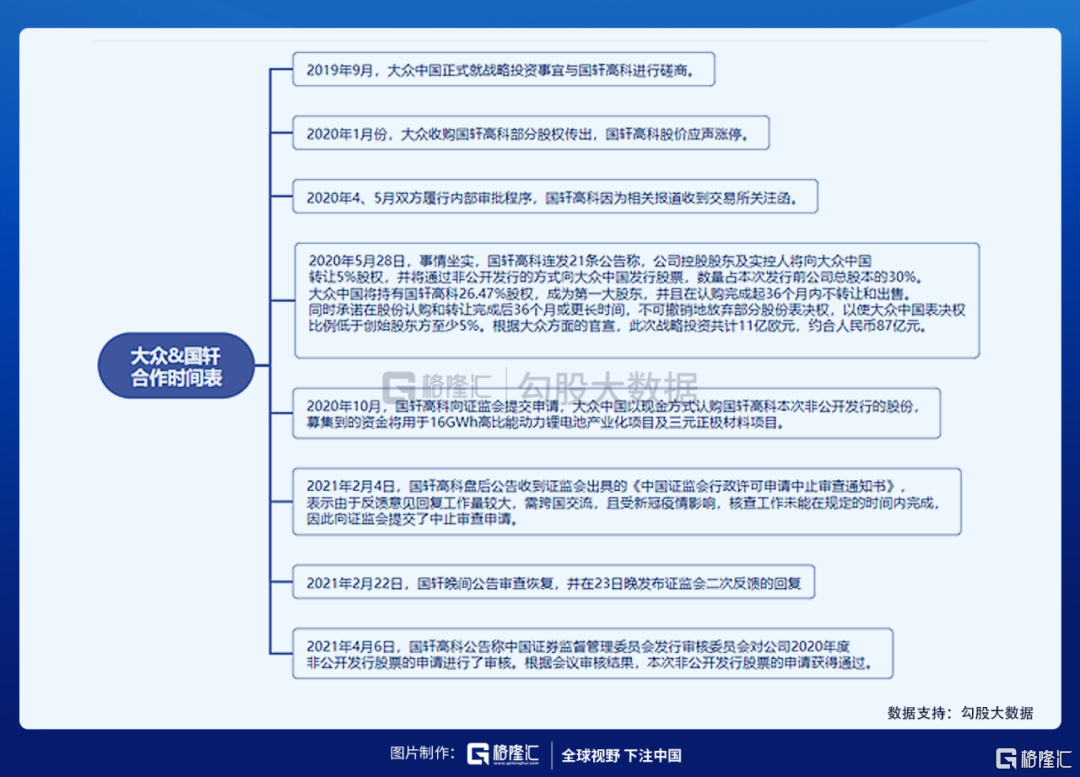

4月6日,國軒高科發佈公吿稱,中國證券監督管理委員會發行審核委員會對公司2020年度非公開發行股票的申請進行了審核。根據會議審核結果,本次非公開發行股票的申請獲得通過,這意味着大眾中國此前入股國軒高科的計劃正式通過審查。

終於,靴子落地。

實際上,大眾中國尋求控股國軒高科的計劃由來已久。

一年半的一波三折,國軒和大眾的合作終於敲定。大眾中國將持有國軒26.47%的股權,此次戰略投資共計11億歐元,約人民幣87億元,募集資金國軒將用於16GWh動力鋰電池產業化項目和高鎳三元正極材料項目。而有一點非常重要的是,大眾中國承諾目前沒有且未來3年也沒有計劃作為收購入股其他電池公司的計劃,這意味着國軒高科對於大眾有唯一性。

01

為什麼是國軒?

大眾選擇國軒其實也不奇怪。

一則,德國汽車雖然有自己的整車優勢,但是做純電動汽車是一個需要持續砸錢卻短期內看不到收益的長線投資,從開始到量產車至少需要三年的時間。在這種情況下,整車廠的成本很受政府補貼和中上游材料價格的影響。所有的整車廠都需要跨過電池這道坎,只有自己做電池才能更有力地控制成本。而收購電池公司是能夠“自己做電池”最快的方法。

二則,大眾之所以會跳開比亞迪和寧德時代,一方面是因為寧德和比亞迪的市佔率已經很高,兩家加起來超過65%,無論選誰都會助長一家獨大的局面。另一方面大眾和這兩家只能談合作,是不可能像入股國軒一樣收購寧德或者比亞迪。

