美聯儲加息恐止於今年,之後將是300個基點的降息?

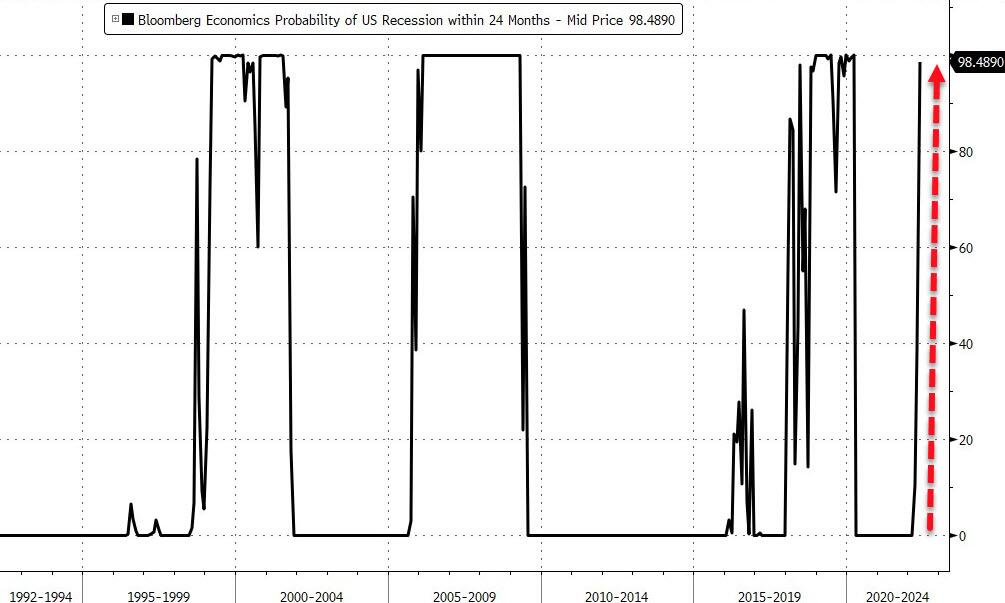

在全球範圍內,以美國爲首的西方國家對俄羅斯的制裁造成了大宗商品和食品高通脹。在輸入性通脹面前,美聯儲毫無招架之力,持續的大幅加息適得其反,市場對美國經濟衰退的擔憂逐漸升溫。

金融博客零對衝認爲,在一場毀滅性的衰退浪潮席捲整個美國之後不久,爲了“救災”,美聯儲將匆忙開啓新一輪量化寬鬆。

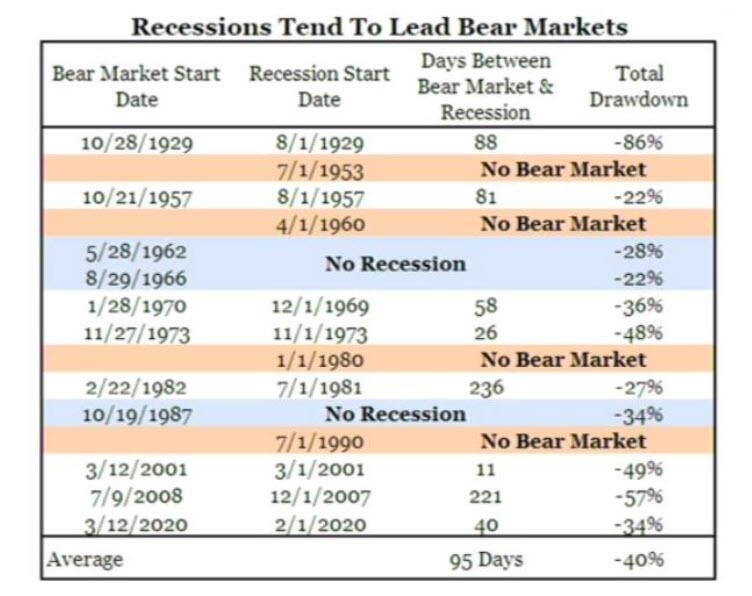

考慮到經濟衰退已開始被市場定價,那麼市場唯一的問題是,美國經濟衰退將於何時爆發?對此,德意志銀行(DB)認爲是2023年;野村證券最新(6月19日)預計,這個時間最早將是2022年下半年。

考慮到經濟衰退已開始被市場定價,那麼市場唯一的問題是,美國經濟衰退將於何時爆發?對此,德意志銀行(DB)認爲是2023年;野村證券最新(6月19日)預計,這個時間最早將是2022年下半年。

