本文來自格隆匯專欄:陶川,作者:東吳宏觀團隊

美聯儲剛剛結束了2022年議息會議“首秀”。會前年內加息4次、年中縮表已基本成市場共識,但1月會議美聯儲的表態明顯更“鷹”,美元和美債收益率強勢上漲,我們認為以下三點內容值得重點關注:

首先,3月將開啟加息,年內最多可能加息7次。聲明顯示美聯儲認為由於高通脹和強勁的就業,加息的合適時機很快就會到來(soon),鮑威爾在新聞發佈會上表示”如果情況合適,美聯儲希望在3月加息“,“不排除每次FOMC會議都加息的可能”,這意味着2022年加息次數最高可到7次,這一超市場預期的鷹派表述令美股由漲轉跌,美債收益率和美元指數短線大漲。

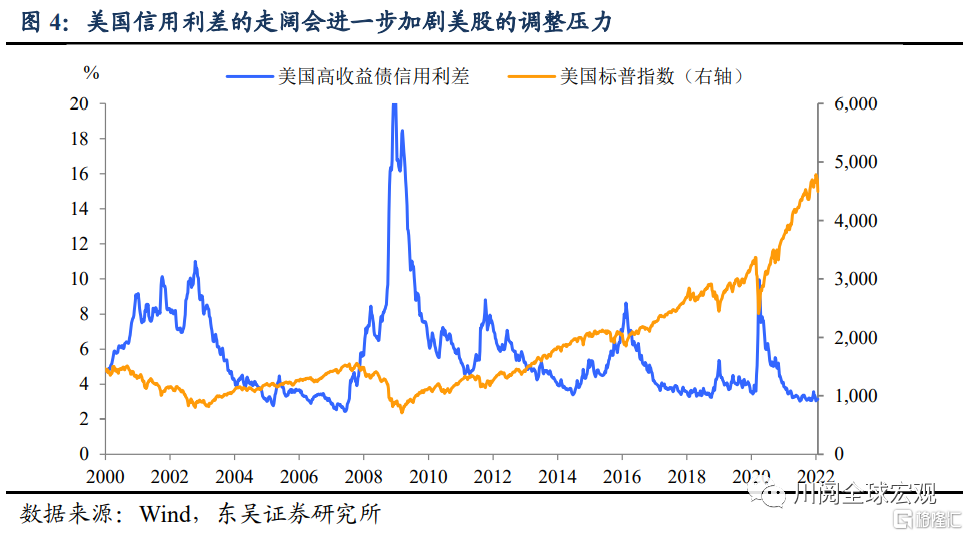

其次,縮表正式提上日程,最早7月落地。1月會議宣佈了縮表的基本原則,縮表作為加息的輔助工具,將在加息後已可預見的方式逐步落地。鮑威爾表示,”將在加息至少一次之後開會討論縮表事宜“,這意味着縮表最早將在6月正式宣佈,7月落地。除此之外,美聯儲表示長期看要減少對信用市場的影響,這意味着縮表可能優先減少MBS的持有量,信用利差走闊進一步使得美股承壓。

