本文來自格隆匯專欄:國盛策略,作者: 熊園 劉新宇

事件:北京時間12月10日21:30,美國公佈11月CPI數據。

核心結論:

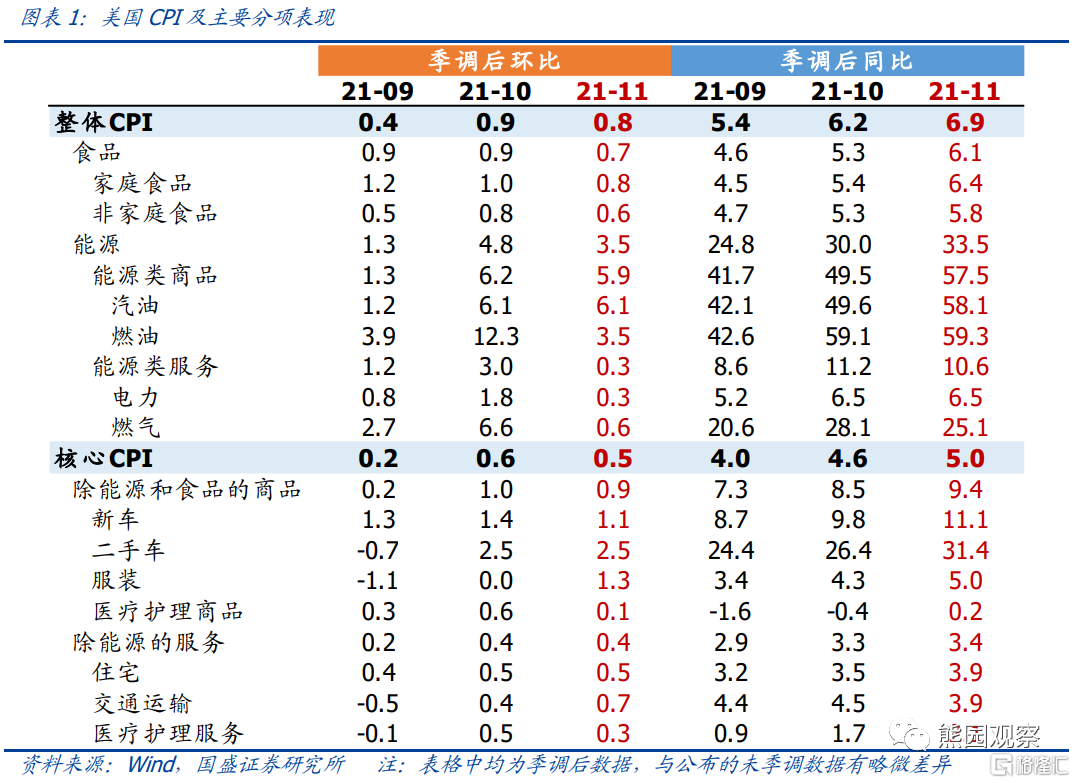

1、美國11月未季調CPI同比6.8%,符合預期,高於前值6.2%;核心CPI同比4.9%,符合預期,高於前值4.6%。分項來看,能源和二手車依然是漲幅最大的兩個分項,食品價格同比漲幅也有所擴大,服務分項價格上漲不明顯。

2、美國CPI數據公佈後,美元指數和美債收益率均快速下行,美聯儲加息預期小幅降溫。背後的邏輯在於,當前市場的通脹恐慌情緒已發酵得非常充分,在此背景下,“符合預期”即“不及預期”。

3、要判斷通脹的影響,需釐清實際通脹、通脹預期、加息預期之間的關係。概況而言,通脹預期和加息預期均跟隨實際通脹變化,但二者均是隻反映了即期通脹,沒有包含對長期通脹走勢的判斷。這也意味着,一旦通脹數據開始回落,通脹預期和加息預期均會降溫。

4、美國通脹展望:美國CPI同比大概率在12月或1月出現拐點,隨後持續回落,到2022年底有望降至2-3%。美聯儲貨幣政策方面:12/16的FOMC會議上可能宣佈加速Taper,從而將於2022年3月結束購債。我們的中性預期仍是2022年加息1次,若通脹回落較爲緩慢同時就業狀況超預期改善,不排除可能加息2次,目前市場對加息超過2次的定價有些過高。

5、大類資產展望:維持我們海外年度報告的觀點:2022年美元指數大概率上漲,高點可能破100;美債名義利率更有可能溫和下行,但實際利率可能上行;美國通脹出現拐點後,黃金大概率重回下跌通道;美股以震盪調整爲主,難持續大幅上漲。

正文如下:

1、美國11月CPI同比繼續上行,能源價格仍是最大的驅動因素

>整體表現:美國11月未季調CPI同比6.8%,符合預期,高於前值6.2%,創1983年來最高;核心CPI同比4.9%,符合預期,高於前值4.6%,創1992年來最高。

>分項來看:能源和二手車依然是漲幅最大的兩個分項,分別同比上漲33.5%、31.4%,較前值分別提高3.5、5.0個百分點;食品分項同比上漲6.1%,較前值提高0.8個百分點;服務分項同比上漲3.4%,較前值提高0.1個百分點。

2、爲何通脹創新高,美元指數與美債收益率卻在下行?

