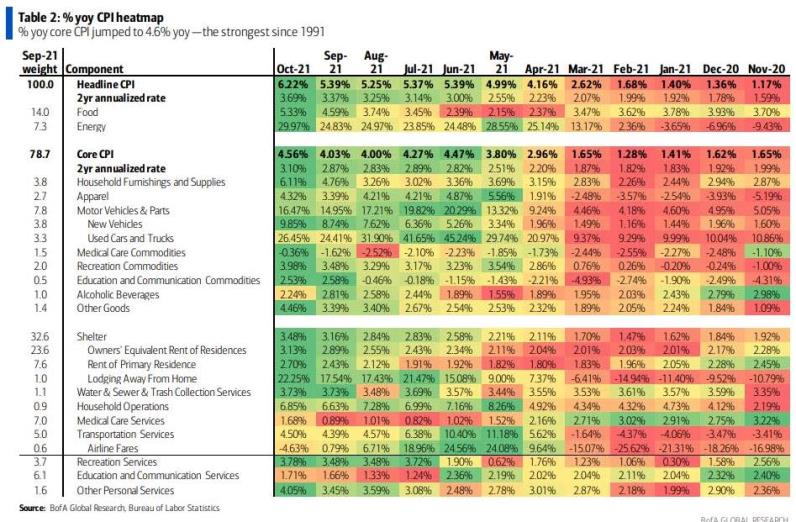

本週三,美國10月CPI數據連升17個月,同比增長6.2%,超預期,增幅創1990年12月以來新高。與此同時,市場對STIRs(短期利率期貨)定價也在急速變化,鮑威爾11月新聞發佈會的「鴿派努力」付諸東流……

實際收益率也被推至歷史新低,美股下跌,對衝通脹的資產趁勢上漲,黃金漲至5個月高點。

加息提前,還是通脹見頂?

從市場反應看,加息提前預期陡然上升。短期2年期國庫券利率上升6個基點,至0.5%。短期國庫券是交易員對美聯儲未來加息的粗略預測。

在美國通脹數據公佈之前,華爾街已經傳出,比現任美聯儲主席更加鴿派的美聯儲理事佈雷納德將繼任美聯儲主席一職,對美聯儲收緊的擔憂可見一斑。

美銀經濟學家預計,非常有「粘性」的通脹細分項——醫療服務的上升趨勢將持續到明年8月。二手車環比上漲2.5%,新車環比上漲1.4%,住宿月環比上升1.4%。

美銀分析師Alexander Lim表示,住房租金和服務業的全面通脹,可能會讓還在等待勞動力供應迴歸以及供應改善的美聯儲不安,最大的風險在於,加息可能提前,市場需要密切注意美聯儲的溝通措辭。

在評論市場反應時,美銀寫道,考慮到持久性成分的力量,熊市曲線的平緩與預期一致。前端和中期名義利率增加了5-7個基點,而長期利率變化不大。通脹盈虧平衡推高了名義利率,而實際利率暴跌,因爲債市正在爲滯脹和衰退定價。

歐洲美元曲線顯示,市場預計到23年中期將額外加息13個基點。然而,在曲線之外,利率變化不大:5年期通脹盈虧平衡下降3個基點,5年期OIS持平。市場的反應說明加息預期和近期通脹的上升一致,而長期通脹預期幾乎沒有變化。

Loyola Marymount大學和SS Economics的經濟學家Sung Won Sohn在本週三寫道,勞動力短缺仍然困擾着全球供應鏈,沒有顯示出緩解的跡象。他寫道,「通貨膨脹像野火一樣蔓延,隨着企業爭搶提供更高工資、獎金和其他福利的工人,通脹預期上升。」

不過,並不是所有人都認爲通脹還會持續走高。

PNC Financial Services 的首席經濟學家Gus Faucher 就表示,波羅的海乾散貨運價指數的下跌可能表明,經濟中已經出現的一些過熱正在逆轉,最糟糕的情況或許已經過去,至少對國際貿易商品而言是這樣。

波羅的海乾散貨運價指數跟蹤運輸原材料的船舶運價,每日更新。該指數在2021年1月份開始加速,從去年12月份的1350上升到2000。不到兩個月後,美國CPI攀升至2.6%,高於美聯儲2%的長期通脹目標,並達到2018年以來的最高水平。

波羅的海乾散貨運價指數下降自6月以來的最低水平,這讓華爾街部分人士認爲,2021年最後兩個月的通脹可能會有所緩解。

然而,波羅的海乾散貨運價指數指數下降,也不能完全說明問題。

當前,美國收入同比增長約4.9%,但CPI漲幅超過6%。這意味着,平均而言,實際工資在過去12個月實際上有所下降。許多美國人根本買不到一年前那麼多物資。隨着美國完成假日購物,對國際貨物的需求可能會減少,並緩解西海岸港口的交通。相反,人們可以決定把收入花在經濟的服務方面,選擇旅遊、參觀水療和度假村、觀看現場音樂和體育賽事。通脹的前景更加難以預測。

2022年,美聯儲新添鷹派票委

鮑威爾在上週的一次新聞發佈會上說,央行經濟學家預計高通脹將「持續到明年」。他補充說,他希望到2022年第二或第三季度,物價上漲將有所緩解。

鮑威爾11月初表示:「我們看到的通脹其實不是由於勞動力市場緊張,而是供應瓶頸和短缺。很難預測供應鏈約束的持續性或其對通脹的影響。全球供應鏈是複雜的,它們將恢復正常功能,但恢復的時間非常不確定。」

美聯儲2022年票委之一、聖路易斯聯儲主席James Bullard本週表示,「基於我們現在的狀況,我實際上認爲美聯儲將在2022年計劃加息兩次」。

James Bullard不是美聯儲政策制定委員會2021年的投票委員,但明年會如期成爲票委。相對來講,他對通脹更加擔憂,比美聯儲其他多數官員更爲鷹派。

More Content