Market NewsWith regard to the external pressure on copper and cobalt prices, how to examine the subsequent growth logic of Jinchuan International (02362.HK)?

Market NewsWith regard to the external pressure on copper and cobalt prices, how to examine the subsequent growth logic of Jinchuan International (02362.HK)?Since August, the price of copper has fluctuated somewhat, releasing anxiety to the market. Lengthening to the large cycle, copper prices experienced the first long upward trend after the bottom, and now the trend of copper prices tends to be volatile, in fact, the market is also waiting for the fundamentals to give a clear upward signal.

(picture: K trend of International Copper Futures Day)

(picture: K trend of international copper futures week)

After sorting out the information, the author found that the fundamentals were positive as a whole in the second half of the year.

According to previous expectations, a stronger dollar will put downward pressure on Q3 copper prices, but this is not entirely the case. Although the copper price is under pressure, it still remains in the shock range, and the anti-falling ability is sufficient. The minutes of the Fed's July meeting are too hawkish, and by Q4, the market may regain the expectation that it will stop raising interest rates, pushing copper prices higher.

At the same time, the off-season of traditional consumption of industrial metals will end in a short period of time and enter the "Golden Nine Silver Ten". This is mainly because the lower reaches of the industrial chain is responsible for economic transformation of new energy and other related consumption is about to start the peak season, then copper will benefit more.

Overseas investment banks have also stepped forward to sing more copper prices. According to foreign media reports, Goldman Sachs released a research report on July 25, raising the target price of Lun Copper for the next three months and six months to $9250 / ton and $9500 / ton, respectively. This shows that copper prices have the potential to continue to rise this year.

For investors, choosing related industries and enterprises may be a good trading window at the moment. Such as copper, cobalt, as well as upstream copper and cobalt suppliers, such as Jinchuan International (02362.HK), which recently announced interim results.

The size of cash reserves increased month-on-month, and external pressure suppression waited to be eliminated.

Let's take a look at this copper and cobalt supplier, Jinchuan International.

In the first half of 2023, Jinchuan International recorded revenues of $327 million and a gross profit of $28.389 million, according to Gongyi. While the business is steadily advancing, the Group has bank balances and cash (including bank deposits) of US $129 million, compared with US $89.7 million in the second half of last year. The Group has more abundant funds to withstand the impact of the macro environment.

In terms of net profit, Jinchuan International fluctuated in the first half of 2023 compared with the first half of last year, changing from a profit to a small loss of-$10.038 million.

Officially, this is mainly due to the continued decline in commodity prices of copper and cobalt, delays in the sale of cobalt products, impairment losses on cobalt inventories, exchange losses resulting from the depreciation of the Congolese franc and rising production costs.

The decline in copper and cobalt metal prices in the first half of the year led to a decline in net profit, which can be said to be a common problem encountered by the industry.

The data show that in the first half of this year, the average benchmark price of copper on the London Metal Exchange was $8704 per tonne, down 11 per cent from the average benchmark price of $9756 per tonne in the first half of 2022. The average benchmark price of cobalt was reported at $15.40 per pound, down 58 per cent from the average benchmark price of $36.70 per pound in the first half of 2022.

Not long ago, Hanrui Cobalt disclosed that its semi-annual net profit was 65.9508 million yuan, down 78.39% from the same period last year, mainly due to the decline in the price of cobalt metal. Tengyuan Cobalt previously disclosed the record of investor relations activities, pointing out that the cobalt price is now close to the mine cost price, and that it is unlikely to fall sharply.

For Jinchuan International, through the financial results, it can be found that the group's response is to slow down the sales strategy to slow down and accumulate more cobalt inventory, waiting for cobalt prices to pick up before selling.

In the first half of this year, the mining business produced 1364 tons of cobalt, down 48 per cent from the first half of 2022, while selling only 172tons of cobalt. This means that if cobalt prices pick up and sales resume, the revenue from this part of cobalt inventory will be reflected later.

