煤炭:疫情拖累需求,外部風險仍存

本文來自格隆匯專欄:中金研究,作者:王炙鹿 郭朝輝

海外煤價高企,進口關税取消或緩解進口成本壓力

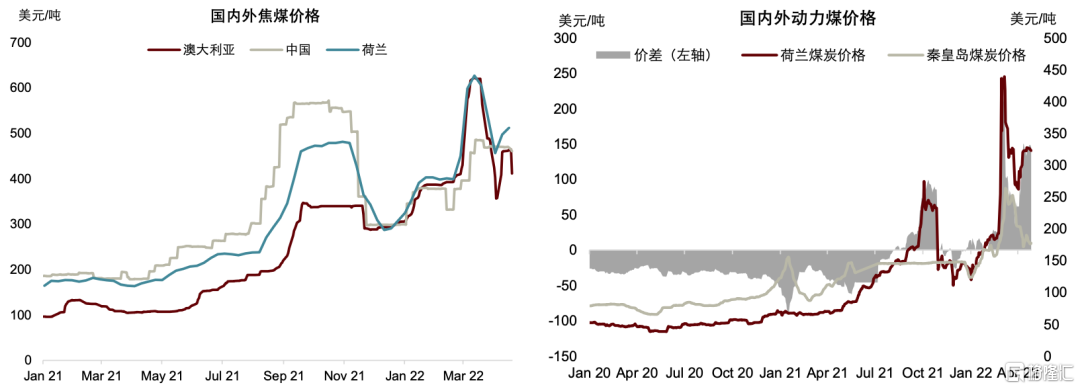

在俄烏局勢的衝擊下,海外煤炭價格出現了飆升。(詳見《海外煤、氣價大漲,折射歐洲能源三重矛盾》)隨着歐洲宣佈將對俄羅斯煤炭進口實施禁運,我們先前所擔憂的制裁升級已逐步轉為現實。當前,海外煤炭庫存偏低,供給彈性偏弱,與煤炭互為發電能源替代的天然氣價格也較為高昂,考慮到歐洲對俄羅斯煤炭的依賴度(近70%動力煤進口來自於俄羅斯),我們認為俄煤進口禁運可能對海外乃至於全球煤炭的緊張格局“雪上加霜”。

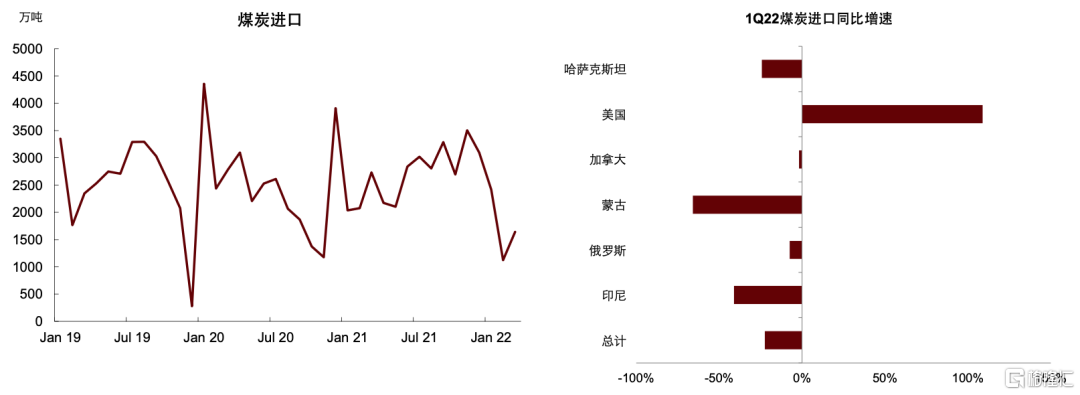

今年以來,國內外煤價長期處於倒掛之中,進口成本大漲,一季度煤炭進口下滑約24%。分國別看,蒙煤受疫情影響進口下滑程度最大,同比收縮約66%,印尼與俄羅斯也分別下滑了約41%和7.4%。

