Market NewsHong Kong stock market review: the Hang Seng Branch Index fell 3.48% and lost 4000 points, technology stocks suffered another heavy fall, and catering stocks collectively pulled back.

Market NewsHong Kong stock market review: the Hang Seng Branch Index fell 3.48% and lost 4000 points, technology stocks suffered another heavy fall, and catering stocks collectively pulled back.On April 21, Hong Kong stocks fell again, and technology stocks led the market, causing the Hang Seng Technology Index to fall 3.48%, losing the 4000-point mark, and nearly 8% in a row for three days. The Hang Seng Index closed down 1.25% at 20682 points, both recording three consecutive falls. The index of state-owned enterprises fell 1.92% to 6962 points.

On the market, large-scale technology stocks JD.com fell 6.5%, Meituan fell 4.9%, and Xiaomi fell more than 4%. Military stocks, mobile games, aviation stocks, automobile stocks, photovoltaic stocks, biotechnology stocks, inner housing stocks and property management stocks fell one after another. On the other hand, large financial stocks (banks, insurance, brokerages) rose rapidly in the afternoon, most bank stocks closed higher, and Hong Kong local stocks bucked the trend. Turnover in the market today was HK $120 billion.

Specifically:

Technology stocks tumbled again. JD.com fell by more than 6%, Meituan, bilibili and Xiaomi by more than 4%, and Tencent, Alibaba, Baidu and NetEase followed suit.

Catering stocks collective pullback. The bottom of the sea fell by more than 7%, Jubaoli and Helens fell by more than 6%, and Jiaojiao and Huangpu followed suit. In terms of news, Hong Kong will relax social distance restrictions in phases from today. The first phase includes the resumption of evening restaurant dining in the catering industry. The Hong Kong SAR government also called on members of the public to consciously abide by the relevant epidemic prevention regulations after the relaxation of social distance measures. In the first stage, sports venues, places of public entertainment, playgrounds and so on will be reopened. In addition, starting from the 21st, the restriction prohibiting people from gathering in private places with more than two households will be lifted, and the maximum number of people gathering in public places will be relaxed from 2 to 4.

Auto stocks fell. Great Wall Motor fell by more than 5%, Xiaopeng Motor and ideal car by more than 4%, and Weilai by more than 3%. On the news side, data from the Federation of passengers show that retail sales in the overall narrow passenger car market reached an average of 27000 vehicles per day in the second week of April this year, down 39% from the same period last year and 33% lower than the average in the second week of March this year. As the epidemic has already occurred in mid-March, it is also normal to have a small month-on-month decline this week. Retail sales averaged 25000 vehicles a day in the first two weeks of April, down 35 per cent from a year earlier, reflecting relatively low demand amid recent complex outbreaks.

Gaming stocks led the decline. Asian Vanguard Entertainment fell more than 15%, Wynn Macau fell more than 8%, and Century Entertainment International fell more than 6%. Credit Suisse published a research report, saying that the valuation of Macau's gaming industry is low and its potential recovery remains optimistic, but at the same time, it points out that there are many hidden worries in the industry, including the mainland's policy of maintaining zero clearance of the epidemic, resulting in a high degree of uncertainty in the recovery of the industry; as well as macroeconomic weakness harming terminal demand, and SMEs facing operating pressure under the city closure measures, gambling revenue growth will be affected. The bank expects daily gaming revenues to pick up to 247 million patacas in the third quarter of this year and 406 million patacas in the fourth quarter, with mid-field gambling revenues expected to return to 98 per cent of 2019 levels in 2024 and VIP lounge gambling revenues expected to remain at about 1/3 of 2019 levels. In response to the latest revenue forecast, Credit Suisse cut its EBITDA forecast for high-end gambling stocks by 19 per cent to 53 per cent and its target price by 15 to 60 per cent.

Photovoltaic solar plate continues to decline. Flaite Glass fell more than 8%, Xinyi Light Energy fell more than 6%, and Xiexin New Energy, Xinte Energy and Poly Xiexin Energy fell more than 4%. Shengang Securities said this week that the implementation of the photovoltaic glass project hearing has accelerated since March, with a blowout in the number of new projects and a short-term focus on the disturbance of corporate profit expectations caused by a large amount of new production capacity and the catalysis of expectations for upstream demand for raw materials.

