今日,申萬食品飲料行業漲幅0.57%,但作為行業新秀歡樂家在昨日暴漲527%之後,今日大跌逾16%。

數據來源:富途牛牛

上市企業鮮有像歡樂家這種次日翻臉的,特別在近期食品飲料行業表現都不錯的情況下。

近十年,隨着社會進步和人民收入水平不斷的提高,消費者對食品飲料偏好變化較快,對產品的口味、質量、功效、消費體驗等方面要求也在不斷提高,消費需求呈現出多樣化、個性化的趨勢。

最值得一提的是,在追求差異化產品的道路上,元氣森林以無糖泡泡水以及“網紅孵化式”模式,成功精準營銷,C位出道。

一時間得到其他飲料企業的一片豔羨,隨後各大資金雄厚的企業紛紛入局,娃哈哈、屈臣氏、農夫山泉、嶗山等大品牌均加入了蘇打水領域的混戰,紛紛妄想從中撈一桶金。

然而出圈容易長紅難,在市場競爭越來越激烈的氣泡水領域,元氣森林氣泡水似乎也沒有那麼香了。

與此相仿,早前受到韓流的影響,國內流行起蜂蜜柚子茶,彼時天喔國際靠鋪天蓋地的廣吿在短時間內建立起品牌知名度,將“天喔蜂蜜柚子茶”做成爆款,獲得了不錯的市場反饋。

但因為蜂蜜柚子茶飲品本身壁壘較低、容易複製,在各種包裝類似的蜂蜜柚子茶競品湧現出來後,紅火一時的天喔柚子茶也逐漸淡出市場。據悉,2020年11月,經營不善的天喔國際正式從港交所退市。

歡樂家遠沒有那麼幸運,與這些靠一個爆款打開品牌知名度的飲料企業相比,它並沒有一款讓全世界都知道它存在的“神奇水”,但是它卻憑藉其20年的市場深耕上市了。

不過,歡樂家上市兩日,股價表現猶如過山車,不知是不是市場發現了它的什麼祕密?

歡樂家是一家名正言順的家族企業,2001年成立於廣東湛江,實際控制人為李興、朱文湛和李康榮。其中,李興和朱文湛系夫妻關係,李康榮系李興之弟,3人直接和間接合計控制歡樂家93.19%的股份。

公司主要銷售區域位於華中、西南、華東和華北,佔比80.26%,其中湖北是公司的重點銷售省份。近幾年受產品老化影響,公司業績增長乏力,去年在疫情下,業績快速下滑。

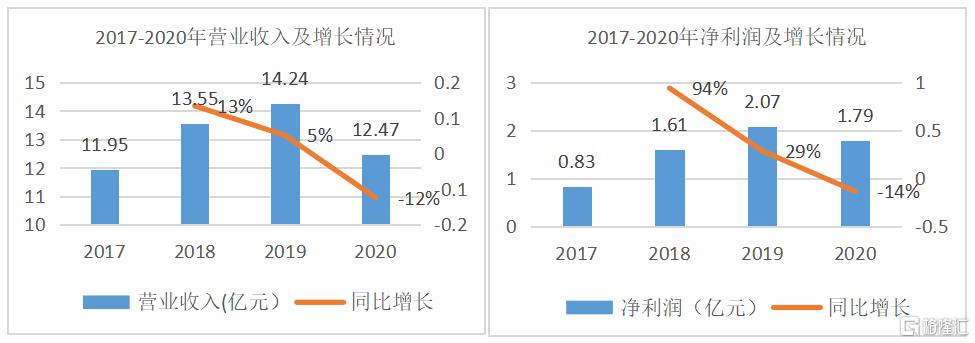

2020年公司實現營收12.5億元和淨利潤1.79億元,分別同比下降12%和14%。

今年隨着國內經濟復甦,2021年1季度公司實現營收3.4億元和淨利潤4691萬元,分別同比增長33.62%和54.8%,但這僅僅説明疫情以來公司經營恢復。實際上,公司業務拓展不佳,規模增長表現依舊疲軟。據公司公吿,公司預計今年上半年營收規模實現增長在5.36%-13.72%之間,淨利潤增長在1.42%-12.04%之間。

