業績持續被驗證,新寶股份才是小家電龍頭?

公司以代工小家電業務起家,有多年的ODM代工生產經驗,客户有眾多的全球知名企業,去年海外疫情爆發,公司出口業務迎來高速增長。最近幾年,新寶推出了自由品牌東菱,摩飛,萊卡等;憑藉電商渠道打造了爆款品牌摩飛。

從代工龍頭走向品牌化

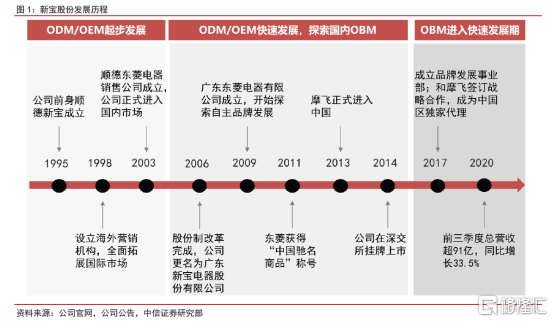

新寶的發展大致可以分為三個階段:

第一階段:1995年,新寶以家庭小作坊的形式成立,創業之初以生產電吹風為主,逐漸地把產品線擴充到了咖啡機,電熱水壺和攪拌機等產品;同年新寶成功殺入歐美市場,並在1998年成立海外銷售公司,積極發展海外市場,直到目前出口業務仍然是公司最重要的銷售渠道,佔比在90%左右。

第二階段:2006 年,公司完成了股份改革,並改名為廣東新寶股份有限公司。2009年,廣東東菱電器公司成立,並且開始探索自主品牌業務。東菱品牌有一段時期在國內市場被點爆,但隨着營銷模式的落後逐漸開始沒落。

第三階段:2017年,新寶積極與海外品牌客户摩飛開展合作,成為摩飛在中國的獨家品牌代理。到目前這個階段為止,公司也從ODM模式逐漸轉型為OBM模式。

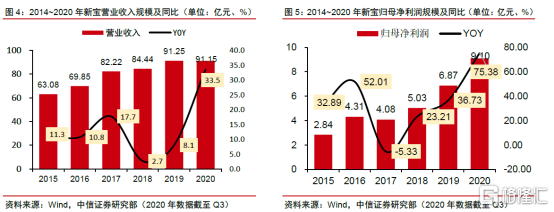

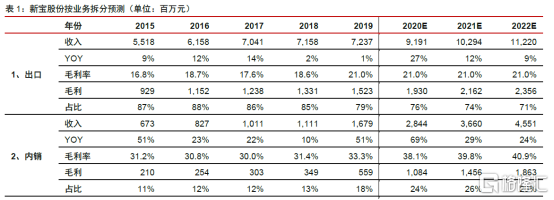

隨着中國加入WTO,新寶的業務收入也在突飛猛進。2015年-2019年期間,公司收入增長超過60%,歸母淨利潤增長2.3倍。發展至今,公司客户已經包括飛利浦,西門子,松下等知名企業。

經過20多年的發展,公司已經從最初的小作坊發展成國內小家電代工的龍頭公司。同時隨着國內品牌摩飛的崛起,公司在估值方面也被拔高。

內銷品牌崛起拔高估值

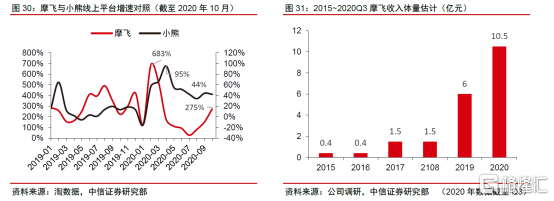

1998年摩飛成為新寶的代工客户,2013年新寶以支付品牌使用費的方式取得了摩飛在中國區的獨家運營權。

在疫情的影響下,由於產品都是線上銷售,摩飛2020H1的業績已經超過去年全年。淘數據顯示,摩飛品牌的爆發式崛起是在2018年第四季度:多功能料理鍋上線增速超過200%,在2020年第一季度增速仍然超過200%。

從產品端來看,摩飛品牌的崛起核心在於:1、精準定位年輕化用户羣體;2、深入挖掘潛在需求,打造差異化產品。

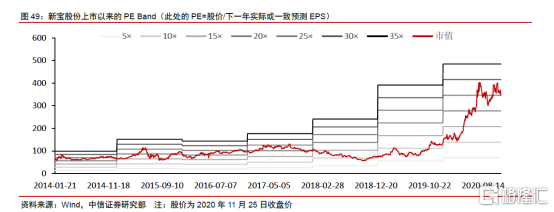

雖然目前新寶國內業務佔比不到30%,但是這個比例從2015年的10.7%提升到2020年的24%。自主品牌的崛起也提高了市場給與公司的估值。不僅僅因為出口業務增速快,很大一部分原因是來自內生性成長,估值從2019年的15倍拔高到了30倍。

目前來看新寶國內業務佔比24%,到2022年有望達到30%,其中60~70%為自主品牌,對應總收入約20%將為自主品牌收入。參考自主品牌和ODM 代工企業估值,其中自主品牌可比公司對應2020 年PE 估值平均值約為28 倍,ODM 可比公司約22倍。

新寶當前估值35倍,2021年估值29倍,考慮到公司供給端優勢地位和自主品牌快速增長,當前的估值還具有吸引力。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.