Therefore, after the current performance, Jinchuan International, once the external pressure, the performance is basically negative, the potential is expected to be further magnified and tapped by the market, and then show the real value.

In fact, Jinchuan International has always had the advantage of high-quality copper and cobalt resources, which is the scarcest on this track. Backed by Jinchuan Group, the world's leading copper and cobalt miner, Jinchuan is its only overseas listing platform and a mature copper and cobalt miner rarely seen in the Hong Kong stock market.

The company owns five copper and cobalt metal resources mines in Africa. For example, the Kinsensa mine, one of the world's highest-grade copper deposits, produced about 15843 tonnes of copper in the first half of this year, up 20 per cent from about 13235 tonnes in the same period last year.

(photo: Jinchuan International Mineral Resources introduction, Source Haitong International)

It is worth noting that the operation of the Musonoi mine is expected to be achieved in the short term, and the mine is expected to begin stand-alone commissioning by the end of 2023.

It is understood that the mineral copper resources are 1.085 million tons, copper reserves are 606000 tons; cobalt resources are 363000 tons, cobalt reserves are 174000 tons, and the grade is as high as 0.9%. According to the feasibility study, the service life of the mine is about 19 years, roughly based on the normal mining capacity, the average annual copper mining reaches 31900 tons (606000 tons / 19 years).

By comparison, the Ruashi and Kinsenda mines already in operation have copper reserves of 299000 tons and 221000 tons, respectively. This means that when the Musonoi mine is fully operational, it will significantly increase the company's copper and cobalt production and boost the group's market position among global copper and cobalt suppliers.

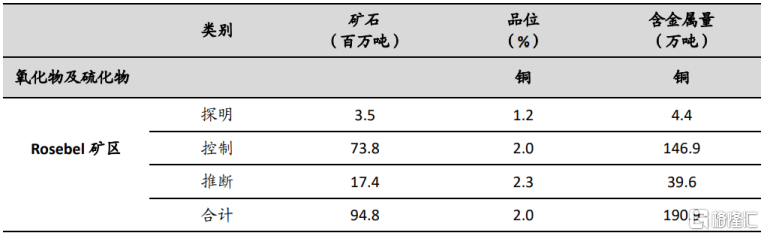

In addition, the company has made steady progress in the Lubembe project, which has raised most of its mineral resources from the inference level to the control level by the end of 2021 and is now in the feasibility stage.

(figure: Lubembe mineral resources, source Haitong International)

Generally speaking, for Jinchuan International, two points can be made clear:

First, the internal operation of the company is actively responding to external pressure, while making intensive efforts to distribute production capacity, the quality of the company still exists; second, if the influence of external pressure is eliminated, the price of copper and cobalt is very low. The performance of copper and cobalt and related companies will be optimized.

So how will the price of copper and cobalt perform in the long run?

Copper metal: inventory is low, long-term supply and demand gap will support copper price

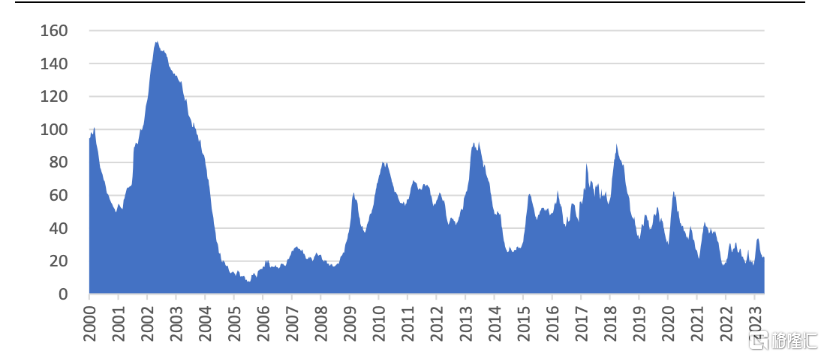

As we all know, as an industrial metal, the price of copper is determined by both "financial attribute" and "commodity attribute". Behind the "financial attribute", there are many influencing factors, such as the expectation of the Federal Reserve to raise interest rates and the weakening margin of economic data, which is also the reason for the recent decline in copper prices.