The concept of clothing is rising against the trend. Seagate Global rose more than 9%, Lihua Holdings and Guangtai International Holdings rose more than 4%, Fast Retailing and Urban Beauty followed. Guoxin Securities said that the recent annual reports of textile service companies have revealed that sports brands at home and abroad have shown outstanding performance and operational efficiency, and the epidemic has had a significant negative impact on plate fundamentals and valuation since mid-March, but it does not affect the potential improvement of medium-and long-term high-quality local sports brands and the growth prospects of the industry. Some manufacturing enterprises are affected by downstream demand transmission, but the companies with the advantage of share increase are still dominant in growth, and the cost pressure can be controlled gradually from the recent data. Be optimistic about the fundamentals and the opportunity for valuation to rebound in the context of historically low valuations.

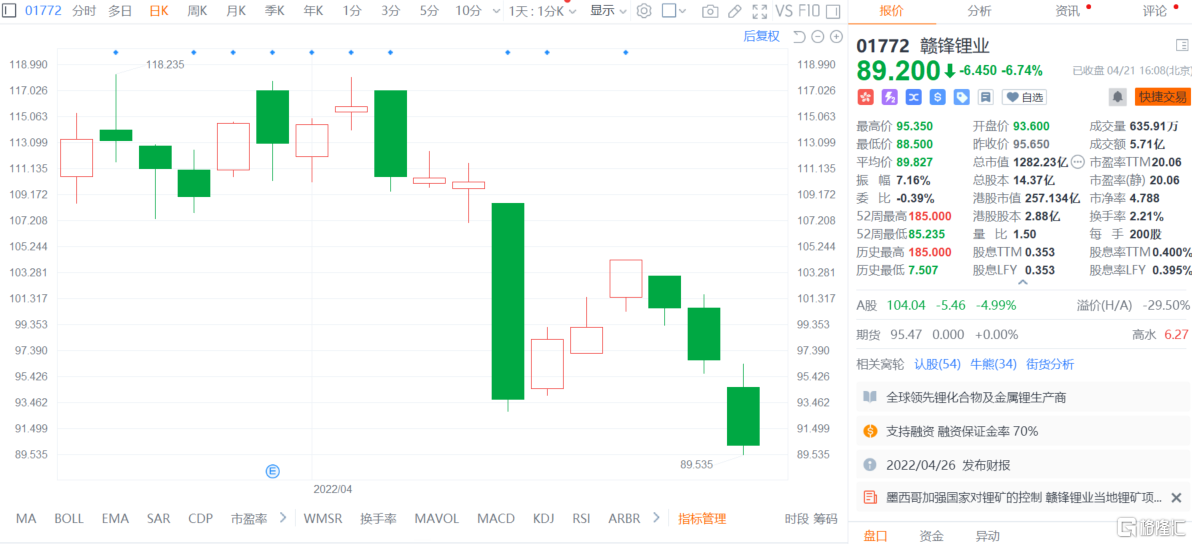

In terms of individual stocks, Ganfeng lithium fell 6.74 per cent to HK $89.2, with a total market capitalization of HK $128.2 billion. On the news, the Mexican Senate passed a mining bill on Tuesday afternoon confirming state control over lithium mining. The bill requires state-owned enterprises to take precedence over private investment in lithium mining. Mexico's president says he sees lithium as the country's strategic resource, just like oil. Previous Mexican governments have granted eight lithium exploration licenses, including Bacanora Lithium Plc, which was later acquired by China's Ganfeng Lithium Industry.

Today, the net inflow of southbound capital was-HK $530 million, of which the net inflow of Hong Kong Stock Connect (Shanghai) was-HK $511 million and that of Hong Kong Stock Connect (Shenzhen) was-HK $19 million.

Looking to the future, Citic Securities said that the Hong Kong stock market experienced a "double kill" of valuation and earnings due to multiple risk factors after the Spring Festival, but the market has currently filled the negative expectations of price in investors. Looking back, the external risks are becoming clearer, the marginal impact of Russia-Ukraine conflict and general delisting on Hong Kong stocks has gradually weakened, and the market expectations of the Fed's sustained and aggressive monetary tightening are also expected to be reversed. Internal support has become increasingly clear, the spread of the epidemic in many places across the country has had a significant impact on the economy since late March, and the policy of stabilizing growth is expected to be accelerated and intensified. Under the assumption that both internal and external risks are fully digested, it is expected that the Hong Kong stock market will usher in an annual valuation repair from the second quarter. On the main line, it is recommended to pay attention to stable growth, post-epidemic recovery plate and the Internet, mid-May may be the best configuration time.

More Content