本文來自格隆匯專欄:新時代策略,作者:邢曙光 劉娟秀

一般認爲PMI枯榮線是50%,PMI大於50%,經濟擴張,反之經濟收縮。然而,無論是從理論還是事實來看,PMI真正的枯榮線都不是50%,而是略高於50%。

類似於實際經濟增速和潛在經濟增速的概念,由於技術進步、人口增長等因素,經濟長期是增長的,PMI的長期趨勢也是擴張的,應該大於50%,只有PMI大於這個閾值,實際經濟增速才大於潛在經濟增速,產出缺口才會增加,經濟纔是擴張的,反之,產出缺口縮小,經濟收縮。

由於PMI數據的特殊性,很難從理論上得到對應潛在經濟增速的PMI數值。非要給個數的話,可以這樣粗略計算。雖然PMI理論上是季調環比數據,但是它和GDP同比等指標更相關,我們將PMI視爲同比數據。假設一國的潛在經濟增速是2%,那麼對應潛在經濟增速的PMI應是51%(51%/50%-1=2%)。這是沒有依據的很不準確的測算。我們只好依據歷史數據來測算PMI真正的枯榮線。

雖然美國製造業增加值佔GDP的比重已經比較低,但是各部經濟聯繫密切,製造業PMI和非製造業PMI大致同趨勢,製造業PMI能夠反映整體經濟形勢,加上製造業PMI數據時間較長,我們用製造業PMI替代綜合PMI。

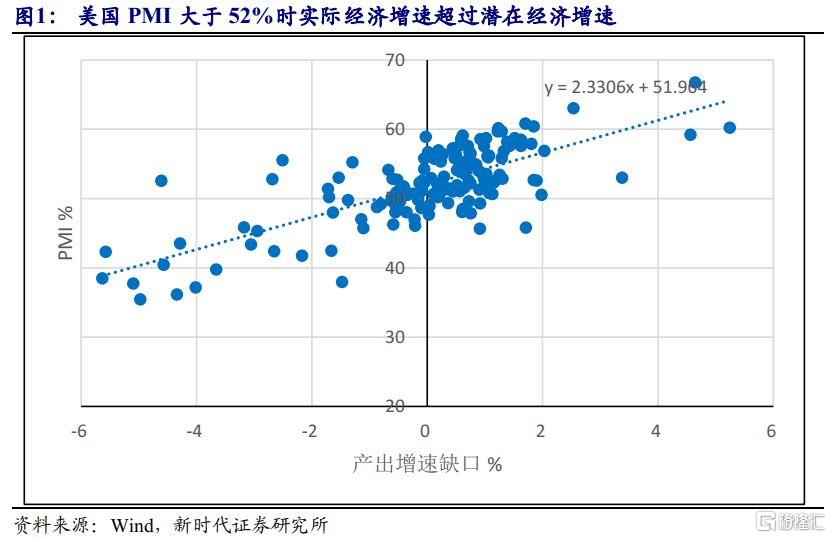

從經驗上看,美國潛在經濟增速對應的PMI爲52%。當PMI大於52%,實際經濟增速超過潛在經濟增速,經濟增速缺口爲正,反之,實際經濟增速低於潛在經濟增速,經濟增速缺口爲負。當然,這是經驗上的均值,每一次的具體值可能不同。