圖表: 國內外焦煤與動力煤價格

資料來源:WoodMac,Wind,Bloomberg,中金公司研究部

圖表: 中國煤炭進口與1Q22煤炭進口分國別同比增速

資料來源:海關總署,中金公司研究部

外部風險持續升温且短時難以緩解,亦加劇了國內保供穩價的壓力。近日財政部宣佈,自2022年5月1日起至2021年3月31日,對煤炭實施税率為零的進口暫定税率[1]。我們認為這在一定程度上將緩解高昂進口煤炭以及近期人民幣對美元匯率下行帶來的進口成本壓力。但當前海外煤、氣庫存均處於低位,且歐洲對俄天然氣政策尚不明朗,我們認為海外能源價格可能維持在高位波動,國內外價差可能將持續。另外,俄煤與蒙煤進口下滑可能是價差之外的因素導致,譬如俄烏局勢與疫情對運輸的擾動,往前看不確定性亦較大,焦煤進口可能仍面臨一定風險。

保供穩價持續加碼,國內產量保持在高位

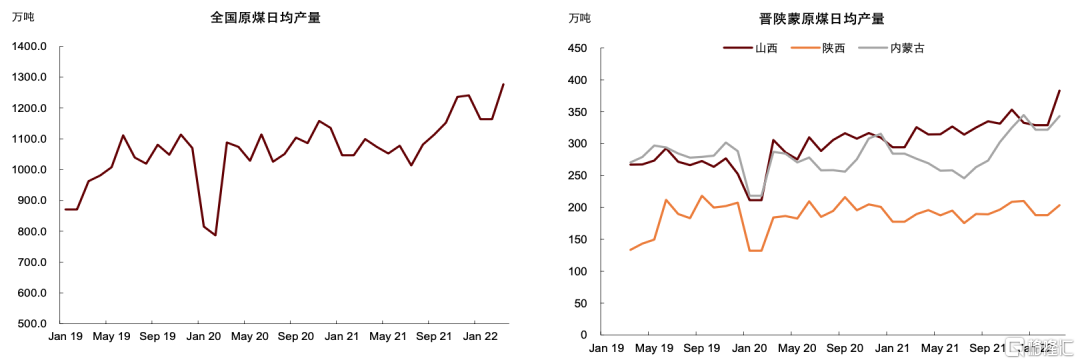

在國內,一季度原煤產量與電廠庫存均增長較快,國家亦積極引導煤炭價格運行在合理區間,並提升長協覆蓋度與執行率。我們看到原煤基本延續了去年四季度的產出強度,一季度原煤日均產量1203萬噸,同比增長12.9%,其中3月日均產量1277萬噸,高於去年12月的日均水平。山西仍是增產主力,3月日均產量達383萬噸,是歷史新高,較去年11月提升了約30萬噸/天。

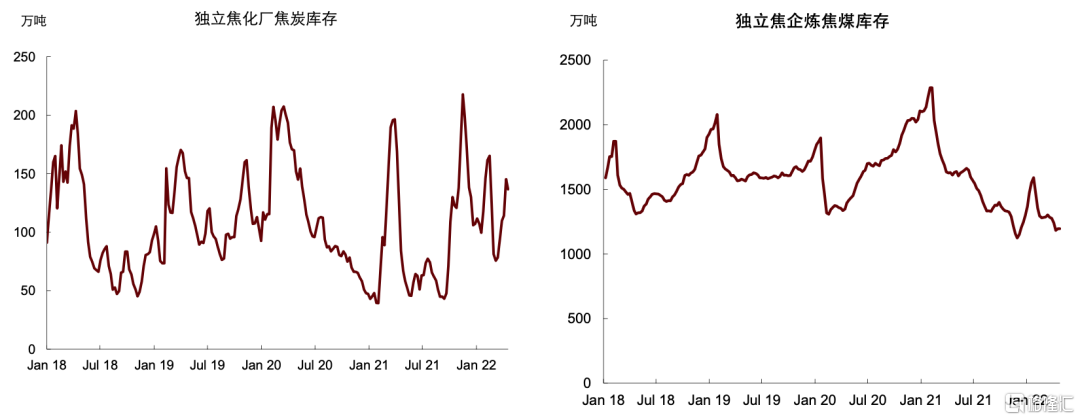

圖表: 獨立焦化廠焦炭庫存與獨立焦企煉焦煤庫存

資料來源:Mysteel,中金公司研究部

圖表: 全國與晉陝蒙煤炭日均產量

資料來源:國家統計局,中金公司研究部

往前看,保供穩價持續加碼,我們認為煤炭產量或將保持在高位。國家發改委要求年內再釋放3億噸的有效產能,全國日產量維持在1260萬噸以上[2]。我們預計內蒙古仍有一定產能潛力,可能是未來增產的主力。但安全事故、環保以及長協煤對市場煤供給量與運力的擠壓等因素仍不容忽視。

