白馬藥業衝擊創業板IPO:經銷收入佔比95%,面臨集採風險

據格隆匯新股瞭解,江西杏林白馬藥業股份有限公司(以下簡稱“白馬藥業”)日前更新招股説明書,擬登陸創業板,光大證券為其保薦人。

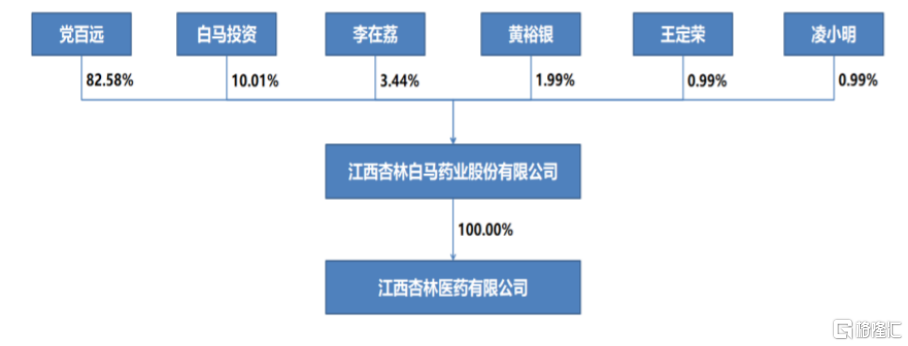

IPO前,黨百遠持股佔比82.58%,為公司控股股東及董事長。其子黨皓通過白馬投資間接持有公司0.54%股權,與黨百遠共同為實際控制人;黨百遠妻子李在荔持股佔比3.44%,三人合計佔比約86.56%。

(公司股權結構,來源:招股説明書)

01

面臨集採風險

白馬藥業是一家從事中藥及化學藥品的研發、生產和銷售的企業。自2001年成立以來,公司逐漸形成清熱解毒類、婦科類、心血管系統類藥品為核心梯隊,兒科類、補益類藥品為儲備梯隊的產品發展格局。

目前,白馬藥業擁有顆粒劑、膠囊劑、片劑、凝膠劑、煎膏劑、口服液製劑等12個劑型65個品種73個規格的藥品批准文號。其中,5個品種為公司獨家品種。主要產品包括清熱解毒類藥品猴耳環消炎顆粒、裸花紫珠膠囊,婦科類藥品保婦康凝膠、婦炎康復膠囊、八珍膠囊,心血管系統類藥品替米沙坦膠囊。