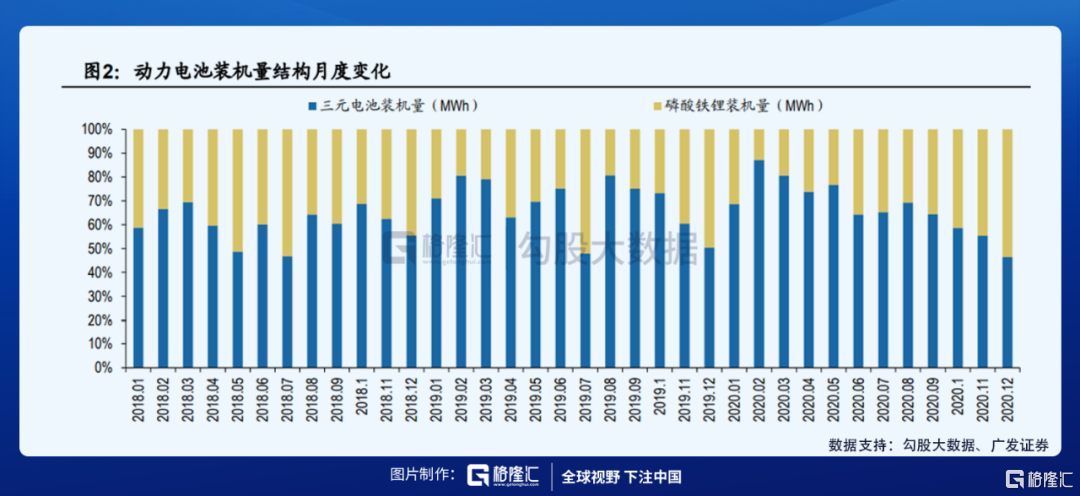

三則,由於五菱宏光Mini,Model 3以及比亞迪漢等磷酸鐵鋰車型的熱銷,加上本身的成本優勢,磷酸鐵鋰在動力電池的裝機量開始回温。據中國汽車動力電池產業創新聯盟,2020全年磷酸鐵鋰電池裝車量累計24.4GWh,同比增長20.6%,佔總裝車量38.3%,同比增長15.6%, 2020年Q4磷酸鐵鋰電池共計裝車14GWh,同比上升149.3%,環比上升69.1%,磷酸鐵鋰裝機量佔比從2020年初的12.83%提升至53.51%,增長趨勢顯著。

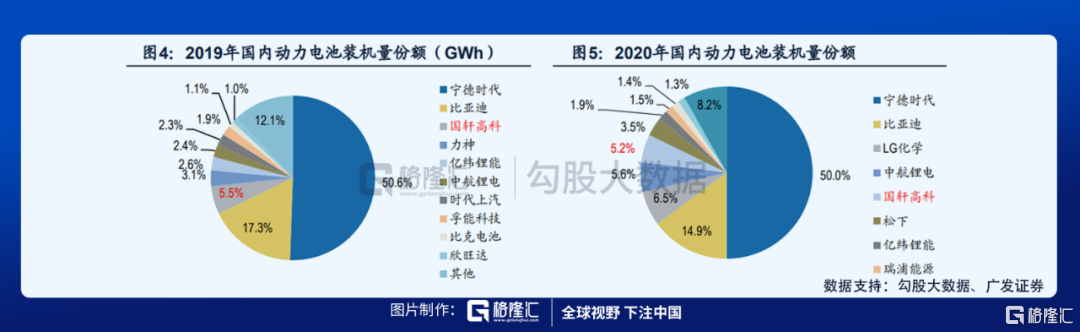

四則,國軒高科主營的動力電池產品是磷酸鐵鋰電池。2019年國內磷酸鐵鋰電池裝機量為19.98Gwh,國軒高科磷酸鐵鋰電池的裝機量為2.85GWh,超過了比亞迪磷酸鐵鋰電池的裝機量,僅排在寧德11.43Gwh裝機量之後。據中國汽車動力電池創新聯盟數據,2020年公司動力電池裝機量3.32GWh,國內市佔率5.2%排名第五。據SNE數據,2020年公司動力電池裝機量全球份額約2.2%。今年1月,國軒高科發佈了210Wh/Kg磷酸鐵鋰軟包電芯及JTM技術產品。根據官網介紹,能量密度達到三元NCM5系水平,業界領先。

02

大眾入股能給國軒帶來什麼?