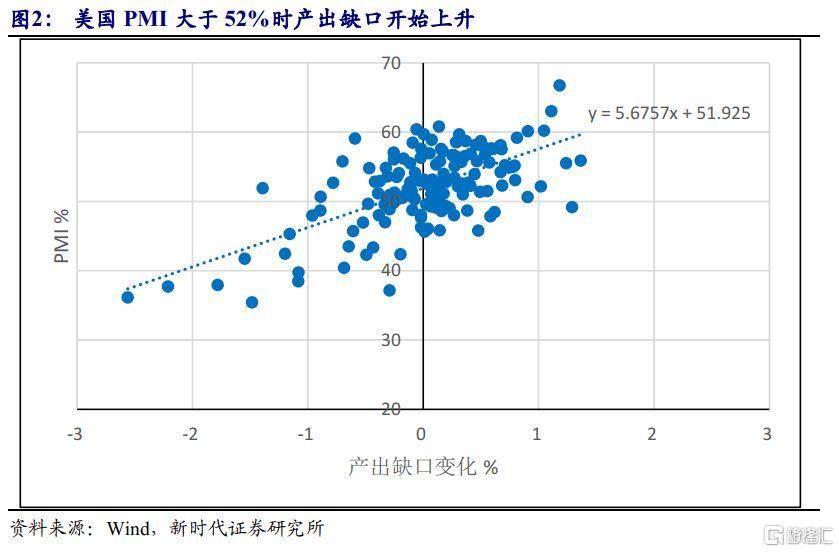

經濟增速超過潛在經濟增速時,產出缺口上升,反之,產出缺口下降,所以,也可以從產出缺口的變化來看PM枯榮線。

經濟增速超過潛在經濟增速時,產出缺口上升,反之,產出缺口下降,所以,也可以從產出缺口的變化來看PM枯榮線。

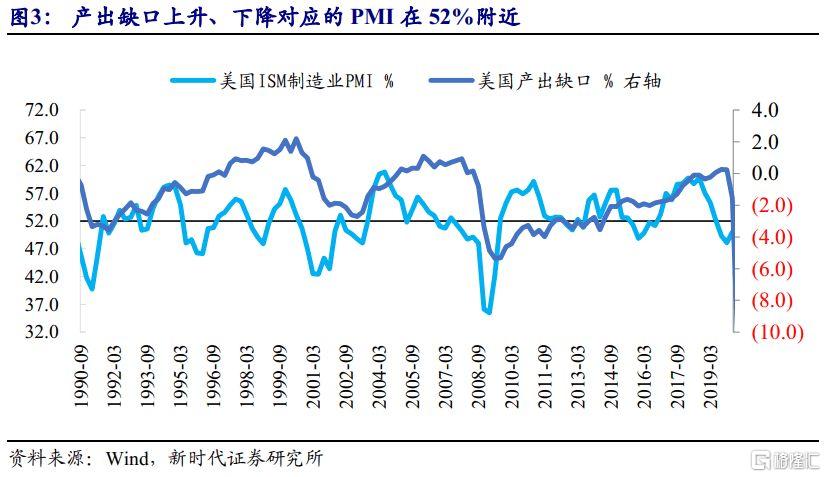

以1990年以來的美國幾輪經濟週期爲例。1992年一季度美國開始新一輪經濟週期,實際經濟增速超過潛在經濟增速,產出缺口開始回升,此時PMI季度均值是52.5%,2000年三季度經濟進入衰退階段,實際經濟增速低於潛在經濟增速,產出缺口開始下降,此時PMI均值爲50.7%。2003年三季度產出缺口再次開始回升,PMI均值是52.5%,2008年一季度產出缺口再次下降時,PMI也從50%開始下滑。2009年三季度產出缺口又開始回升,PMI均值爲50.7%,2020年一季度產出缺口又明顯下降,PMI均值爲50%。2020年三季度產出缺口回升時,PMI均值爲55%,當前PMI雖然有所下降,但仍高於真正的枯榮線,產出缺口會繼續上升。

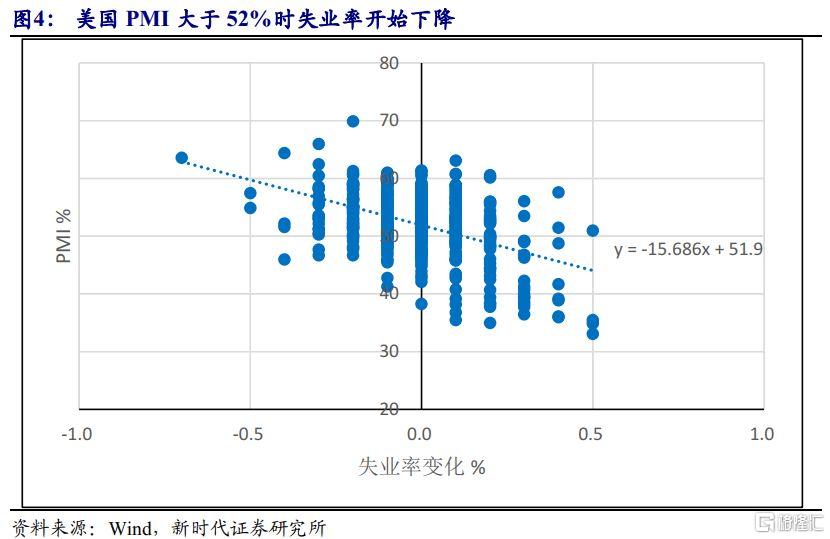

從失業率同樣可以得到PMI真正的枯榮線爲52%。當PMI大於真正的枯榮線時,失業率開始下降。只要PMI仍高於真正的枯榮線,即使PMI下滑,失業率也會繼續下降。相反,如果PMI低於真正的枯榮線,即使PMI上升,失業率也不會下降。

由於季度GDP數據、月度失業率數據都是離散的,不是連續的,依據這些數據得到的PMI枯榮線也是粗略估計,特別在是某個時間點,PMI枯榮線會變化比較大。

由於季度GDP數據、月度失業率數據都是離散的,不是連續的,依據這些數據得到的PMI枯榮線也是粗略估計,特別在是某個時間點,PMI枯榮線會變化比較大。

還有一個簡單的方法。如果PMI圍繞長期趨勢波動,那長期來看PMI的均值就是真正的枯榮線。但現實並非如此。由於經濟週期是非對稱的,實際經濟增速並不是對稱地繞着潛在經濟增速波動,PMI均值也不是真正的枯榮線。不過,從統計數據來看,PMI均值雖然和真正的枯榮線存在差異,但差距並不大,可以作爲真正枯榮線的近似值。