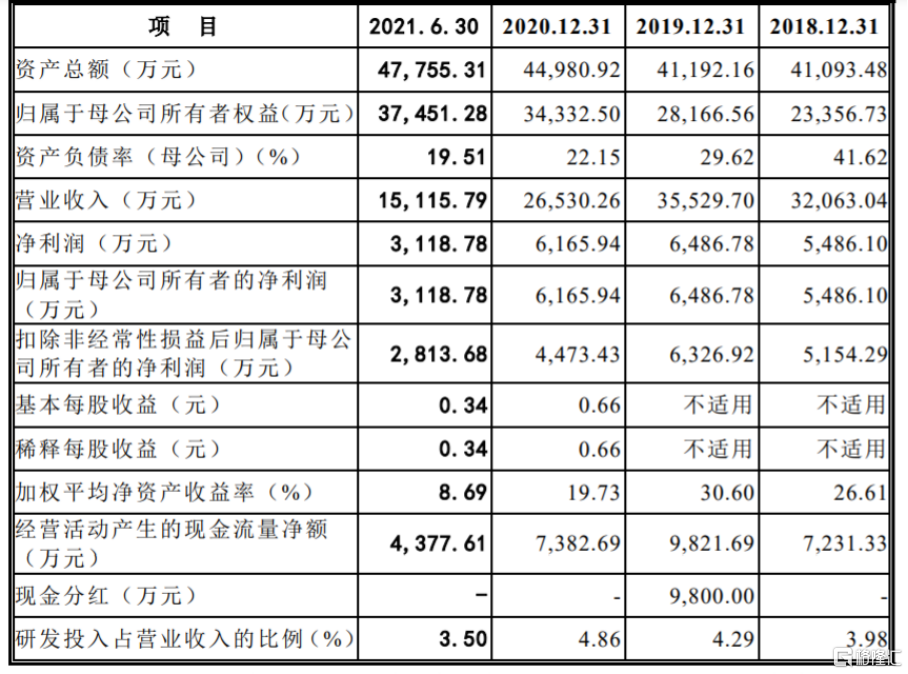

2018年-2019年,白馬藥業實現營業收入由3.21億元增長至3.55億元,歸母淨利潤則由5486萬元上升至6487萬元。2020年,受到新冠疫情的影響,公司營收及利潤雙雙下滑,實現營收2.65億元,歸母淨利潤為6166萬元。2021年上半年,隨着疫情有效控制,公司生產經營逐漸恢復。

(公司主要財務數據,來源:招股説明書)

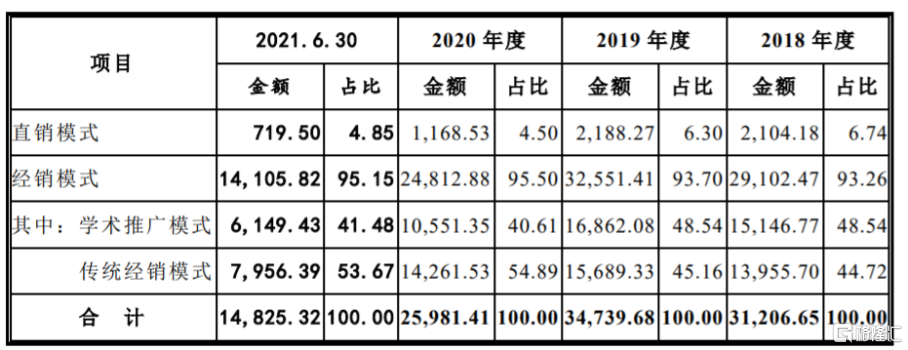

目前,公司銷售模式以經銷為主,直銷為輔,經銷收入佔比達到95%。截至2018年底,全國31個省自治區、直轄市公立醫療機構已全面實施“兩票制”,由於白馬藥業產品為各類的中成藥和化學藥,已然受到“兩票制”的規範。

(公司銷售模式結構,來源:招股説明書)

在此背景下,行業集採已至。去年12月14日,首批中成藥企業談判結果出爐,相關中成藥最終降價三分之一左右,進一步加劇中藥企業未來發展的焦慮。雖然目前白馬藥業中成藥產品品種尚未進入國家或地方集中帶量採購目錄範圍,但存在主治功能範圍與公司在售產品相同或相近的藥品品種納入。若未來其主要產品實施集採,公司不僅面臨產品大幅降價,還可能面臨不能成功中標的局面,將會對白馬藥業經營業績產生衝擊。

