港股三大指數集體收漲,恆指漲0.52%報25539.54點,國指漲0.42%報8995.82點,恆生科技指數漲1.09%報6391.17點。

盤面上,電力股再度活躍領漲市場,新天綠色能源等個股大幅拉昇創歷史新高;黃金股、特斯拉概念股、光伏股、軍工股、體育用品股、石油股、鋼鐵股、煤炭等能源股普遍上漲,中石油、中石化皆大漲超4%;大型科網股多數上揚,快手大漲近9%,阿裏巴巴、美團漲1.5%,京東跌超2%,騰訊小幅收跌。 另一方面,恆大概念股繼續下挫,醫美股、保險股、內房股、教育股全天表現弱勢。今日大市成交額爲1365億港元,南下資金淨流入18.67億港元。

盤面上,電力股再度活躍領漲市場,新天綠色能源等個股大幅拉昇創歷史新高;黃金股、特斯拉概念股、光伏股、軍工股、體育用品股、石油股、鋼鐵股、煤炭等能源股普遍上漲,中石油、中石化皆大漲超4%;大型科網股多數上揚,快手大漲近9%,阿裏巴巴、美團漲1.5%,京東跌超2%,騰訊小幅收跌。 另一方面,恆大概念股繼續下挫,醫美股、保險股、內房股、教育股全天表現弱勢。今日大市成交額爲1365億港元,南下資金淨流入18.67億港元。

黃金股普漲,紫金礦業漲超5%,靈寶黃金漲超4%,灣區黃金、中國黃金國際漲超3%,大唐潼金、招金礦業漲超2%。

美聯儲主席鮑威爾出席傑克遜霍爾全球央行年會時表示,FOMC在2021年開始減碼QE可能是適宜的。減碼QE並不直接發出關於何時開始加息的信號。鮑威爾暗示美聯儲將保持耐心,以便美國經濟恢復到充分就業,這有助於緩解人們對美聯儲可能很快縮緊經濟支持政策的擔憂。

美聯儲主席鮑威爾出席傑克遜霍爾全球央行年會時表示,FOMC在2021年開始減碼QE可能是適宜的。減碼QE並不直接發出關於何時開始加息的信號。鮑威爾暗示美聯儲將保持耐心,以便美國經濟恢復到充分就業,這有助於緩解人們對美聯儲可能很快縮緊經濟支持政策的擔憂。

物流股全天走強, 京東物流漲超8%,中通快遞漲超7%,粵港灣控股漲近7%,嘉裏物流、海豐國際漲超2%,華南城漲超1%。

消息面上,8月27日晚間,中通快遞率先宣佈“快遞派費上漲”。次日,圓通、申通、百世、韻達、極兔陸續發佈派費上漲消息。僅一天時間,6家快遞公司均宣佈自9月1日起,全網末端派費每票上漲0.1元。

消息面上,8月27日晚間,中通快遞率先宣佈“快遞派費上漲”。次日,圓通、申通、百世、韻達、極兔陸續發佈派費上漲消息。僅一天時間,6家快遞公司均宣佈自9月1日起,全網末端派費每票上漲0.1元。

港口航運股繼續走強, 中遠海運港口漲超5%,天津港發展、中遠海控漲超4%,中遠海發漲超3%,太平洋航運、招商局港口、中遠海能漲超2%。

波羅的海乾散貨運價指數上週五續漲1%,周漲幅爲3.5%,且已連漲六週。海岬型船運價指數漲2%,周漲幅爲2.8%,亦連漲六週。

波羅的海乾散貨運價指數上週五續漲1%,周漲幅爲3.5%,且已連漲六週。海岬型船運價指數漲2%,周漲幅爲2.8%,亦連漲六週。

石油股表現強勢,中石化、中石油漲超4%,崑崙能源、中海油田漲超3%,中海油漲0.78%。

隨着油價大幅上漲,“三桶油”盈利能力增長強勁,今年上半年,中海油業績同比大增220%,中國石油、中國石化一舉扭虧,“三桶油”共實現淨利潤1255.18億元,創近七年以來同期最好水平。

隨着油價大幅上漲,“三桶油”盈利能力增長強勁,今年上半年,中海油業績同比大增220%,中國石油、中國石化一舉扭虧,“三桶油”共實現淨利潤1255.18億元,創近七年以來同期最好水平。

有色金屬股延續漲勢,贛鋒鋰業漲超7%,紫金礦業、五礦資源漲超6%,中國鋁業漲超5%,中國有色礦業、洛陽鉬業漲超4%。

中國有色金屬工業協會通報有色金屬上半年運行情況時表示,2021年上半年有色金屬生產、固定資產投資持續穩定增長,規上有色金屬企業實現利潤創歷史新高,經濟運行質量提升。

中國有色金屬工業協會通報有色金屬上半年運行情況時表示,2021年上半年有色金屬生產、固定資產投資持續穩定增長,規上有色金屬企業實現利潤創歷史新高,經濟運行質量提升。