而金融博客零對衝甚至認爲,早在三個月前,美國經濟可能就已經開始衰退了。美聯儲再加息幾次,就會在今年結束加息週期。

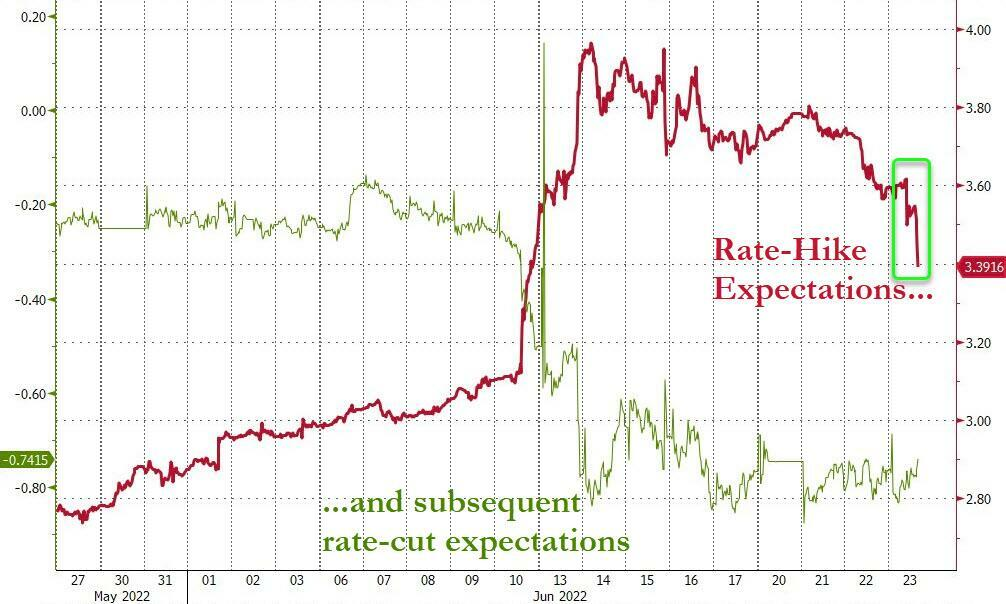

彭博分析師Edward Bolingbroke稱,隨着美國經濟衰退的可能性接近100%,隔夜利率掉期市場的加息溢價正逐漸下滑,6月23日的交易日內出現了另一次大幅的政策重新定價。