02

研發費用率不足5%

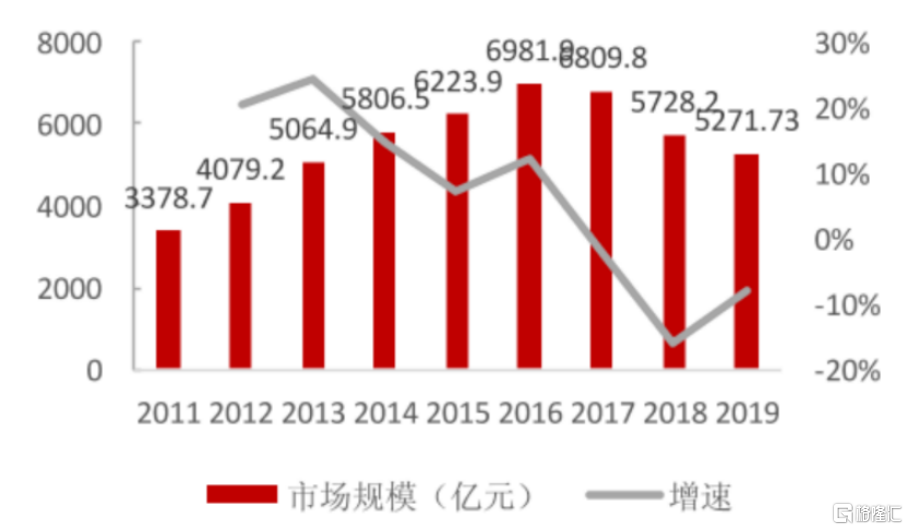

事實上,近年來公司所處的中成藥市場規模持續震盪下行。2019年,我國中成藥市場規模為5271.73億元,同比下降7.96%。一方面,由於部分中成藥營銷模式存在瑕疵,各地政府相繼出台重點監控目錄限制中成藥“野蠻生長”;另一方面,説明書修訂風波持續發酵。

(2011-2019年中成藥市場規模及增速;來源:國家統計局,粵開證券研究院)

除此之外,缺少創新亦是行業發展停滯不前的原因之一。對於中藥企業來説,中藥更講究對人全身系統的調節以及需要更長週期的治療,研發新產品所投入的時間和資本並不划算,還是吃老本來的更加舒適。這也是為什麼傳統中藥企業研發費用很低,白馬藥業的研發費用也僅有4%左右。

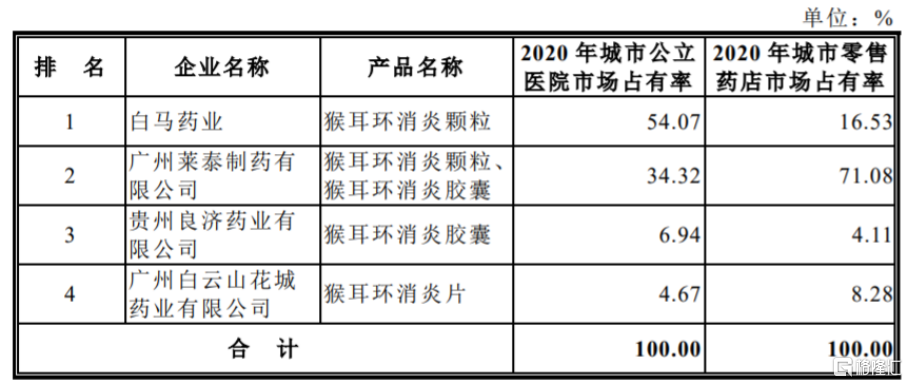

從公司核心產品市場地位來看,猴耳環消炎類藥品國內共有4家企業擁有,白馬藥業的猴耳環消炎顆粒2020年在公立醫院市佔率為54%,排名第一,而萊泰製藥在零售藥店市場以71%佔比排名第一,公司僅有16.53%市場份額。另一款裸花紫珠膠囊,公司在公立醫院中僅有16.56%份額,排名第四。

(猴耳環消炎顆粒市場排名情況,來源:招股説明書)

在婦科領域,公司的保婦康凝膠雖在公立醫院排名第二,但市佔率僅1.55%,絕大部分被碧凱藥業所佔據;婦炎康復膠囊以53%公立醫院市場佔有率排名第一,而零售市場僅有11%;八珍膠囊在公立醫院市場處於第三,佔有11%份額。

心血管領域,公司替米沙坦膠囊佔比更低,僅在零售藥店市場佔有2.82%份額。由此可見,公司核心產品並非獨家享有市場空間,且多數產品市場份額並不高,存在一定替代風險。

03

小結

雖然白馬藥業目前產品眾多,經營業績也在疫情過後逐漸恢復,但仍面臨諸多挑戰和風險。譬如:行業集採推進、創新力不足、市場競爭激烈、產品同質化且無相對優勢等等。

要知道,光靠品牌、營銷是無法令中藥企業的基業長青,只有保證源源不斷的產品生命力,才能突破重圍。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.