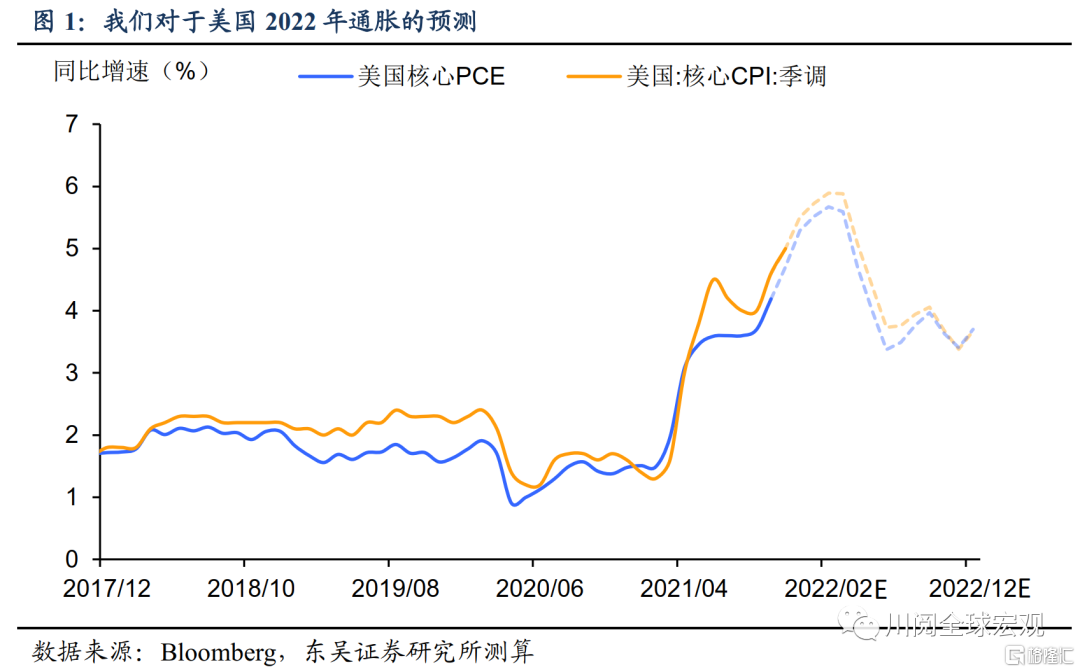

第三,通脹形勢依舊嚴峻,供給瓶頸短期內無法解決。隨着美國就業市場繼續改善、逐步接近充分就業,由供給瓶頸和工資上漲帶來的通脹壓力可能比聯儲預期的更長久。半導體等供應鏈問題將持續至超過2023年。我們預計美國通脹在第一季度見頂後,全年仍處於較高水平(圖1)。