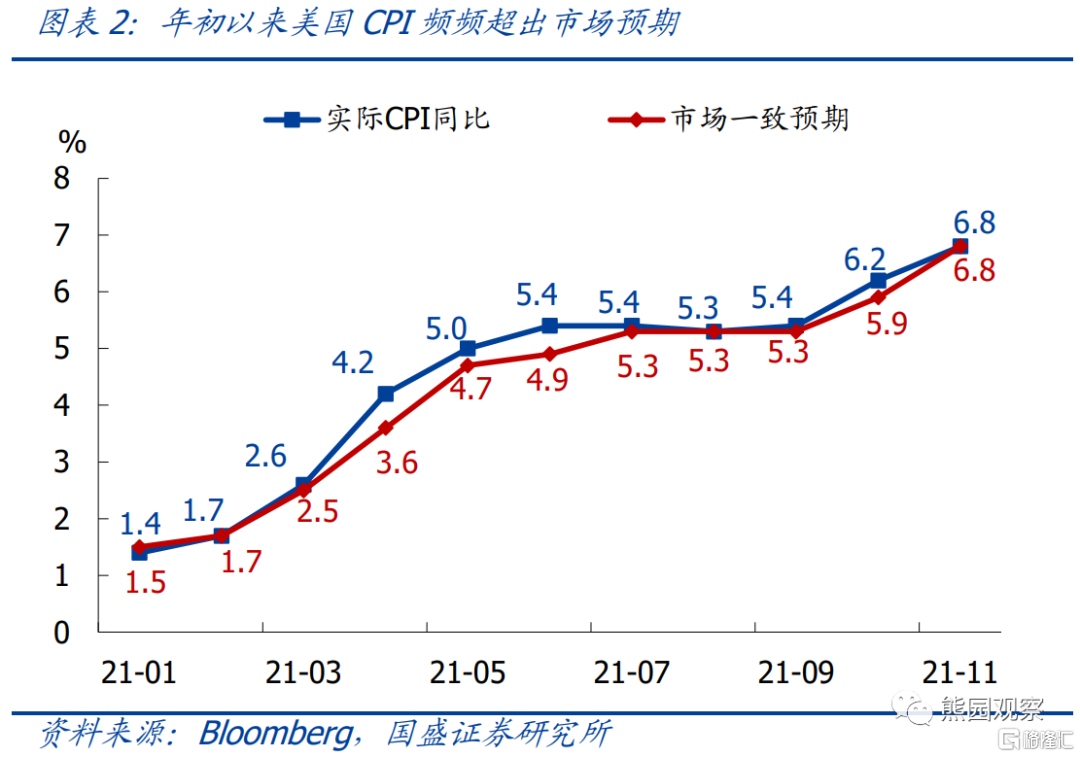

自2021年初以來,幾乎每個月的美國CPI同比都高於市場預期,且不斷創下過去數十年新高,導致通脹恐慌情緒不斷加劇。在此背景下,“符合預期”即“不及預期”,也就是說,即使通脹仍在上行,但只要沒有超預期,市場就會認爲通脹壓力即將緩解。典型代表是今年7-9月,實際CPI數據與市場一致預期差別不大,通脹擔憂暫時緩解,10Y美債收益率由1.5%降至1.2%。但自10月初以來,由於OPEC+不擴大增產和歐洲天然氣危機,能源價格持續大幅上漲,導致通脹擔憂再度加劇。