樣本區間不同,測算的真正枯榮線存在差異,但大部分處於51%至53%之間,將52%作爲美國製造業PMI真正的枯榮線是合理的。服務業的PMI大於製造業,綜合PMI的真正枯榮線大於製造業PMI、小於服務業PMI。

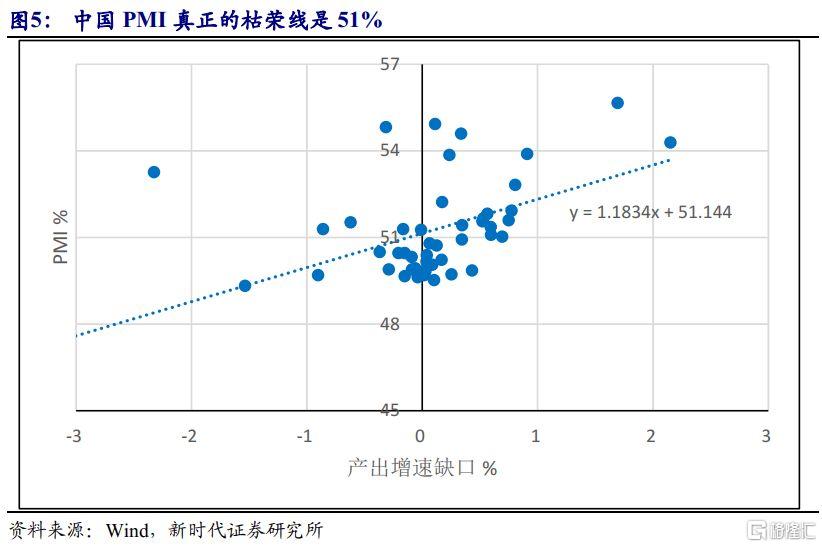

比較意外的是,次貸危機後中國製造業PMI真正枯榮線在51%左右,低於美國PMI真正枯榮線。有兩點需要說明。首先,PMI數據屬性比較複雜,體現的不是經濟增速絕對值,不能認爲中國經濟增速高於美國,中國PMI中樞就高於美國PMI。中國PMI中樞低於美國,可能體現了次貸危機後中國潛在經濟增速趨勢性下滑,而美國潛在經濟增速則是緩慢爬升。其次,中國PMI數據較短,同時,中國經濟制度、結構快速變化,潛在經增速也變化較快,中國PMI真正枯榮線波動比較大,這也是中國PMI和經濟增速缺口的擬合度小於美國的原因。

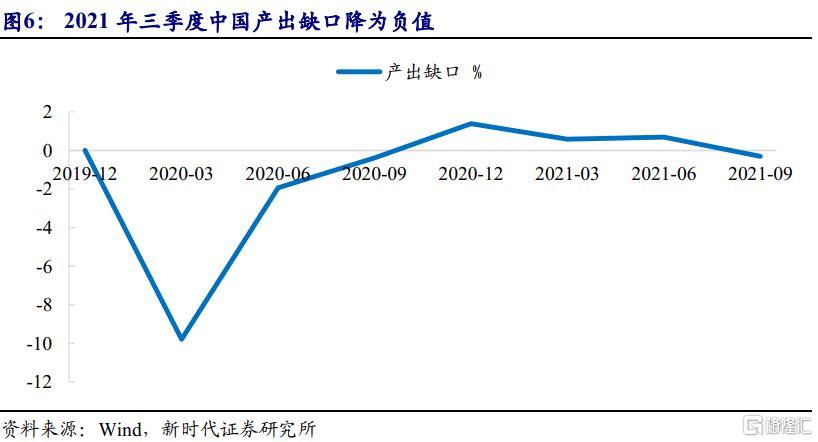

不管如何,我們傾向於認爲中國PMI真正枯榮線也是高於50%,51%是一個比較合理的估算。這也符合近期的經濟形勢。疫情衝擊下,2020年一季度PMI降至46%,低於枯榮線,產出缺口下降併爲負值,之後產出缺口回升。2021年三季度,PMI均值降至50%,低於真正的枯榮線51%,產出缺口下降並再次爲負值。10月中國製造業PMI降至49.2%,如果11月、12月PMI回不到51%附近,四季度產出缺口很難上升、甚至繼續下降。當然,以上只是大概邏輯,因爲受疫情、政策影響,中國潛在經濟增速、PMI真正枯榮線是快速變化的。

本文要探討的問題,不管是對經濟週期劃分,還是資產定價,抑或政策制定,都非常有意義。產出缺口是劃分經濟週期的最重要依據,但是產出缺口是季度數據、較難準確獲得,還是慢變量,得到真實枯榮線的PMI,可以彌補產出缺口的缺陷。

風險提示

PMI真正的枯榮線不穩定

More Content