環球一覽 | 美股強勁反彈,銀行股暴升!核心CPI環比超預期,3月加息25基點預期升温

經歷了6個交易日的下行後,昨日美股三大指數集體收升,道指升1.05%,納指升2.14%,標普500指數升1.67%。

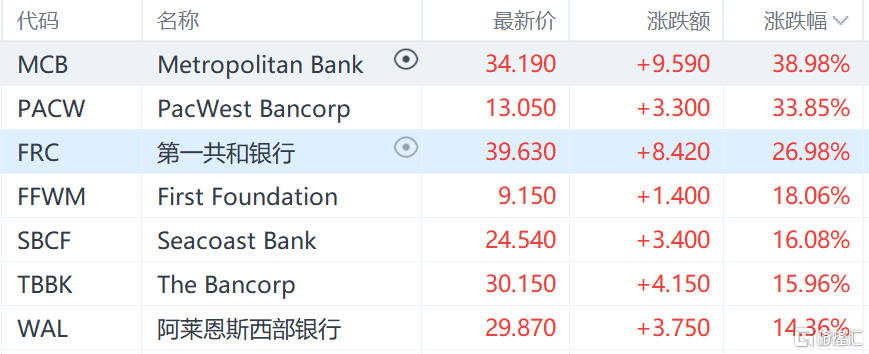

地區銀行股也開始暴力反彈,開盤後集體暴升,後雖有所回落,但許多公司收盤仍錄得兩位數升幅。第一共和銀行收升27%,盤中一度升超63%,前一日收跌61.83%;西太平洋合眾銀行收升近34%,盤中最高升77%;阿萊恩斯西部銀行收升14%,盤中最高升53%。

中概股跟隨大盤上升,納斯達克中國金龍指數升0.62%。百濟神州升逾4%,霧芯科技和唯品會升超3%,百度升超2%,小鵬汽車跌超4%,教育股普跌,好未來一度跌超22%,收盤跌10%,新東方跌逾3%。

大型科技股全線上升,蘋果升1.41%,亞馬遜升2.65%,Meta升7.25%,谷歌升3.14%,微軟升2.71%,奈飛升0.49%,英偉達升4.78%。

消息面上,有對沖基金大佬表示,美國地區性銀行“難以置信的便宜”。昨晚公佈的美國CPI同比雖有所下降,但環比仍高於前值。

核心CPI環比高於預期、前值

美國勞工部公佈的重磅CPI顯示,美國2月未季調CPI同比上升6%,已連續第八個月下降,為2021年9月以來新低預期6.00%,前值6.40%。

2月未季調核心CPI同比上升5.5%,預期5.5%,前值5.6%,也已連續第六個月下降,為2021年12月來新低。核心CPI環比高於預期和前值,為0.5%,達到5個月來的最高水平,表明過去一年的加息之後通脹仍然具有彈性。

CPI數據發佈後,期貨市場押注下週美聯儲加息25個基點的概率為76%,暫不加息的概率為24%,峯值利率預期重回5%。

美銀評價CPI稱,2月的CPI報吿繼續説明了美聯儲目前面臨的是粘性通脹問題。鑑於美聯儲對不包括房租的核心服務的關注,美聯儲不會因為2月份核心服務通脹環比增長0.5%而受到鼓舞。儘管銀行業的問題增加了不確定性,但美聯儲仍然需要做更多來為經濟和勞動力市場降温,預計美聯儲下週將加息25基點,且利率將在6月達到5.25%-5.50%的峯值。

摩根士丹利的首席美國經濟學家Ellen Zentner也認為,通脹數據堅定地支持美聯儲在3月份再次加息25基點,且加息週期可能不會在5月份停止。

美國銀行業將加強監管

儘管市場已經先一步反彈,但銀行業危機並未結束。昨日,美國評級公司穆迪下調對整個美國銀行系統評級的評估至負面,之前持穩定展望。

穆迪現在認為,雖然拜登政府和美聯儲等眾多監管部門竭力承託銀行業,但“(銀行業)運營環境(仍然)在急劇惡化——硅谷銀行和簽名銀行的存款流失、且這兩家地區銀行機構先後倒閉”。

對於美股市場上銀行股的企穩,美國白宮高級官員稱,美國聯邦監管當局週日採取緊急措施後,政府正在密切監控第一共和銀行和其他銀行的動態。如果沒有這些干預措施,美國銀行系統的狀況要比現在糟糕得多。市場企穩令人欣慰,人們花了一些時間來探討週日行動帶來的影響。還需要仔細監控是否有大量資金流向大型銀行。

有消息透露,美聯儲在硅谷銀行倒閉事件發生後,正在考慮對中型銀行實施更嚴格的監管規定,可能會將當前用於監管大型銀行的規則擴大到中型銀行上。

據一位熟悉美國監管機構最新想法的人士透露,當局正在審議對銀行業實施一系列更嚴格的資本和流動性要求,以及加強年度"壓力測試"的措施。這些規定可能針對資產規模在1000億至2500億美元之間的銀行,這些銀行目前沒有受到最嚴格的監管要求。

美國參議院銀行委員會主席、民主黨人布朗也呼籲,此前美國在2018年放鬆銀行業監管規定是一大錯誤,美國需要對銀行業實施更強力的資本及流動性監管措施。布朗還希望,美聯儲能夠在下週的會議上暫停加息。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.