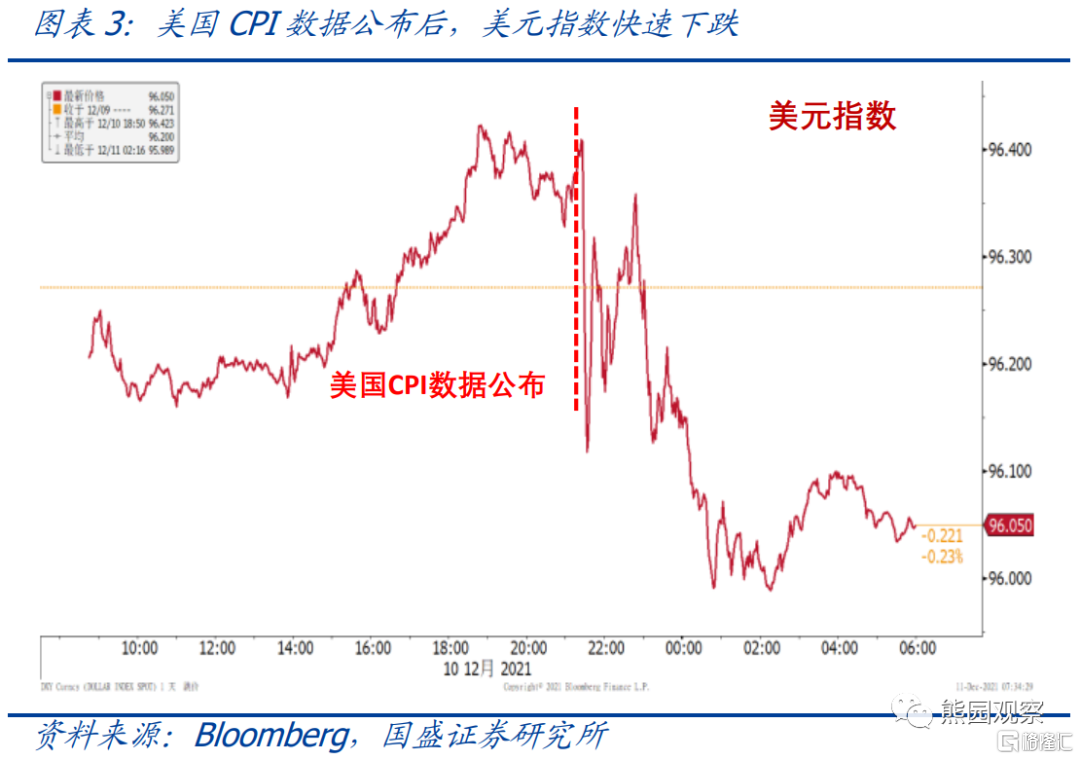

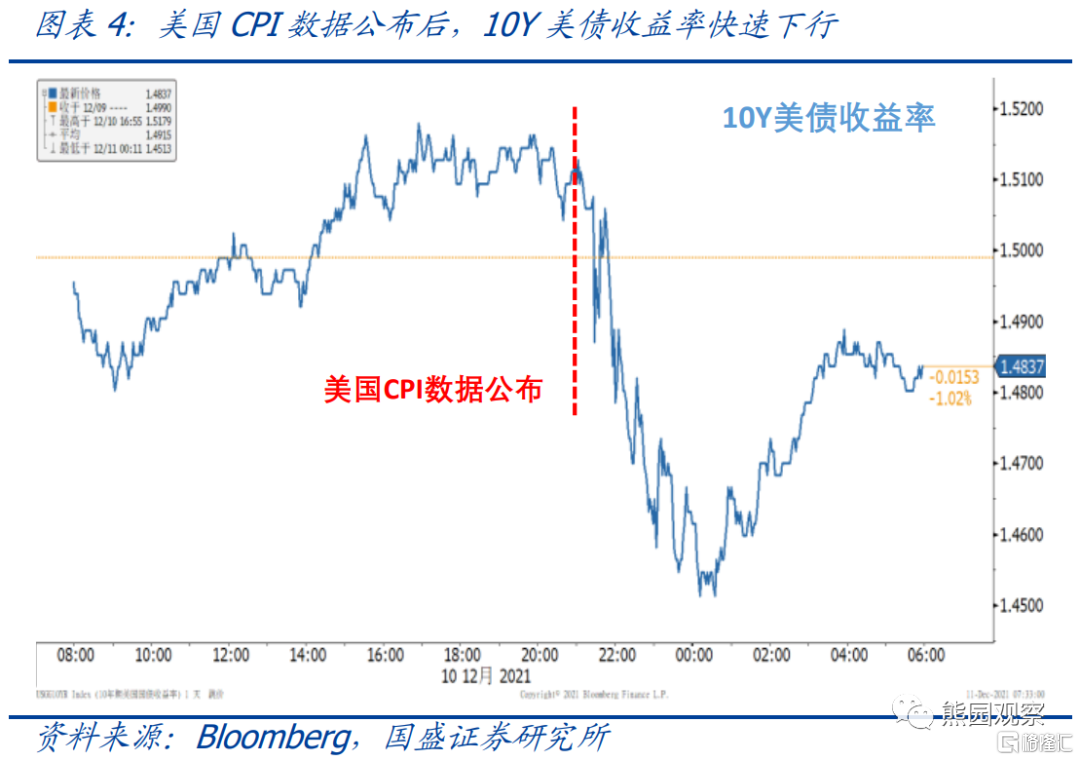

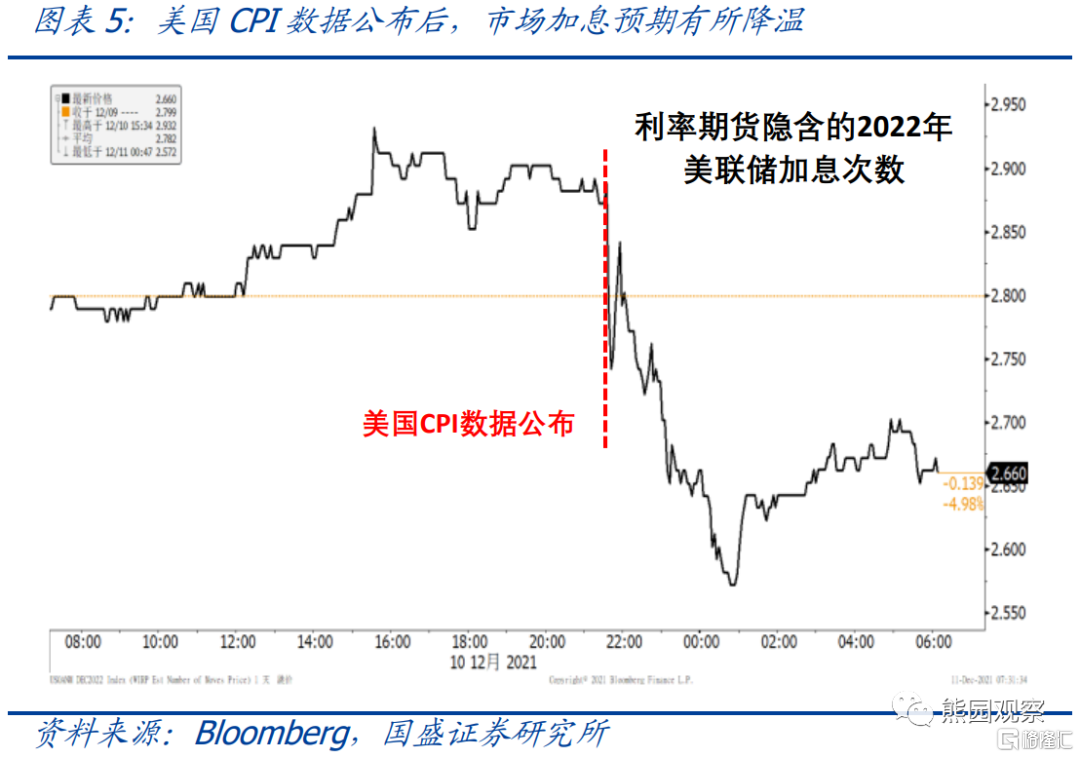

本次美國CPI數據公佈後,美元指數由96.4快速下跌至96.0左右;10Y美債收益率由1.52%一度下行至最低1.45%,最終收盤在1.49%;聯邦基金利率期貨隱含的2022年加息次數由2.9次回落至2.66次。資產價格和加息預期的這一表現,正是反映了“符合預期”即“不及預期”這一邏輯。

