港股收評:三大指數均跌逾1%,內房、汽車股普跌,煤炭股逆市走強

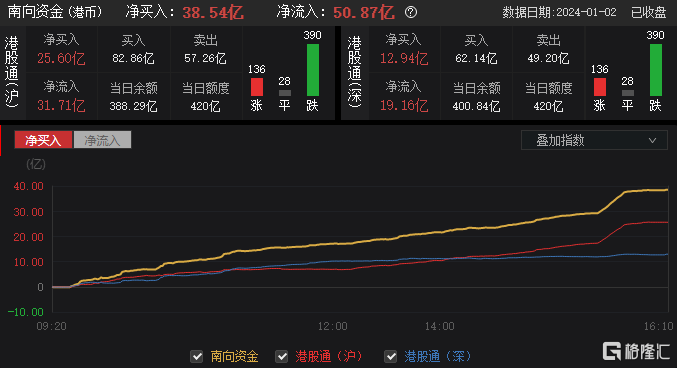

2024年首個交易日港股早盤高開低走,午後繼續弱勢震盪,截至收盤,恒指跌1.52%報16788.55點,失守萬七關口;國指、恒生科技指數分別下跌1.66%及1.32%。南下資金全天淨買入港股38.54億港元。

盤面上,汽車股普跌,蔚來跌逾6%,理想汽車跌逾5%;科技股普跌,美團跌逾3%,京東跌逾2%。啤酒股走低,華潤啤酒大跌超8%,百威亞太、青島啤酒跌超4%。內房股普跌、內險股低迷,中國平安跌超3%。生物醫藥、電力設備、光伏太陽能等板塊跌幅居前。遊戲、教育、核電、影視、黃金、虛擬現實等板塊逆勢走高。影視傳媒、遊戲股集體反彈。教育股全天強勢,卓越教育集團升超16%,思考樂教育升超11%,新東方升超5%。

具體來看:

大型科技股多數下跌,蔚來跌超6%,理想汽車跌超5%,萬國數據、美團跌超3%,京東集團、中芯國際等跟跌。

酒精飲料股普跌,華潤啤酒跌超8%,珍酒李渡、百威亞太和青島啤酒跌超4%。

據國家統計局官網,2023年1月至11月,白酒(折65度,商品量)產量累計值為395.8萬千升,同比下降6.0%;其中11月白酒(折65度,商品量)產量為46.9萬千升,同比增長7.1%。2023年1月至11月,啤酒產量累計值為3339.8萬千升,同比增長1.6%;其中11月啤酒產量為159.7萬千升,同比下降8.9%。

內房股走弱,越秀地產、龍湖集團跌超7%,世茂集團、中梁控股跌超6%,華潤置地、中國恒大、萬科企業等跟跌。

業內人士認為,1月迎來春節前淡季,房企推盤積極性不會太高,供求預期走低,考量到2023年1月基數較低,整體同比持平或微降。2024年,在宏觀經濟向好及支持政策綜合影響下,房企銷售有望築底企穩,房地產企業風險出清將提速。

煤炭股走強,南戈壁升超36%,蒙古焦煤升超11%,力量發展、易大宗、中煤能源等跟升。

消息面上,國務院關税税則委員會公佈《中華人民共和國進出口税則(2024)》税則顯示,2024年1月1日起,恢復煤炭進口關税。普通税率為20%;特惠税率為0;協定税率基本為0;最惠國税率中,無煙煤、煉焦煤、褐煤為3%,其他煤為6%。

電力板塊表現活躍,其中,華能國際電力、華電國際電力升超2%,華潤電力跟升。

12月29日,國家發展改革委體改司在廣西南寧召開全國發展改革系統體制改革工作會議。會議明確2024年重點工作任務:持續推進重點行業改革。加快全國統一電力市場體系的建設,推動電力現貨市場轉正式運行,各地要完善市場建設工作機制,做好工作協同,強化監督管理。完善綠色電力市場建設,切實推動本地區能源結構轉型。

遊戲股集體反彈,聯眾升超13%,網易升超3%,中旭未來、友誼時光等跟升。

大和發表報吿指出,國家新聞出版署12月22日意外發布《網絡遊戲管理辦法(徵求意見稿)》,震驚市場後,當局正軟化語氣,並於過去幾日採取補救措施,包括新批12月份的國產遊戲版號、與遊戲公司會面,以及對可能修改有關措施草案持正面開放態度。大和認為投資者情緒可能逐漸復甦,監管不確定性下,市場情緒可能需要一段時間才能改善。雖然修訂後的措施尚未確定,但估計實際影響程度遠小於市場反應。未來幾個月的進一步補救措施應會推動市場情緒的復甦。

個股異動

恒大汽車收跌11.76%報0.45港元,總市值48.8億港元。根據昨日公吿,紐頓集團股份認購協議及債轉股認購協議的訂約方並未同意延長截止日期。因此,紐頓集團股份認購協議及債轉股認購協議已於2023年12月31日失效。

今日,南下資金淨買入38.54億港元,其中港股通(滬)淨買入25.6億港元,港股通(深)淨買入12.94港元。

展望後市,中泰國際認為,恒指盈利預測在2023年6月底已見底回升並持續至今,除地產及原材料行業外,其餘行業的盈利預測均獲不同程度的上修或企穩。港股估值處於歷史低點,當前恒生指數及MSCI中國指數未來12個月的預測PE分別為7.7倍及9.0倍,分別處於2016年以來0.5%及 0.9%分位數。2024年全球美元流動性出現邊際改善,港股的企業盈利有望築底回升,恒生指數的估值有條件出現修復。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.