(由於2020年受疫情影響,此處以2019年公司數據對公司其他方面進行説明)

公司產品包含水果罐頭、植物蛋白飲料、果汁飲料、乳酸菌飲料等食品飲料產品線。其中,水果罐頭和植物蛋白飲料(椰汁)是公司的兩大類產品,2019年分別實現收入5.63億元和8.55億元,分別同比增長1%和8%,分別佔比47%和52%。

數據來源:公司年報,時代商學院

2019年公司兩大類產品增長動力已明顯不足,公司產能利用實際更是低下。公司產品產能利用率除旺季(春節、中秋等)勉強能達到70%,其餘時候公司產能利用率低下。2019年公司罐頭產品和飲品年產能利用51%和34%,旺季產能利用率為82%和69%。

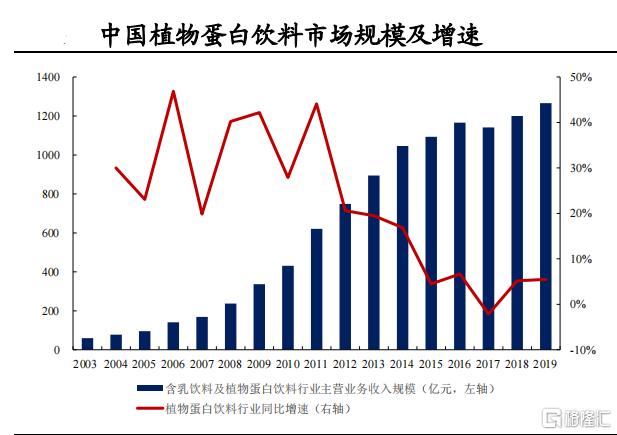

公司椰汁產品屬於植物蛋白飲料行業,該行業增速自2015年開始放緩,2017 年遭遇負增長,2019年市場規模達到1266億元,2015-2019年年複合增長率僅為3.7%。該階段行業進入者增加,從2018年的283家激增至2019年的4074家,眾多乳企也開始植物蛋白飲料業務,市場競爭愈發激烈。

(數據來源:興業證券)

競爭激烈的市場競爭下,若沒有一定的品牌優勢,很難與同類企業競爭。相比同類上市企業,公司的毛利率低,淨利率則更少了。

2020年公司毛利率為39%,而養元飲品(核桃露)和承德露露(杏仁露)毛利率分別為48%和50%,公司至少低了9個百分點。

2020年公司淨率為12%,而養元飲品和承德露露毛利率分別為35%和19%,公司至少低了7個百分點。

(數據來源:choice數據)

目前歡樂家在市場上是個沒有品牌實力的選手,公司產品老化,產能利用率不足。

然而此次公司融資4.92億元,其中用於年產13.65萬噸飲料、罐頭建設項目2.58億元,營銷網絡建設項目2 億元,即公司購置50,000台自助智能零售終端投放於目標銷售市場。

經前面分析,公司這兩項投建項目沒那麼必要。

一來公司產能常能利用率不足,而這一擴增又多出了五分之一,後續公司產能能否被市場消耗實在是個迷。

另外,在產品方面,雖然它是國內水果罐頭龍頭,但是市場規模並不高,且傳統上新鮮水果更符合大多數消費者的需求。而公司最大的椰汁飲品,年銷售額不到五個億,相比椰樹集團150億元的營收,70%的市場佔有率,公司被完全碾壓。

如今公司要在下游渠道提供能零售終端,眾所周知,產品品牌實力不夠是很難玩轉這種無人銷售的機器的。試想一下,你會在路邊買一個不知名的食品嗎?

總而言之,飲料行業是個完全競爭行業,同質化產品極高,過去飲料企業光靠一兩個大單品的湧現雖然能有“一石激起千層浪”的效果,但這些企業想要長期存活很難。

對於沒有產品優勢的企業,想要存活更難。未來歡樂家能否走上正軌還未知曉,但其募投項目大概率是無法幫助它改善現狀的吧。

More Content