3、要判斷通脹的影響,需釐清實際通脹、通脹預期、加息預期之間的關係

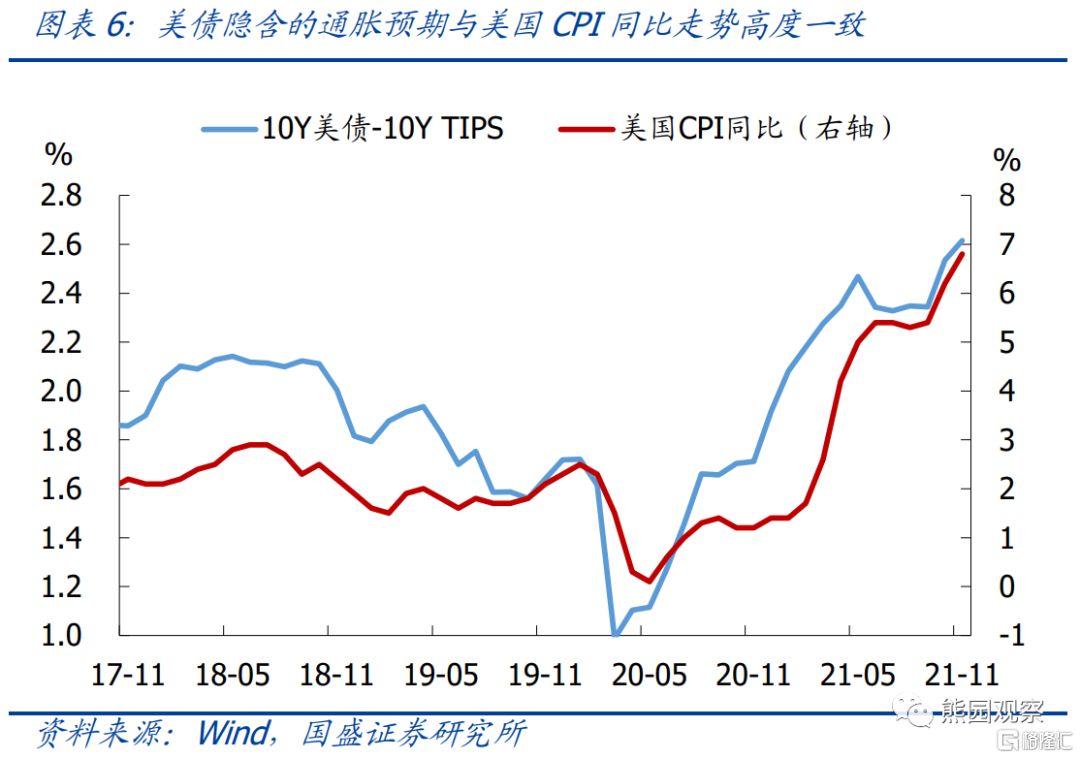

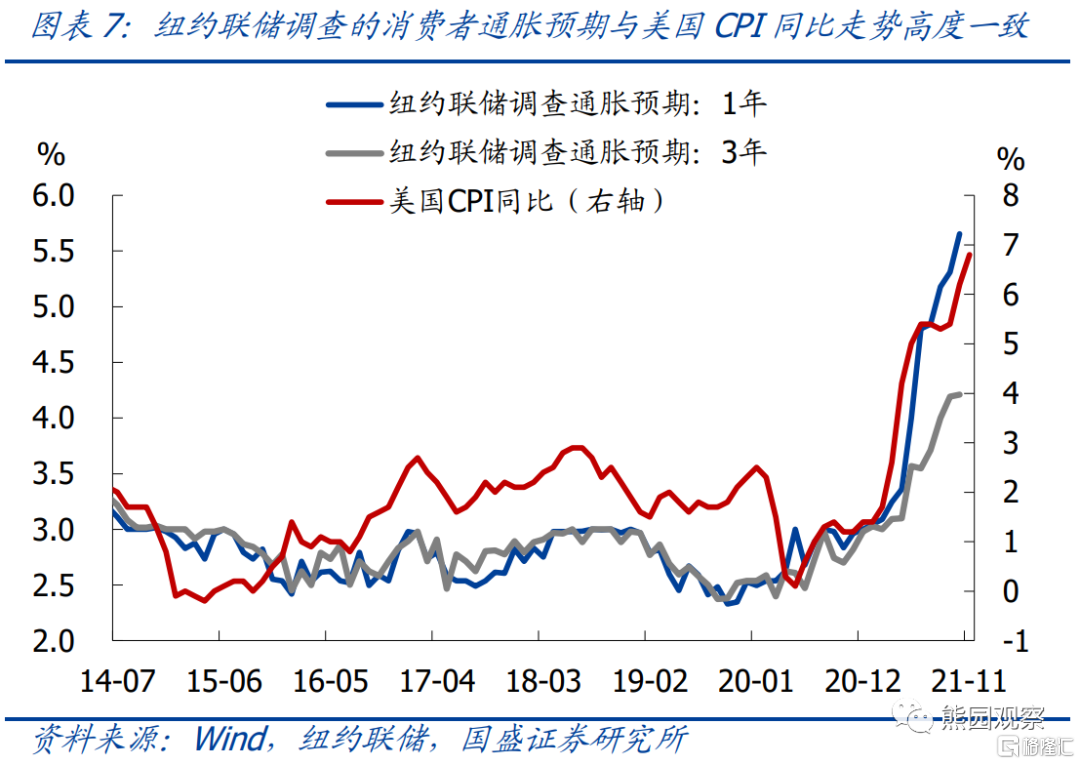

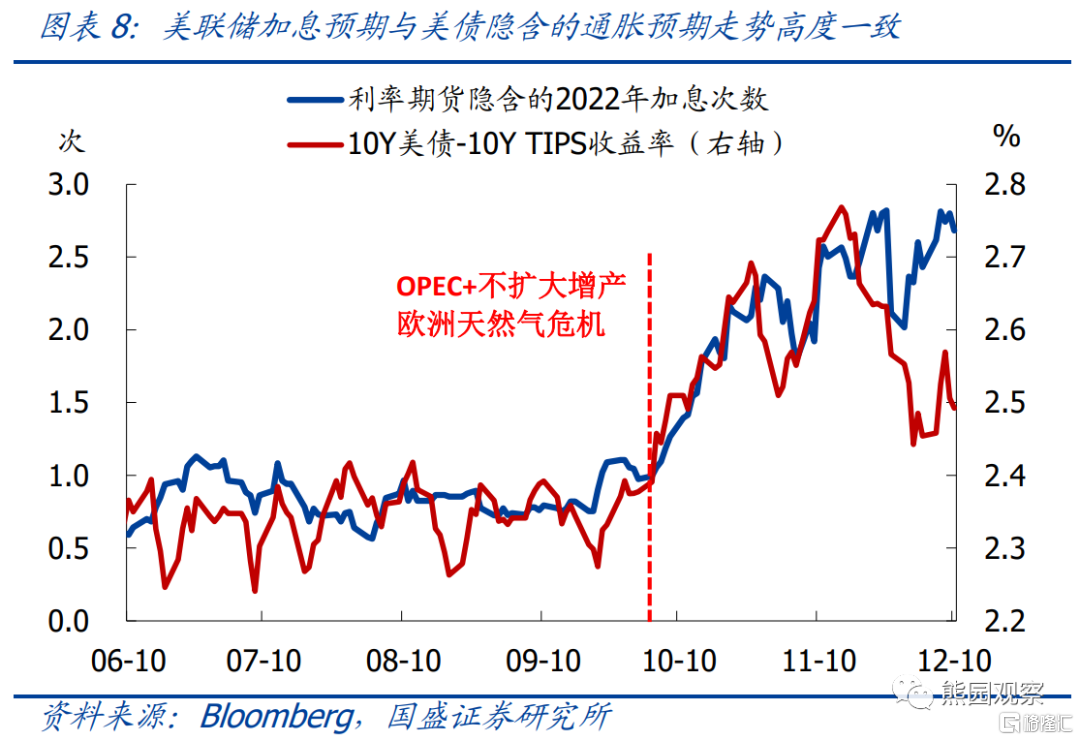

概況而言,通脹預期和加息預期均跟隨實際通脹變化,但二者均是隻反映了即期通脹,沒有包含對長期通脹走勢的判斷。不論美債隱含的市場通脹預期(美債與TIPS利差),還是紐約聯儲調查的消費者通脹預期,均與美國CPI同比走勢高度一致。同時,利率期貨隱含的加息預期與美債隱含的通脹預期走勢高度一致。