疫情拖累需求,但仍有回升預期

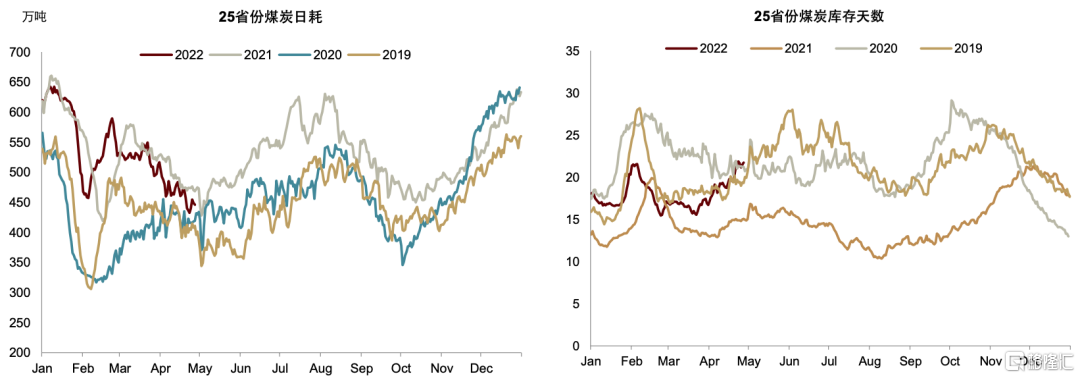

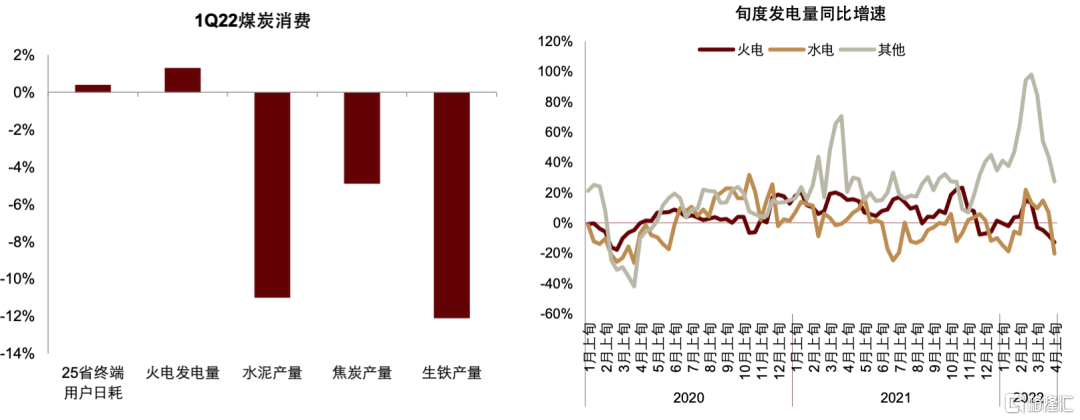

需求方面,今年一季度煤炭消費仍有小幅同比增長,我們認為主要是受到火力發電與供暖的帶動。一季度全國火力發電量同比增長約1.4%,水泥、冶金等領域下滑較為明顯,水泥與生鐵產量分別同比下滑12.1%和11.0%。一、二月份採暖與火電需求均較為旺盛,全國25省份煤炭日耗同比增長2.6%,動力煤價格表現亦較強。但自三月份至今,受局部地區疫情反覆拖累,煤炭日耗已同比轉負,沿海八省日耗甚至回落到2020年疫情初爆發時的同期水平。

時值淡季,我們認為短期需求端壓力尚可,但上海疫情逐步緩解,疊加夏季用電高峯到來,需求側仍有回升預期,屆時煤價可能仍面臨一定上行壓力,因此需密切關注淡季的補庫進度。當前25省份終端用户庫存天數已回升至近22天,較去年同比增加約7天的水平。往前看,日耗走高後,電廠可能仍有一定補庫需求。另外,值得注意的是煉焦煤庫存仍處在相對較低的水平。

圖表: 25省份煤炭日耗與庫存天數

資料來源:CCTD,中金公司研究部

圖表: 1Q22煤炭下游消費同比增速與旬度發電量同比增速

資料來源:CCTD,國家統計局,中金公司研究部

全年來看,我們認為今年火力發電需求可能仍有小幅的上漲,但水電預期較好,火電總體壓力可能小於去年。冶金、建材等領域的煤炭需求可能有小幅下滑,主要是受到地產的拖累。從基本面看,今年煤炭的供需缺口將趨於收窄,但也難言大幅放鬆。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.