煤炭股大幅拉昇,兗州煤業股份漲超5%,中煤能源漲超4%,南戈壁漲超3%,中國神華、首鋼資源漲超1%,蒙古焦煤漲0.41%。

電力股低開高走,中國電力漲超8%,華潤電力漲超7%,華電國際電力股、華能國際電力股漲超2%,大唐發電漲超1%。

電力股低開高走,中國電力漲超8%,華潤電力漲超7%,華電國際電力股、華能國際電力股漲超2%,大唐發電漲超1%。

內險股跌幅居前,衆安在線跌超4%,中國平安跌超2%,中國太保、中國再保險、中國太平跌超1%,新華保險跌0.88%。

內險股跌幅居前,衆安在線跌超4%,中國平安跌超2%,中國太保、中國再保險、中國太平跌超1%,新華保險跌0.88%。

醫療股大幅跳水,德斯控股跌超36%,康華醫療跌超8%,太和控股跌超7%,朝聚眼科跌超6%,康寧醫院跌超5%,瑞麗醫美、中國醫療網絡跌超4%。

醫療股大幅跳水,德斯控股跌超36%,康華醫療跌超8%,太和控股跌超7%,朝聚眼科跌超6%,康寧醫院跌超5%,瑞麗醫美、中國醫療網絡跌超4%。

建材水泥股走弱,海螺水泥、華潤水泥控股跌超2%,亞洲水泥跌超1%。

建材水泥股走弱,海螺水泥、華潤水泥控股跌超2%,亞洲水泥跌超1%。

海螺水泥27日披露半年報,公司上半年實現營業收入爲804.33億元,較上年同期增長8.68%;淨利潤爲149.51億元,較上年同期下降6.96%;基本每股盈利2.82元。

海螺水泥27日披露半年報,公司上半年實現營業收入爲804.33億元,較上年同期增長8.68%;淨利潤爲149.51億元,較上年同期下降6.96%;基本每股盈利2.82元。

個股異動

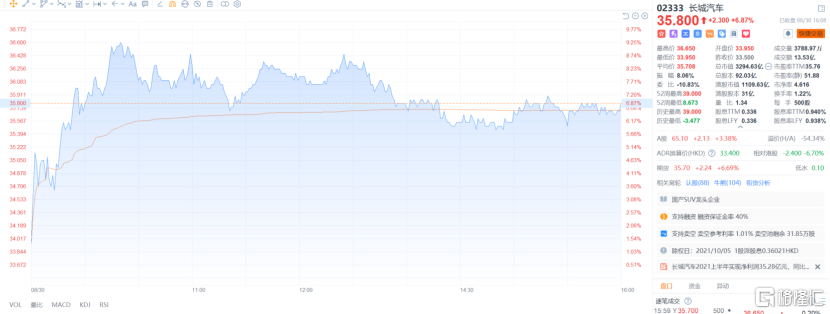

長城汽車收漲6.87%,報35.8港元/股,總市值3294.63億港元。

今日消息,長城汽車上週五(27日)晚間公佈中期業績稱,期內公司實現營業收入約619.28億元,同比增長72.36%;歸屬於上市公司股東的淨利潤約35.29億元,同比增長207.87%;基本每股收益0.39元,擬10派3元。

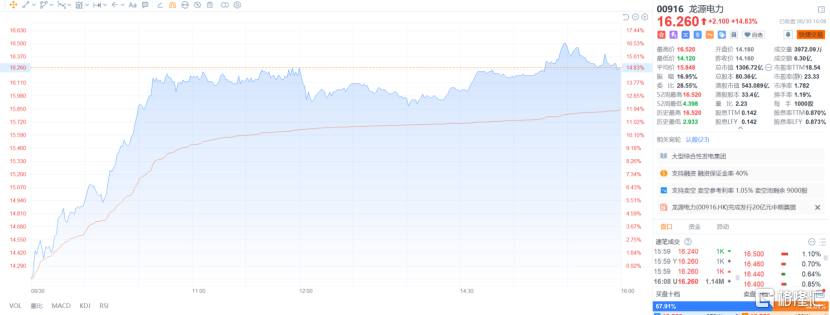

龍源電力收漲14.83%,報16.26港元/股,總市值1306.72億港元。

龍源電力收漲14.83%,報16.26港元/股,總市值1306.72億港元。

龍源電力27日公佈,上半年收入同比增長25.7%至178.77億元人民幣;股東應佔溢利同比增長36.3%至45.4億元人民幣;每股收益0.55元。溢利的增長主要是由於風電分部、火電分部淨利潤同比增長所致。另外,集團新簽訂開發協議23吉瓦,遠超去年同期水平。同時公司擬出資10億元參與設立國能低碳基金。

南向資金方面,南下資金今日淨流入-18.66億元,其中港股通(滬)淨買入-7.35億元,港股通(深)淨買入-11.31億元。

南向資金方面,南下資金今日淨流入-18.66億元,其中港股通(滬)淨買入-7.35億元,港股通(深)淨買入-11.31億元。

展望後市,興業證券認爲,互聯網作爲港股市場的中流砥柱,監管風險雖尚未消除,但近期的政策降低了極端悲觀預期的可能性。我們判斷互聯網作爲中國的競爭優勢不會輕易被廢棄,政策預期在四季度有望改善。

展望後市,興業證券認爲,互聯網作爲港股市場的中流砥柱,監管風險雖尚未消除,但近期的政策降低了極端悲觀預期的可能性。我們判斷互聯網作爲中國的競爭優勢不會輕易被廢棄,政策預期在四季度有望改善。

More Content