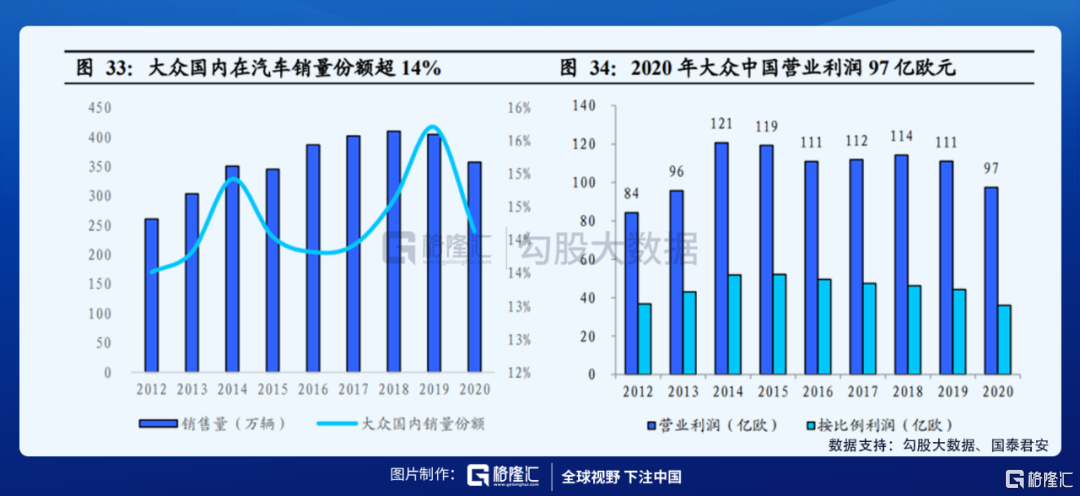

首先來看看大眾的銷量,2020年受疫情影響下,大眾國內總共銷量為385萬輛。大眾新能源汽車全球總共交付為37.18萬輛,全球佔比13%,僅次於特斯拉的16%(49.95萬輛)。大眾中國新能源汽車交付5.23萬輛,佔大眾新能源汽車銷量14%。

根據大眾Power Day會議披露,2021年大眾全球電動車銷量目標為100萬輛,在中國市場上,2025年大眾旗下各品牌將有15款基於MEB平台的車型實現本土化生產,屆時大眾電動化車型將佔集團在華車型的35%,新能源汽車的年交付總量將達到150萬。

根據大眾規劃,2020年開始將基於MEB平台密集投放新車型,其中首發量產車型ID.3於2020年9月起正式在歐洲交付,起售價37350歐元,WLTP標準續航里程420km。ID.4定位純電動緊湊型SUV,續航里程超550km,國內補貼後售價不超過25萬元,將於2021年上半年上市。據電車匯消息,ID.1/2或將分別於2025、2023年上市,其中ID.2有望搭載磷酸鐵鋰電池進一步打造低成本爆款車型。

簡單算一下,如果按2021年大眾100萬輛新能源汽車的銷量,中國區佔比提升至16%,則大眾2021年國內新能源汽車銷量為16萬輛,平均每輛車帶電量為80Kwh,則大眾對國軒的電池需求量為12.8Gwh。目前,國軒的電池產能為28GWh,預計國軒2023年電池產能將提高至80GWh,2025年提高至100GWh。

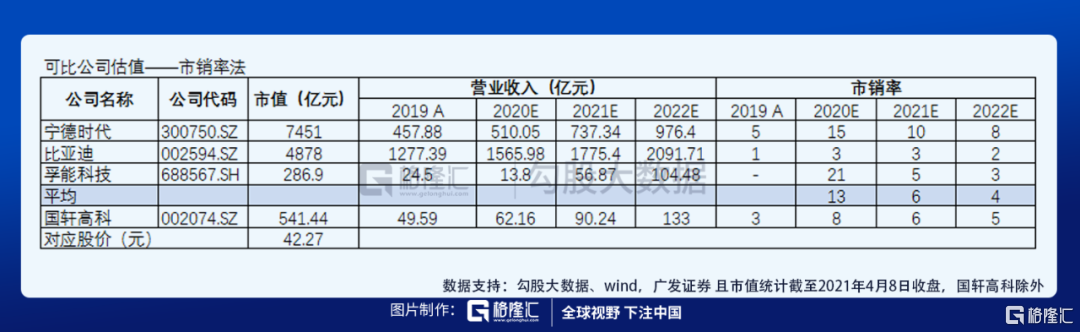

根據公司公吿,預計2020年歸上淨利潤為1.3-1.7億元,同比增長153.64-231.68%。也有券商預測,國軒2021一季度淨利潤增速為7282%,預計全年淨利潤約4.9億元。預計2020-2022年底動力電池名義產能可達28GWh、44GWh和54GWh,受益於動力電池行業中高速增長,考慮產能爬坡因素對應銷量可實現8GWh、13.3GWh和19GWh,複合增速約51%。

預計公司2020-2022年EPS為0.13/0.45/0.69元/股,營收62.16/90.24/133.00億元。公司2020年開始處於內部管理機制調整階段,壞賬與存貨減值等發生較多,淨利潤無法充分反映此階段公司產品能力,而2021年後銷售額以磷酸鐵鋰技術優勢加快增長,尤其在A00級車型及儲能市場不斷放量,因此採用市銷率估值方法更加合適,公司對標動力電池可比公司平均估值約6倍PS,考慮公司尚未突破國際一線車企,技術優勢兑現仍需時日,給予2021年可比公司6倍PS,合理價值42.27元/股。

More Content