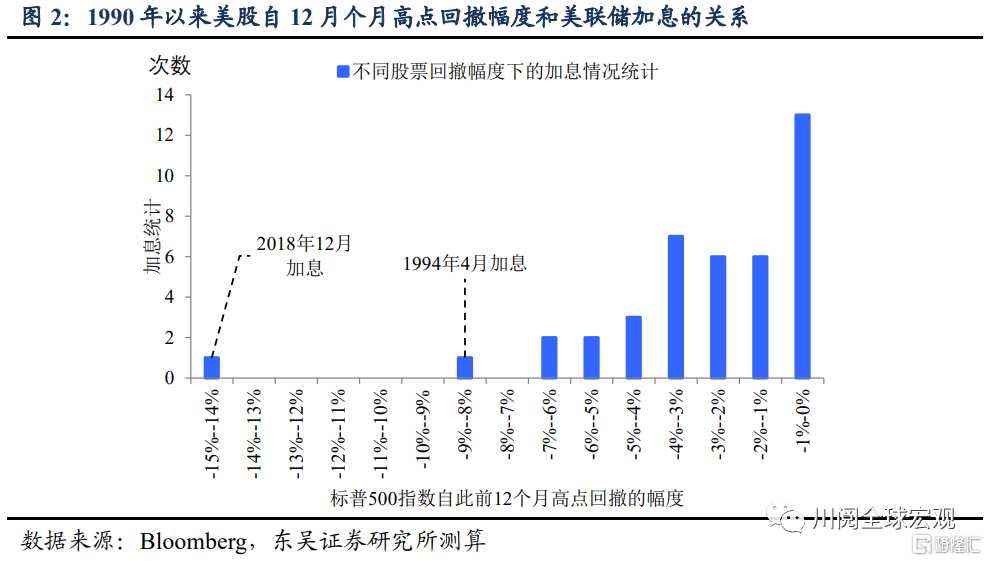

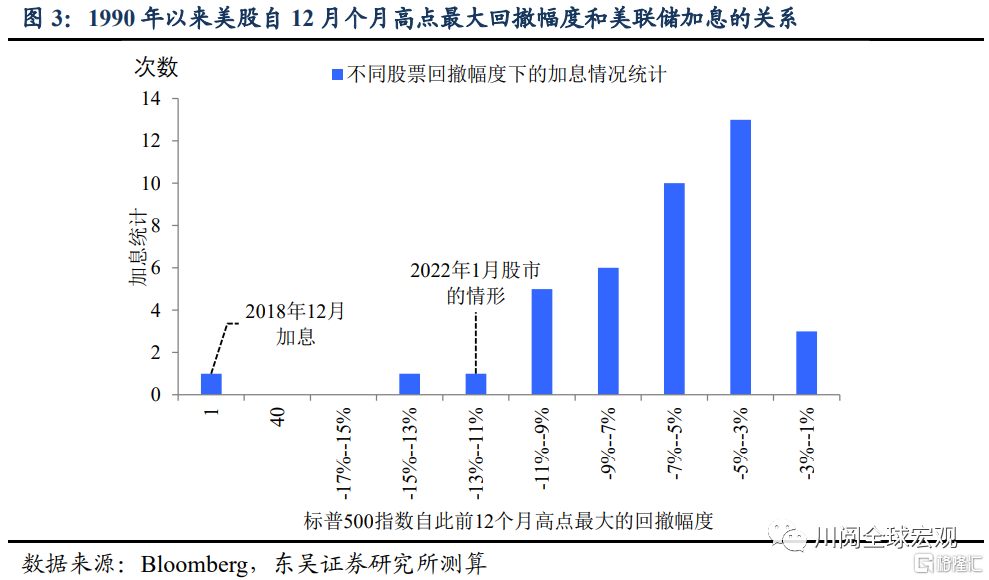

我們認為2022年美聯儲加息7次的可能性不大。除了就業和通脹之外,金融穩定也是美聯儲貨幣政策的重要考量,而股市無疑是其中重要的一環。我們認為過於快速的緊縮將導致美國股市繼續大幅回調,反過來會約束美聯儲緊縮的步伐。2022年開年以來美股的回調已經接近這一臨界點。我們統計了1990年以來標普500指數回撤幅度和聯儲加息的關係,我們發現當議息會議前標普500指數自之前12個月高點回撤幅度超過9%,最大回撤幅度超過15%時,美聯儲會暫停甚至停止加息。例如2018年12月加息就是上一輪加息週期的終點,彼時標普500自12個月高點回撤14.5%,最大回撤超過20%(圖2和3)。2022年1月議息會議前,在年內加息4次+縮表的預期下,標普的這兩個回撤指標分別達到7.9%和12.4%,已經接近制約聯儲緊縮的臨界點。

此外,縮表加速且更加偏向減持MBS可能會使得美國的信用利差走闊,這會進一步加劇美股調整的壓力。從歷史上看高收益債期限利差的大幅走闊往往對應着美股的明顯調整(圖4)。2022年初以來標普500指數雖然已經下跌約8%,雖然當前信用利差尚處於較低水平,但加息和縮表的加速很可能會使得信用利差走闊帶來美股繼續回調的壓力。