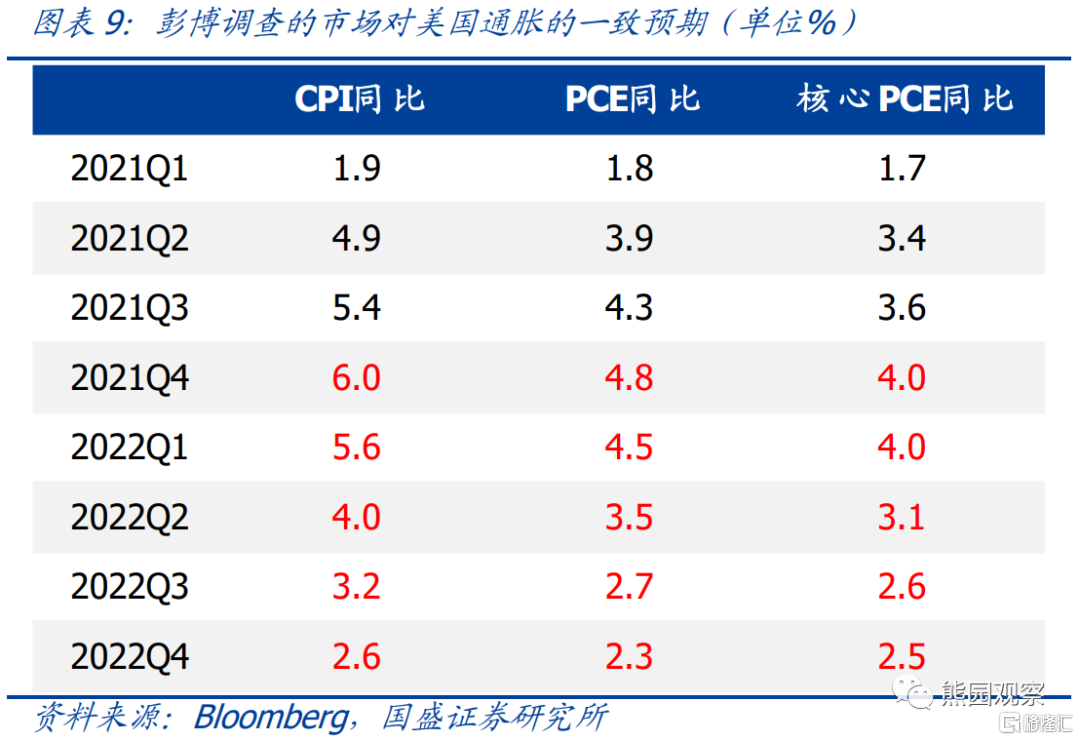

實際上,彭博最新的一致預期顯示,市場預計2022Q4美國CPI同比將降至2.6%,PCE通脹將降至2.3%,核心PCE通脹將降至2.5%,這與我們年度海外報告中的測算較爲接近。若認爲通脹會持續回落至僅略高於美聯儲的政策目標,則不應預期2022年會加息接近3次。這反映出,利率期貨隱含的加息預期更多反映了即期通脹表現,一旦通脹開始回落,加息預期也將開始降溫。

