乘聯會:“缺芯短鋰”下的中國乘用車世界超強

本文來自:乘聯會,作者:崔東樹

雖然疫情之下我們的生活也受到一定影響,我們乘用車行業自己感覺很艱難,但是我們要看到在世界性的“缺芯短鋰”形勢下,中國乘用車市場在世界的地位反而獲得了大幅的提升,總體車市的市場份額達到36%的新高,尤其中國新能源車的市場份額達到65%的世界份額。這也是在世界缺芯的情況下,中國自主品牌車企相對於其他國家車企獲取更多的芯片資源,因此自主品牌獲得更強的增長。

從數據看,芯片對中國車企的發展,不僅沒有帶來太大損失,反而在困難之中,由於中國自主車企的優秀表現而獲得了超強的市場成績。在鋰價暴漲的背景之下,中國自主品牌獲得了銷量超強增長的良好表現。相信3月的乘聯會新能源車銷量數據會給大家更大的驚喜。

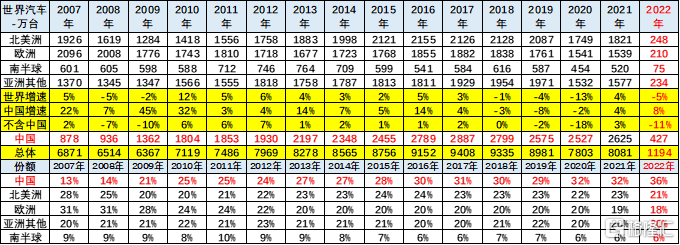

一、“缺芯”——中國汽車的世界份額創出36%新高

中國汽車市場對世界汽車市場影響力極其巨大。2018年中國汽車佔世界30%,2019年下降到29%,但仍具有絕對優勢,2020年回升到32%,2021年中國份額保持32%,2022年1-2月中國份額上升到36%。

北美和歐洲市場份額全面下降,這也是中國市場消費韌性較強的體現。

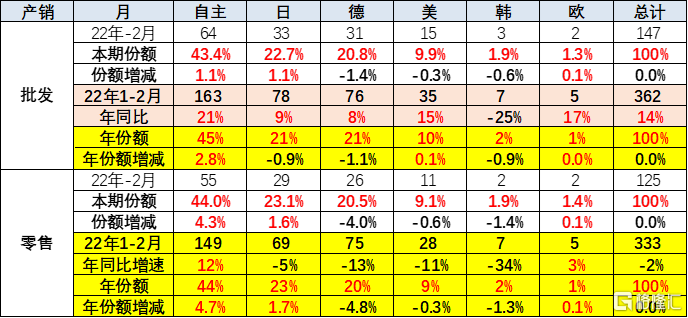

自主品牌份額近期強勢增長,目前已經達到批發45%和零售44%的超強表現。

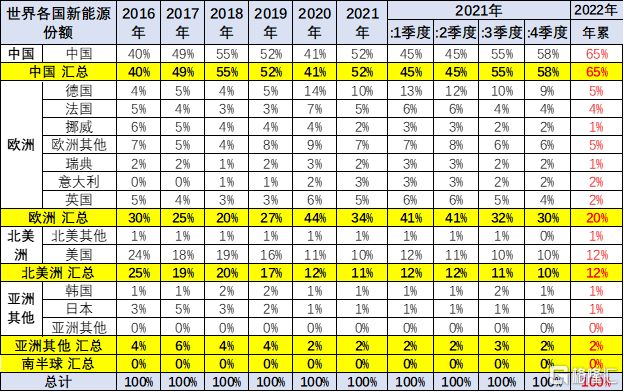

二、“短鋰”——中國新能源乘用車世界份額衝刺到65%

2021年全年的歐洲新能源市場受疫情影響,新能源增長較強。2022年仍舊受到疫情影響,2022年較2021年份額下降較大。近期中國新能源乘用車的增速弱於世界平均增長速度,2020年中國新能源乘用車世界份額較大反轉,一季度低迷,二季度反轉,下半年暴漲,2021年全年保持較強。2022年一季度的份額達到20%。

中國之外的世界其他國家的銷量走勢較強,波動較大。2020年年末的法國、德國平均增速都是翻倍之間,歐洲相對很強。增速較慢的是日本,韓國等新能源市場增長速度也是一般。

三、產業鏈優勢是中國車市走強的基礎

2020年四季度開始“缺芯”,汽車行業“缺芯”就已現端倪,一直延續到2021年下半年才開始全面爆發,全球芯片供應平均交付週期由2020年11月的13周延長至2021年11月的22.3周。

在這種缺芯的背景下,可以看到自主品牌的表現特別的突出。自主品牌的2019年生產同比下降15%,弱於行業5個點增速;2020年自主品牌同比下降9%,弱於行業增速的表現3個百分點。

工信部和市場監管總局等部委快速行動,為行業保駕護航。2021年8月,深圳一家代理商因控貨、哄抬價格,有超30人被監管部門調查。最後,這些擾亂市場、囤積居奇的經銷商,被國家市場監督管理總局“重罰”。監管部門的重拳出擊,也讓芯片供應緊張問題在短時間內得到了緩解。

自從缺芯問題嚴重後,自主品牌的表現相對優勢明顯。2021年自主品牌的生產增長29%,大幅好於行業表現的21個百分點。2022年自主品牌的生產同比增長24%,遠好於行業18%增長速度約6個百分點,所以從2020年的下半年開始,自主品牌的表現就明顯優於行業的表現,這也是缺芯背景下,自主品牌獲得高增長機會的一個明顯體現。

四、自強基因是中國車企的優勢

進入2021年,先是大眾集團宣佈因缺芯減產10萬輛車,全年銷量將跌至900萬輛以內;隨後,豐田公司也宣佈公司在日本、美國的多家車廠進入停產期,直接造成數十萬輛汽車的產能損失。大眾、豐田這樣的汽車巨頭也深受其擾,其他車企就更不必説了。

芯片短缺和大幅漲價讓很多中國車企意識到,供應環節不能過度依賴一級供應商,而是應該在國內尋找合適的芯片供應商,或者自主研發芯片,這對於自主芯片研發廠商是一次難得的機遇。

自主品牌車企自強化解芯片壓力,成效不錯。由於自強努力,因此有自主車企老總級領導奔波於芯片企業、芯片供應商、芯片批發市場等各個可能獲得芯片的環節,擔着很大的責任、受着很大的辛苦,確保了自主的芯片供給。

五、市場需求是中國車市的強大動力

中國市場獲得較強增長,主要還是中國市場的消費需求相對較為強烈,尤其是中國新能源車市場真正的市場化需求。中國新能源車市場在擺脱政策補貼的依賴之後,獲得了2020年下半年以來超強的增長,而且每月的增長基本都超越了我們的預期。

中國新能源車市場的較強購買力和對新能源車的認同,也對新能源車車型價格的上漲有一定的容忍度。因此,鋰礦價格暴漲後,導致新能源車型價格上漲,中國新能源車市場仍然保持車市的銷量在一段時間內相對較好的狀態。因此我們有信心,中國新能源車在今年仍有較好的表現。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.