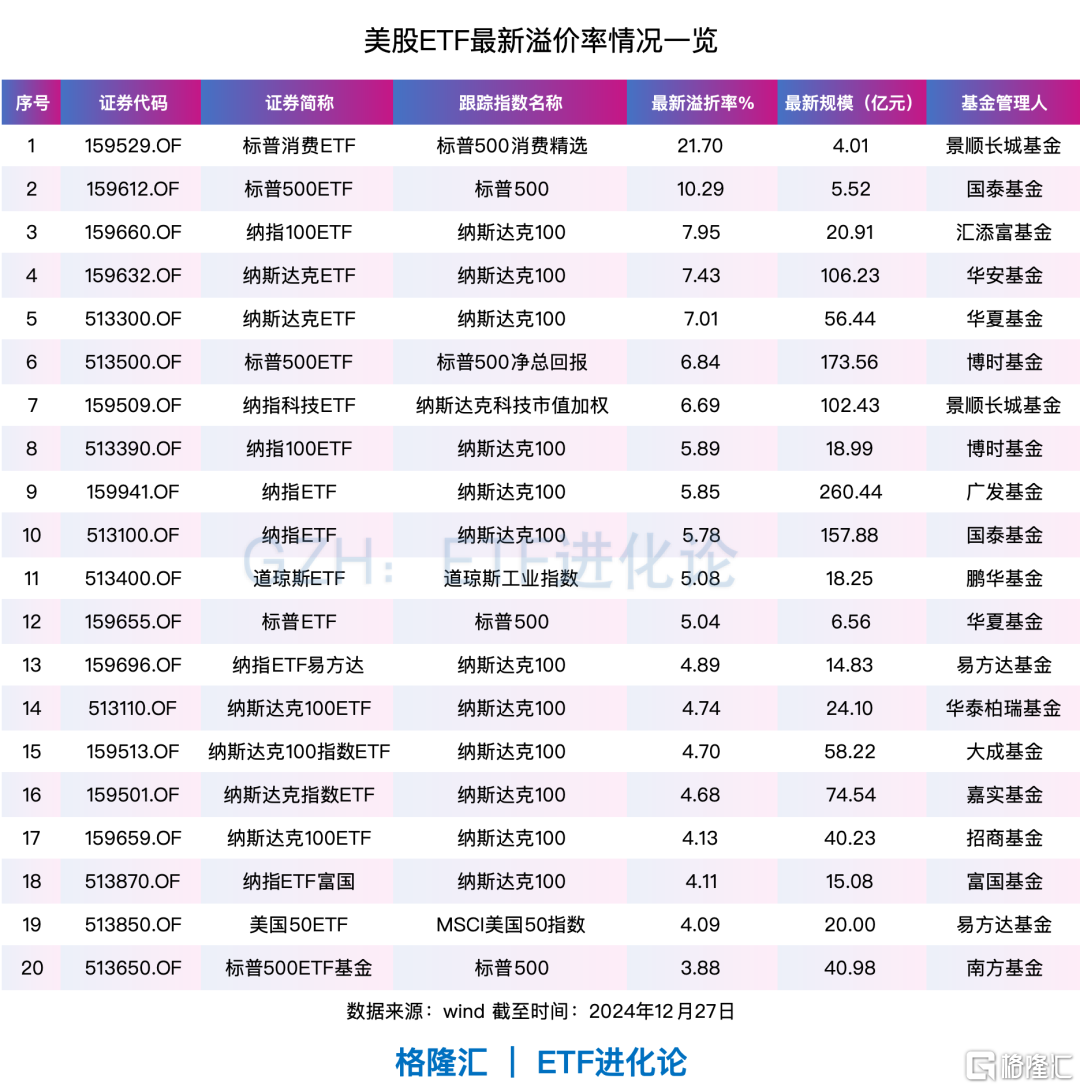

目前A股多隻美股ETF都存在溢價,IOPV溢折率超過3%的ETF有22只,景順長城標普消費ETF和國泰標普500ETF的溢價率分別為21.7%和10.29%。

(本文內容均為客觀數據信息羅列,不構成任何投資建議)

