今夜,市場將再度迎來“不眠夜”,美聯儲將於北京時間凌晨3點公佈利率決議。

雖然暫停加息的結果已經大概率,但投資者還是渴望從會後聲明、點陣圖、經濟和通脹的展望、以及鮑威爾的講話中,窺得未來的降息路徑。

耶倫:正在走向“軟着陸”

當地時間週二,美國財政部部長耶倫表態稱,美聯儲抗通脹的“最後一公里”不會特別困難;美國正走在軟着陸的路上。

她表示:“在我看來,軟着陸是指經濟持續增長、勞動力市場保持強勁、通脹下降。我相信這就是美國正在走的道路。”

耶倫還表示,通脹正在“有意義”下降,在通脹預期得到控制的情況下,完成緩解物價壓力的“最後一英里”工作應該不會特別困難。

她指出:“在我們目前所走的道路上,我認為通脹沒有理由不應該逐漸下降到與美聯儲2%目標一致的水平。”

當被問及美國是否走上可持續的財政道路時,耶倫重申了之前的言論,她不認為這是一個緊迫的問題。不過,如果長期利率保持在高位,債務狀況可能會惡化。

她表示:“如果長期利率大幅高於我們之前的預期,當然會給財政前景帶來一些額外壓力。”

她認為,解決這個問題的最佳方法是提高企業和高收入家庭的税率,並加強現有税法的執行力度。

今晚有何看點?

今晚,美聯儲繼續按兵不動,已經板上釘釘,但現在最重要的是明年的降息路徑。

昨日公佈的數據顯示,美國11月CPI同比上升3.1%,符合預期,核心CPI同比上升4%,有所回升。

數據公佈後,分析師普遍認為,當前的通脹數據並不支持美聯儲快速降息。

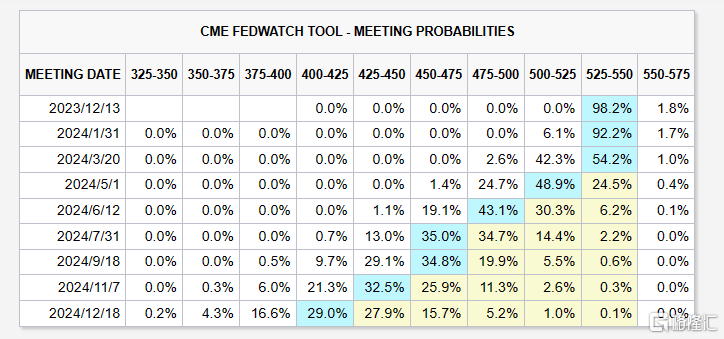

但是,市場對降息的押注卻並未發生大幅改變,市場預期明年5月開始降息,年內累計降息125基點。

對於此次會議,美國銀行的經濟學家Michael Gapen表示:“這將是美聯儲連續第三次按兵不動,在我們看來,這意味着美聯儲可能認為自己已經結束了加息週期。”

他認為,雖然未來通脹加速可能迫使美聯儲進一步加息,但“我們認為經濟更有可能降温,2024年的敍述應該轉向降息”。

結果雖然已定,但此次會議還是有非常多的看點。首先,會後聲明中,委員會對就業、通脹、住房和整體經濟增長的評估也可能會有一些措辭調整。

美國銀行認為,委員會可能會放棄提及“額外政策緊縮”,而只是表示致力於將通脹率回落至2%。

高盛認為,該聲明可能排除了有關金融狀況收緊的描述。自11月美聯儲會議以來,金融狀況(經濟變量和股市價格的矩陣)已大幅放鬆。

點陣圖,包含了美聯儲所有成員對未來三年以及更長期的利率預測的中值。上次的點陣圖顯示,官員們認為,今年將加息兩次,明年降息2次。現在市場對降息的押注依然非常激進,因此美聯儲必須謹慎傳遞信息。

LPL Financial的Quincy Krosby表示:“這將非常重要,因為股市飆升很大一部分是基於鴿派轉向以及降息即將到來。如果美聯儲默許並同意市場,即使是稍微同意,市場也會越來越高。”

與市場不同,華爾街普遍對降息偏謹慎。高盛將首次降息的預期提前至明年三季度,高盛首席經濟學家Jan Hatzius表示:“要讓他們儘快降息,需要發生很多事情。下半年(降息)比上半年更現實。”

嘉信理財的Sonders補充稱:“我並不是説這不會發生,根據目前收集的數據點,現在還為時過早。”

經濟和通脹前景展望,高盛預計,GDP將“小幅上調”,失業率和核心個人消費支出通脹將小幅下調。

鮑威爾的新聞發佈會,鮑威爾的態度可能會偏鷹。中金預計,鮑威爾或反駁市場對於明年降息的激進預期,並稱目前討論降息時機尚不成熟。當前市場已經計入了非常多樂觀的降息預期,如果美聯儲釋放更多的鴿派信號,或將導致金融條件進一步寬鬆,經濟“不着陸”和二次通脹風險加劇,這些都是美聯儲不願看到的。

More Content