However, the expectation that the market will regain the cessation of interest rate hikes may come soon. According to CME's FedWatch forecast, the Fed may start to cut interest rates next year, and a weaker liquidity easing environment for the dollar is just around the corner. Recently, the Goldman Sachs team expects the Fed to start cutting interest rates in the second quarter of next year and gradually cut rates on a quarterly basis since then.

(figure: Fed interest rates and copper prices)

When the negative impact of "financial attributes" is weakened, copper will certainly return to supply and demand in the long run.

On the demand side, although the stable demand for copper still comes from traditional industries, it is well known that the sustained high boom in the new energy industry is the main driving force for the growth of copper consumption. China is in the process of economic transformation and upgrading, and the development of electric power and new energy will further increase the long-term demand for copper.

Combined with the current inventory of copper and the layout of new mines, copper supply may not be able to cope with long-term demand, resulting in a "supply-demand gap" of copper metal. This means that copper suppliers with sufficient and high-quality production capacity in the future will become "resources" that downstream customers are eager to compete for.

Indeed, at present, the global copper explicit inventory is still at a low level.

According to the statistics after August 18, the global copper inventory is 212600 tons, an increase of 10900 tons from the previous month, a decrease of 75800 tons over the same period last year, and the explicit inventory of copper continues to be eliminated. Looking back from 2018 to the present, from the trends in the chart below, we can see that copper inventories as a whole are showing a downward trend.

(photo: global cathode copper inventory compared with the same period last year, source of Huafu Securities)

(picture: LME+COMEX+SHFE copper inventory, per 10,000 tons, source Haitong International)

At the same time, on the basis of low inventory, there is also a situation of "insufficient production of new mines and accelerated production reduction of old mines" in the industry as a whole, and the subsequent supply of copper will undoubtedly be suppressed.

According to S & P data, only 16 large copper mines were discovered in the world from 2010 to 2019, totaling 81.2 million tons, accounting for less than 1/10 of the resources in the past 30 years, while copper exploration expenditure has not declined significantly in recent years. The cost of resource discovery per ton is much higher than in the previous 20 years.

(figure: decline in reserve taste and recoverable life of global copper mines)

At present, among the major producing countries, Chile has experienced uncertain risks such as declining ore grade and tax policy adjustment, which this year reached its lowest monthly output since 2017. Peru has only just begun to alleviate the commissioning of new mines and community problems in some old mines after a three-year long period of capacity recovery. All these will make the actual supply of copper in the future less than expected.

A number of institutions have expressed a similar view, with analysts at Rystad Energy predicting that the supply shortfall will widen to 14 million tonnes by 2040, with even a "best-case" shortfall of more than 5 million tonnes.

From this point of view, Jinchuan International will benefit from the long-term "gap between supply and demand".

On the one hand, it comes from production. Combined with Bloomberg data, some institutions predict that the new production capacity of mineral copper will accelerate its decline, and the new production capacity of mineral copper from 2023 to 2025 is expected to be 78.3 Universe 49.3 / 287000 tons. Taking the Musonoi mine that Jinchuan International is about to start operating, Jinchuan International will contribute more than 11% of global production capacity in 2025, based on an average annual copper mining of 31900 tons.

On the other hand, it comes from price. In the long-term low inventory, the role of inventory as a cushion between supply and demand will be greatly weakened, which means that once the supply and demand further improve, the price elasticity will be significantly larger. Under the long-term "supply and demand gap", copper prices may usher in its upward cycle.

For Jinchuan International, as a supplier of high-quality copper, it is expected to be positively influenced by the logic of "simultaneous rise in quantity and price" of copper metal for a long time, and reap the long-term potential of certainty.