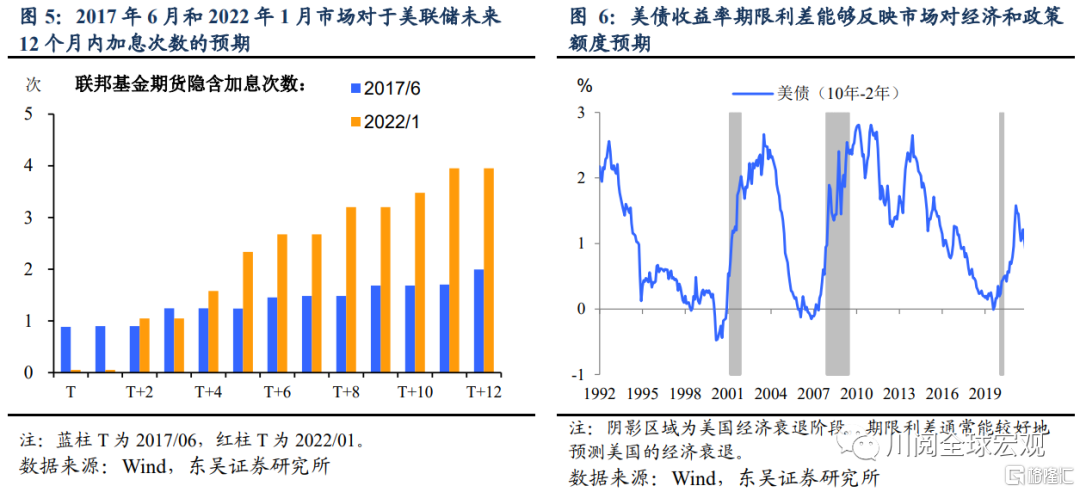

我們認為2022年美聯儲加息4次更加合理。除了上述股市方面的原因外,參考上一輪緊縮週期(2015年至2018年)來看,在類似的市場環境下,美聯儲具備年內加息4次和縮表的空間。2017年6月,市場預期未來一年內加息2次,且縮表預期強烈(美聯儲在6月議息會議公佈了縮表指引)。除此之外,當時10Y-2Y美債利差在0.78%左右,與當前相仿,而這一利差水平反映的是市場對於經濟和政策的預期情況(圖5和6)。

2017年6月之後,美聯儲於9月宣佈開始縮表,12個月內加息3次。而2018年下半年的兩次加息則被認為是導致市場動盪,經濟放緩的重要原因。考慮到美聯儲本輪緊縮週期面臨更大的通脹壓力,相對更快的年內4次加息是合理的。

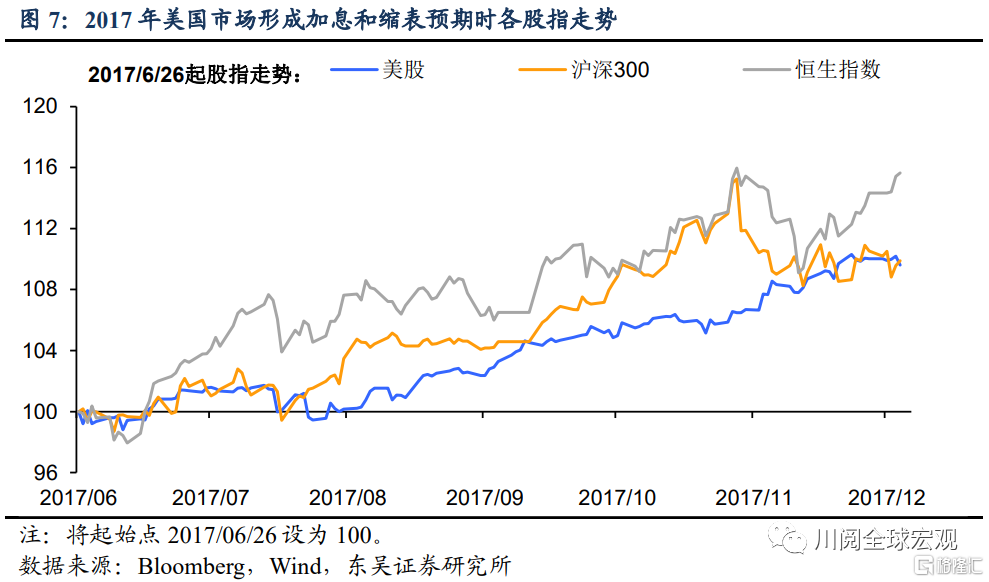

從資產表現來看,2017年6月之後市場並未因加息和縮表而崩盤。雖然當時加息預期不及2022年1月激進,但也可以作為大類資產表現的重要參考點(圖6和7):

股指方面,2017年6月後,美股、A股和港股都發生了短暫的回調,7月美股和A股橫盤震盪,但在強勁的經濟基本面的支撐下,8月各大股指重回上行態勢,最終縮表“安全落地”。總體來看,加息和縮表預期並未阻斷各大股指後半年的上漲趨勢,值得注意的是同期港股的表現更好、彈性更大。