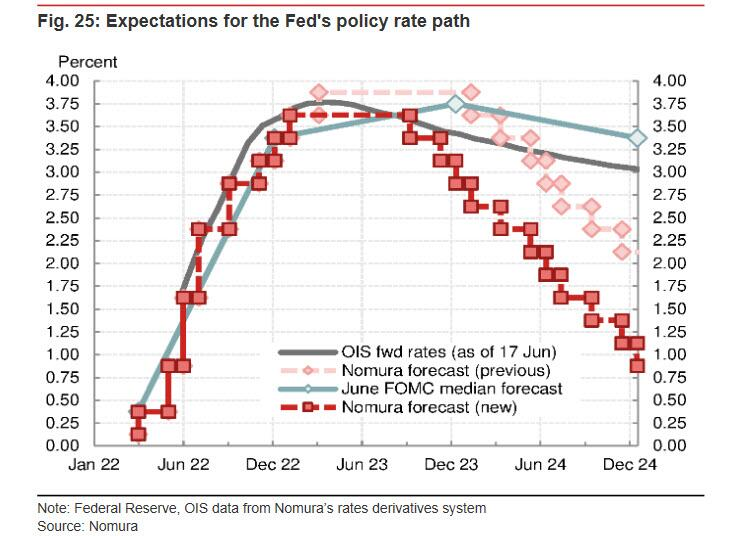

如下圖所示,交易員們不再預計美聯儲在12月FOMC會議之後會繼續加息。相反,目前的歐洲美元利差顯示,交易員預計明年會出現近50個基點的降息。

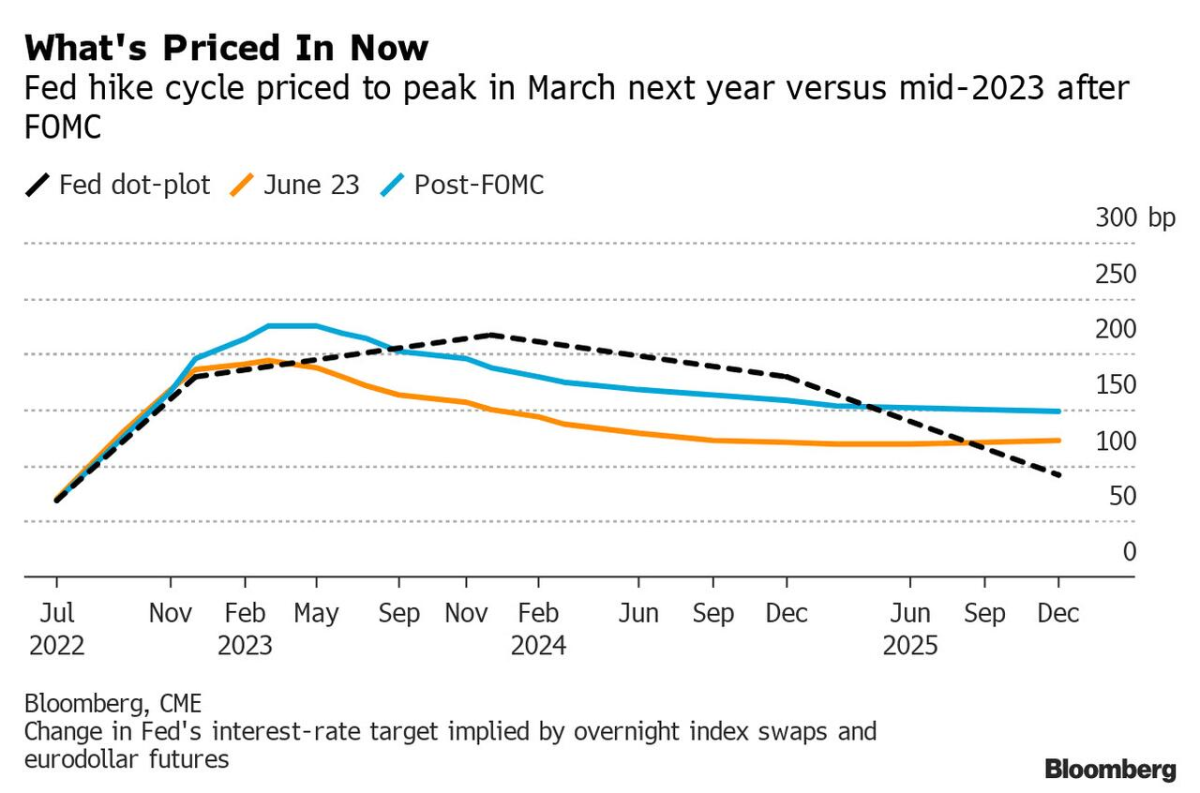

具體而言,最新數據顯示,市場預計美聯儲在12月會議前還將加息175個基點。這可以被解讀爲,在美聯儲放慢加息腳步之前,還會再以75個基點的幅度加息一次。目前,在今年7、9、11、12月的FOMC會議上,美聯儲可能的加息組合包括:

1、75個基點+50個基點+25個基點+25個基點;

2、75個基點+50個基點+50個基點,在12月FOMC會議上暫停加息。

經濟衰退的可能性越高,美聯儲在7月和9月加息75個基點的可能性就越低。事實上,正如下圖所示,7月和9月加息75個基點的可能性正在迅速下降(分別爲68%和22%),而在12月和明年2月加息25個基點的可能性也大幅下滑。

簡而言之,市場正在對美聯儲在中期選舉前結束加息週期進行定價。

結束加息之後會發生什麼呢?零對衝認爲,考慮到美國經濟將受到重創,美聯儲將在2023年初(甚至2022年底)倉促降息,隨之而來的就是量化寬鬆。儘管美聯儲還沒有把這作爲他們的基本方針,但他們正越來越近靠近這一方針。

在上週末發佈的報告中,野村證券(Nomura)將2022年年底出現衰退作爲基本預測情景,該行認爲,隨着衰退加劇,美聯儲認爲失業率上升和整體需求減弱將壓低通脹,並對此信心滿滿。野村補充稱:

在年度通脹仍在上升的背景下,美聯儲可能在幾個月的時間內,將聯邦基金利率提升至在限制性水平(3%-3.5%)。我們預計美聯儲將提前開始降息,降息將始於2023年9月,而不是2024年初。理由是,更高的失業率和更弱的經濟增長應該會增加美聯儲「通脹將持續回到2%」的信心。

因此,野村證券認爲,美聯儲將從2023年9月份開始,在每次FOMC會議上降息25個基點,這終將導致2023年底聯邦基金利率爲2.875%,2024年底爲0.875%。這相當於在18個月左右的時間裏,美聯儲將降息300個基點。

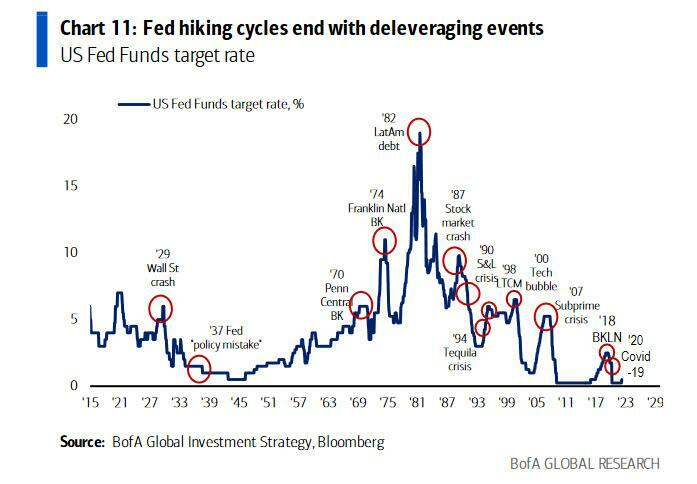

零對衝同意野村證券預測的寬鬆規模,但也認爲野村證券低估了美聯儲即將進行降息的速度。依照歷史經驗,一旦美聯儲的加息週期達到頂峯,美聯儲的政策就會開始急速轉向。

零對衝認爲,一旦美聯儲開啓新一輪量化寬鬆,那必然是突飛猛進的:美聯儲將在幾周內多次大幅降息,在極短的時間內將聯邦基金利率推回到零。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.