Cobalt metal: the terminal demand continues to pull, and the price will be low for a long time.

In the long run, cobalt is expected to beat today's low prices because of the deterministic demand for cobalt in the future.

The upstream of cobalt industry includes cobalt mining, secondary recovery of cobalt-containing waste and other links. The middle reaches are cobalt products, and the middle reaches have different downstream applications according to classification. The downstream applications of batteries can be further divided into three categories: 3C products (computer, communications and consumer electronics) batteries, electric vehicle power batteries and lithium battery energy storage devices.

From the point of view of terminal demand, 3C electronic consumption will be pulled again. The overall consumer electronics market is about to bottom out, in which folding screen mobile phones have become a subcategory for creating increments. According to the IDC report, the Chinese folding screen mobile phone market shipped about 1.26 million units in the second quarter of this year, an increase of 173.0% over the same period last year.

In addition to folding screen phones, there is a big potential demand for head-wearing devices. Apple's Vision Pro is expected to be launched early next year, which will start the innovation cycle of headsets, attract more manufacturers and expand the entire headset market. In addition, the battery life of the Vision Pro is only two hours, and the adaptable battery will be updated during the iteration of the headset, and the smaller size will continue to stimulate the demand for raw materials.

Of course, the largest area of end consumption downstream of cobalt metal is still in power batteries.

At present, downstream car companies prefer lithium iron phosphate batteries, resulting in temporary pressure on the demand for ternary batteries, but the capacity of large cylindrical batteries represented by 4680 is constantly climbing. The latter has higher energy density and lower cost, which is the direction choice of the new stage for automobile companies in the long run.

Tesla's second-quarter results showed that the output of the top 4680 cylindrical lithium-ion batteries at the Tesla super factory increased by 80 per cent month-on-month. According to statistics from the website, the reservation quantity of Tesla's Cybertruck has reached 1.94 million, while the total output of 4680 batteries currently produced by Tesla can only power 11500 electric vehicles. As production capacity climbs, there is still a huge demand for batteries and battery raw materials waiting to be released.

In the long run, cobalt metal can continue to benefit from innovative iterations of power batteries. In the middle reaches of the industrial chain, battery manufacturers represented by Ningde era and Honeycomb Energy continue to promote the iteration of battery technology, while the battery quality is constantly improving, and the quality of upstream raw materials is naturally high, which requires a stable and high-quality cobalt supply.

Therefore, such a deterministic long-term demand will lead to the reevaluation of the upstream enterprises and the core participants in the middle and lower reaches of the industrial chain.

Whether 3C electronic consumption is pulled again, or the growth of new energy-related industries is strong enough, it will be transmitted to cobalt metal, and its demand will be centrally released.

At present, the production capacity and output distribution of domestic copper and cobalt suppliers are steadily advancing.

Last month, Luoyang Molybdenum Industry announced that it had signed a settlement agreement with the National Mining Corporation of the Democratic Republic of the Congo (DRC) on the issue of TFM interest fund. With the smooth progress of the settlement Agreement, TFM copper and cobalt minerals will be released. According to the forecast, the average annual output of copper and cobalt is expected to be about 200000 tons and 17000 tons respectively.

Jinchuan International's Musonoi mine will also bring new cobalt capacity. According to the company's management, after the Musonoi project is put into production, the company's annual cobalt production is expected to rise significantly from 3000-4000 tons to 1.2-13000 tons. At that time, Jinchuan International will rely on higher cobalt production to meet the development of new energy vehicle market.

So in retrospect, although copper and cobalt are under short-term pressure, it must be clear that their long-term potential has not changed. For copper and cobalt suppliers, including Jinchuan International, they have a clear judgment on the trend: continue to invest in copper development and accelerate the strategic layout on a large scale in advance from now on. This is also in line with one of the major opportunities that will be seized by a high-growth copper and cobalt supplier.

Jinchuan International is on the right path, which deserves the expectation of the market.

More Content