4、美國通脹可能在12月或1月出現拐點,隨後美聯儲加息預期將有所降溫

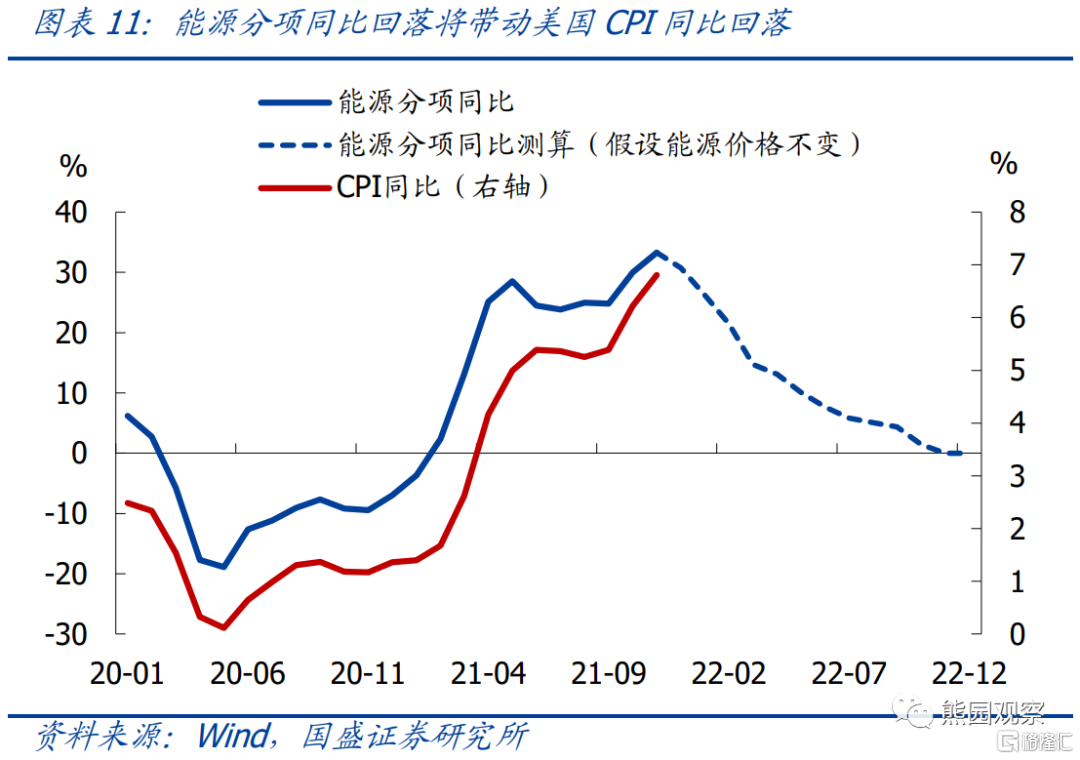

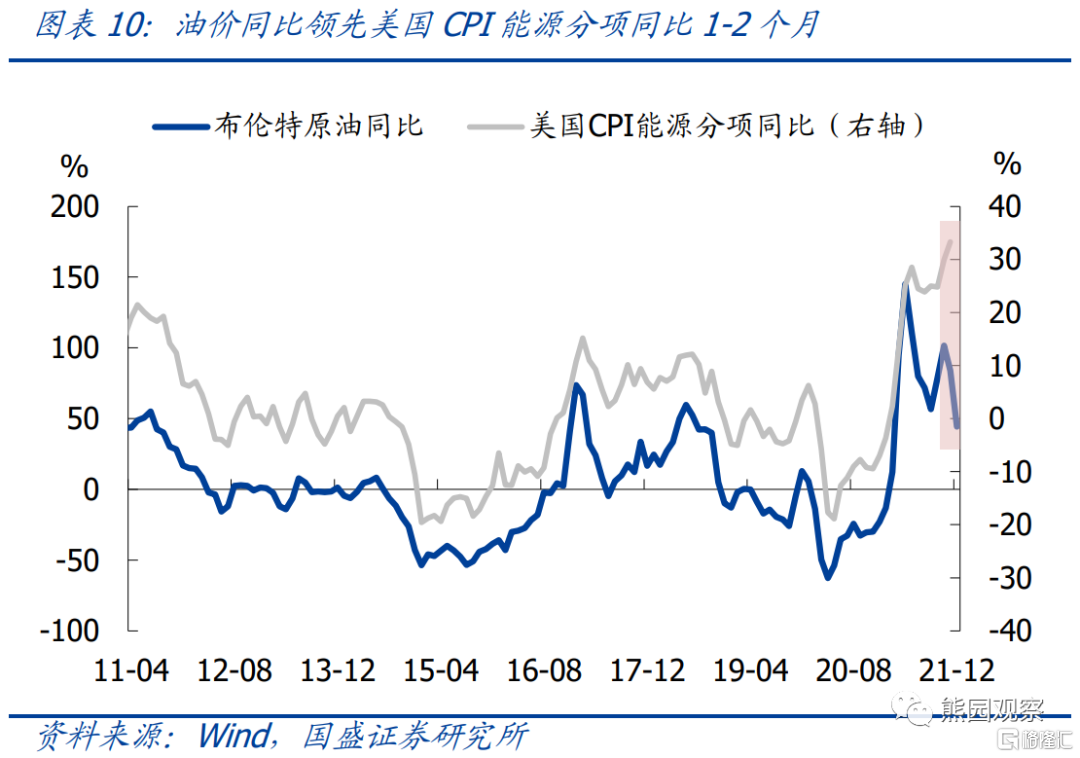

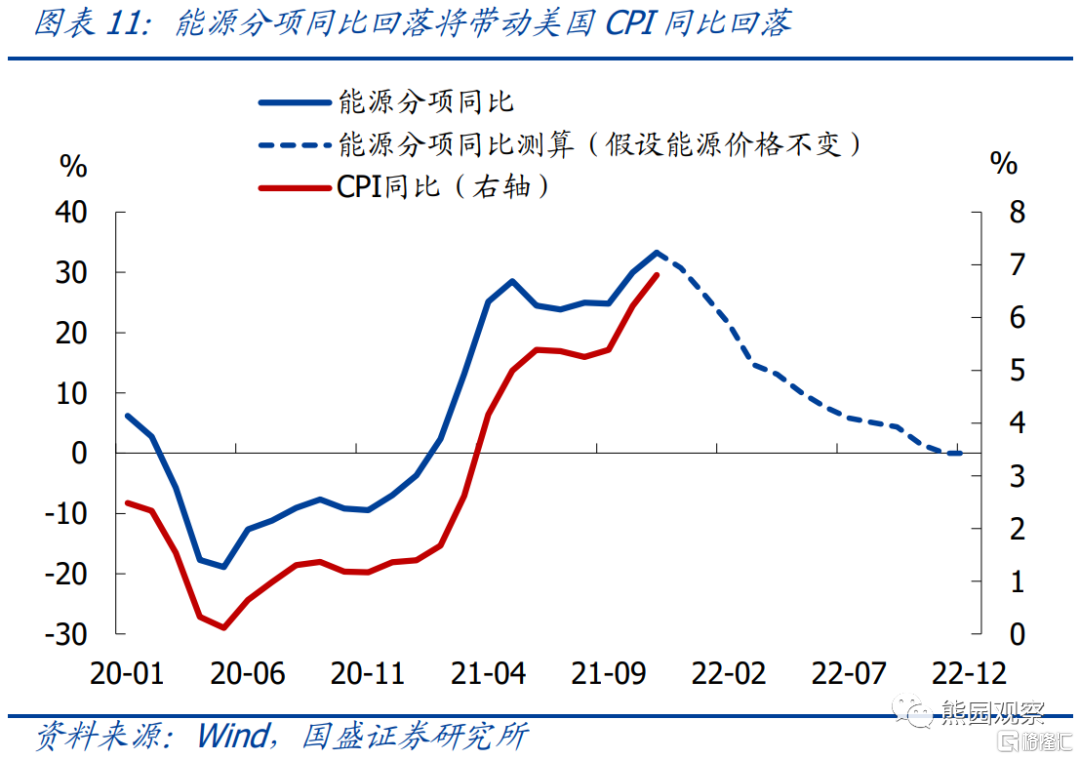

>美國通脹走勢:在前期報告中我們曾多次指出,美國通脹是“能源分項決定方向,其他分項決定幅度”,此外,原油價格同比領先CPI能源分項同比1-2月。根據我們在海外年度報告《反轉之年——2022年海外宏觀展望》中的分析,2022年原油價格大概率下跌,實際上自11月初以來油價已經下跌了超過13%,以12月至今的價格計算,油價同比已由10月的101.7%回落至44.3%。因此,美國通脹可能在12月或明年1月出現拐點,隨後持續回落,到2022年底預計將降至2-3%。

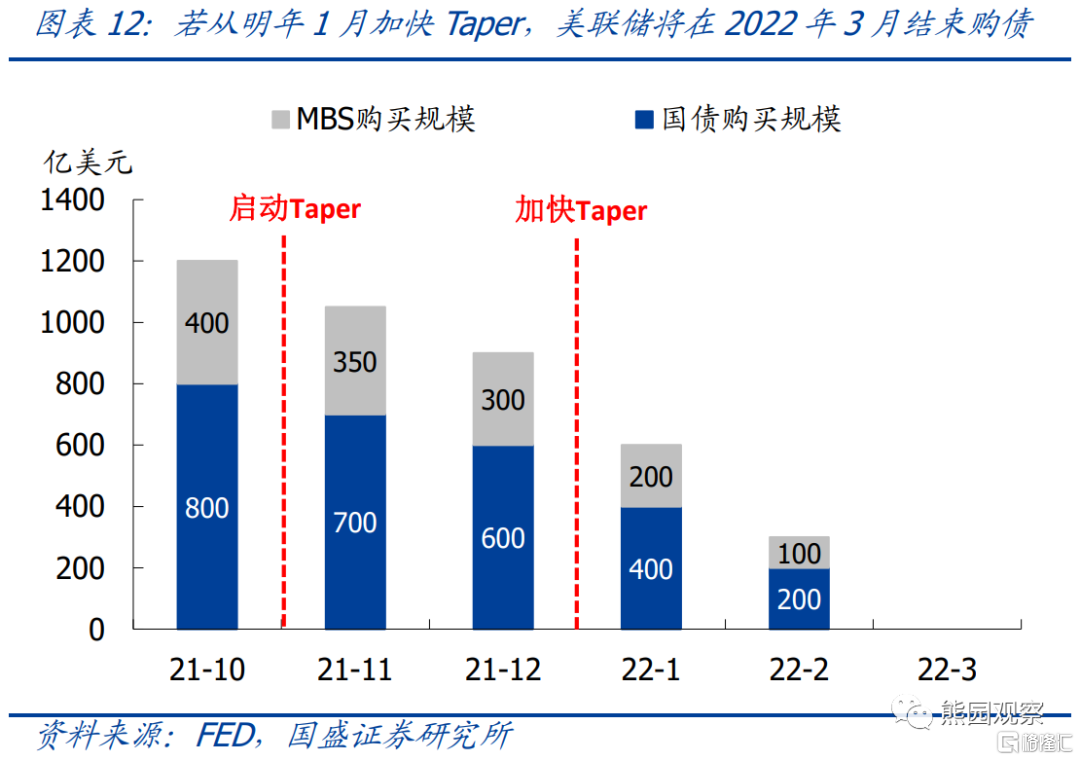

>美聯儲貨幣政策:從近期鮑威爾和其他美聯儲官員表態來看,美聯儲很有可能會在12/16的FOMC會議上宣佈加快Taper,從明年1月開始將縮債規模從150億提高到300億,從而將於2022年3月結束購債。但我們認爲這並不意味着加息節奏會進一步加快,隨着美國通脹見頂回落、經濟持續放緩,疊加Omicron病毒的衝擊,我們的中性預期仍是2022年加息1次,若通脹回落較爲緩慢同時就業狀況超預期改善,不排除可能加息2次,相比之下,目前市場對加息超過2次的定價有些過高。等到美國通脹出現拐點後,市場加息預期大概率會有所降溫。

>資產價格展望:維持我們海外年度報告的觀點:2022年美元指數大概率上漲,高點可能破100;美債名義利率更有可能溫和下行,但實際利率可能上行;美國通脹出現拐點後,黃金大概率重回下跌通道;美股以震盪調整爲主,難持續大幅上漲。

風險提示:

美國通脹持續超預期,美聯儲政策立場超預期變化。

More Content