隨着投資者的熱情高升,QDII額度頻頻吿急,目前市場上有超過八成的QDII基金暫停了大額申購或直接閉門謝客。

3

基金收益率持續下行

QDII產品的高溢價率長存的現象也折射出國內資產荒的問題,更關鍵的一點是當10年國債利率進入1時代,將對資產配置的邏輯將產生關鍵影響。

12月第一個交易日,10年期國債利率跌破2%,截至12月27日,貨幣基金的7日年化收益率持續向下,多隻產品的收益率已行至新低點。

Wind數據顯示,截至12月27日,全市場364只貨幣基金的平均7日年化收益率為1.58%,較年初的2.34%下行了0.76%,多隻基金更是在月內創下了收益率新低,最低的中金財富聚金利7日年化收益率只有0.73%。

貨基還有配置價值嗎?

試想一下,在財政貨幣雙寬鬆的背景下,明年或有批量貨幣基金7日年化收益率跌破1%。

為什麼?搞清楚貨幣基金持有的資產是什麼就一清二楚了。

貨基最主要持倉主要是AAA的銀行同業存單、企業發現債券和金融債等,大頭是銀行同業存單。

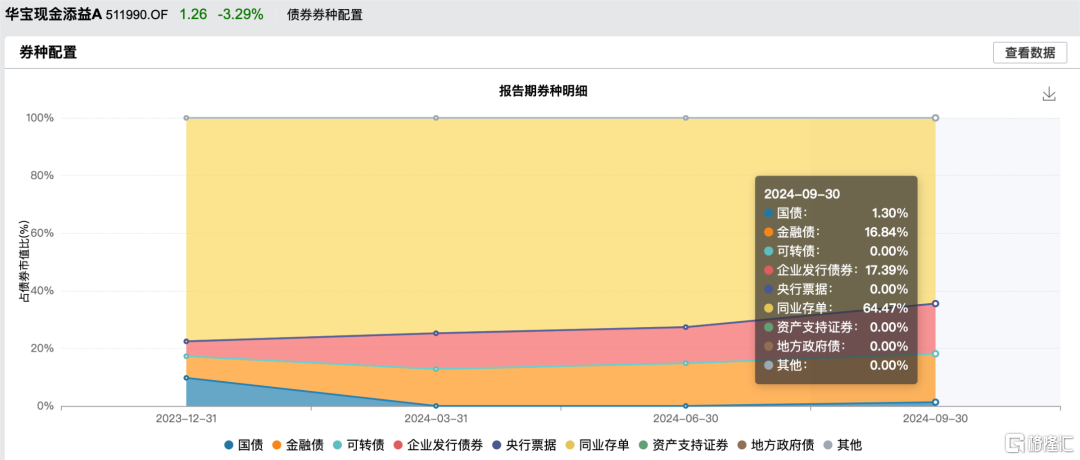

以市場規模最大的華寶現金添益為例,三季度持倉60%是同業存單。同時貨幣基金還有一個硬性規定,持有的資產平均剩餘期限不能超過180天,這意味着貨基主要持有的是短期限的銀行同業存單。

存單利率受資金利率影響大,假設降息一次幅度為20BP,OMO利率將降至1.3%,在此基礎上,同業存單利率預計將降至1.5 - 1.6%。

説一個冷知識,寬基ETF經過一波降費潮,最低的綜合費率是“管理費年率0.15%+託管費年率0.05%”的0.2%組合,但貨幣基金普遍的綜合費率高達0.4%。

底層資產1.5%-1.6%(這僅是假設降息一次的情況)減去綜合費率0.4%,收益率為1.1%-1.2%。

截至12月27日,市場規模最大的兩隻貨幣基金華寶現金添益A和銀華日利A的7日年化收益率1.26%和1.37%。

在市場提前搶跑降息預期,國債利率跌破1.7%,貨幣基金收益率持續下行的情況下,理論上,權益資產的配置價值不斷凸顯,尤其是高股息類的資產。

More Content