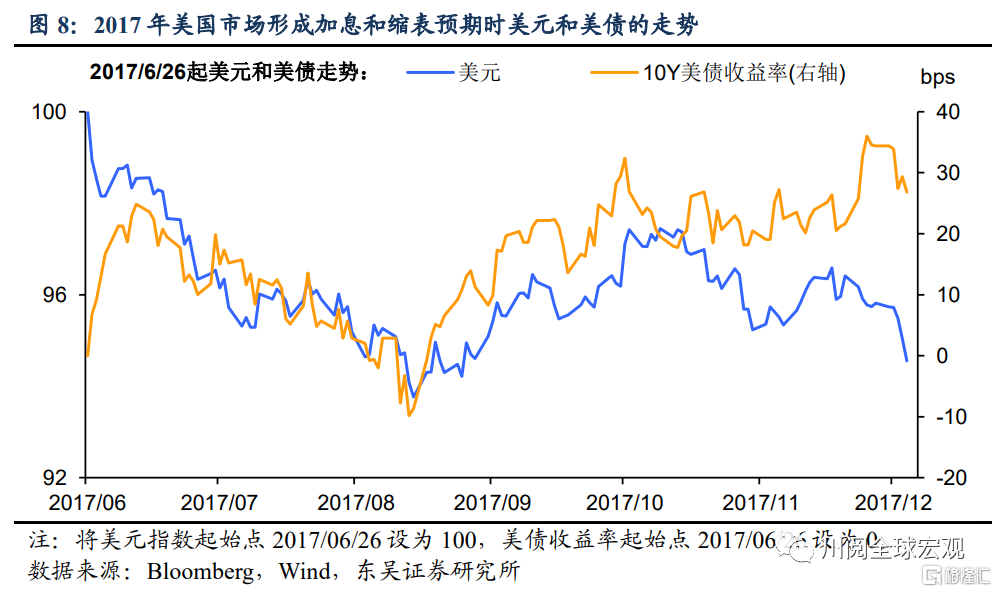

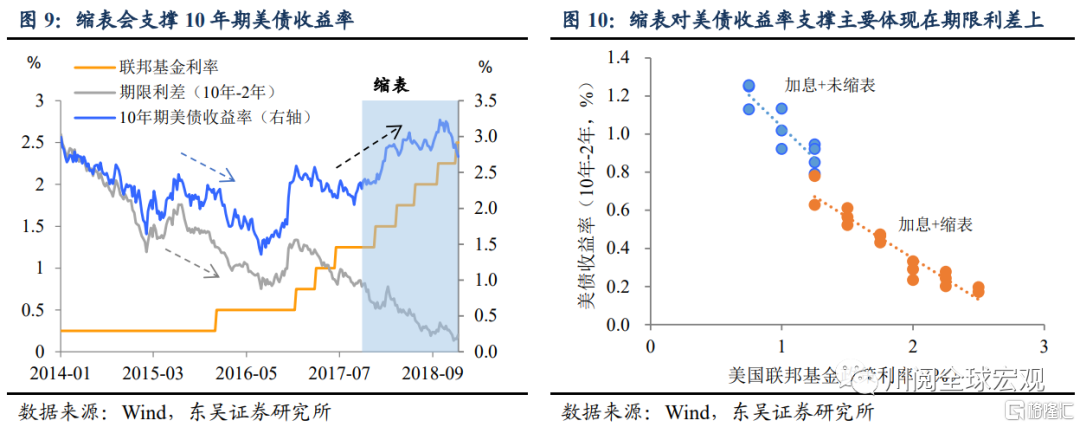

債券方面,美債出現了“三段式”行情演繹,2017年6月縮表預期漸濃時10年期美收益率上漲,隨後的回落主要反映了該預期的階段性降温,9月縮表落地後美債收益率重回上漲,這主要是由於縮表能明顯削弱加息對期限利差的壓縮效果。而這一典型的“三段式”行情演繹對於2022年的市場有一定的借鑑意義(圖8至9)。

匯率方面,2017年美元指數整體偏弱,主要的原因是全球經濟強勁復甦,以歐元區為代表的非美經濟體紛紛開始邊際收緊貨幣政策。這一重要基本面因素在2022年能否出現還存在較大不確定性,不過縮錶帶來美債收益率(尤其是實際收益率)上漲,階段性支撐美元指數走強,可能會在2022年年中再現。

風險提示:疫情變異和擴散超預期;供需緊張和地緣政治危機下商品價格超預期大漲

More Content