估值漂移,敏華控股(1999.HK)還有多少上漲空間?

公司以代工軟體家居業務起家,後來孵化自有品牌芝華士,成為全球功能沙發的領先品牌,目前在國內市場的市佔率高達50%。敏華的這一波上漲,不僅僅因為業績出色,同時估值已經發生了根本性切換,從製造業公司轉變為消費品企業。

從代工龍頭走向品牌化

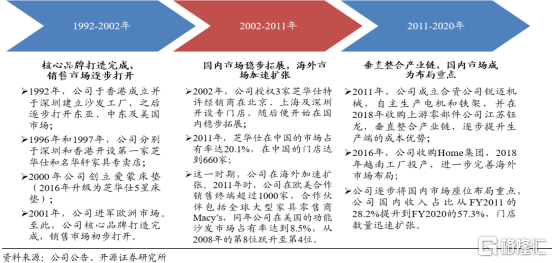

敏華的發展大致可以分為三個階段:

第一階段:1992年,公司在香港成立並於深圳建立沙發工廠,之後逐步打開東亞、中東及美國市場。1996 年和1997 年,公司分別於深圳和香港開設第一家芝華仕和名華軒傢俱專賣店。

第二階段:2002 年,公司授權3 家芝華仕特許經銷商在北京、上海及深圳開設專門店,隨後開始在國內市場穩步拓展。2011 年,芝華仕在中國的功能沙發市佔率達20.1%,在中國的門店達到660 家。同時這一時期,公司在海外加速擴張。2011 年時,公司在歐美合作銷售終端超過1000 家。

第三階段:2011 年,公司成立合資公司鋭邁機械,自主生產電機和鐵架,並在2018 年收購上游零部件公司江蘇鈺龍,垂直整合產業鏈,逐步提升生產端的成本優勢。

在業務拓展上,2016 年,公司收購Home 集團,2018 年越南工廠投產,進一步完善海外市場佈局。另一方面,公司逐步將國內市場作為佈局重點,公司國內收入佔比從FY2011的28.2%提升到FY2020 的57.3%,門店數量迅速擴張。

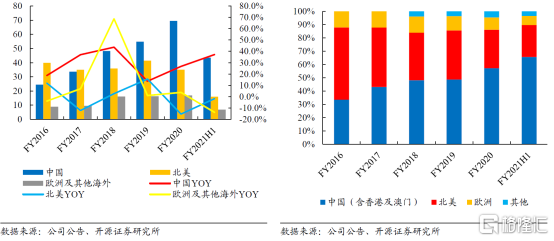

分市場來看,2020年公司在中國市場收入為為69.6 億港元(+26.7%),佔比57.3%,;在北美市場的收入為35.1 億港元(-15.4%),佔比28.9%;歐洲及其他海外市場收入為16.8 億港元(+3.8%),佔比13.9%。

其中中國市場為主要市場,收入從2015年20.7億港元提高到2020年的69.6億港元,收入佔比從31.5%提升到57.3%。

公司旗下芝華仕品牌在中國功能沙發的市場市佔率達50.1%,屬於絕對龍頭。並且,公司在內銷市場正在加速開店以搶佔市場份額。截至2020 年9 月30 日,公司擁有線下門店3532 家,對比2020 財年末淨增加658 家門店,並且在未來兩到三年內仍有望保持較快的開店速度。

竣工回暖下的景氣週期

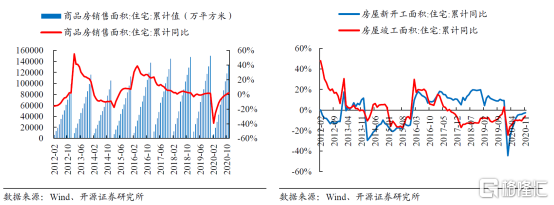

通常來看,從新開工到交房的週期一般不會超過3 年,因此2017 年至今的竣工缺口已經接近亟待回補的臨界點。所以,雖然受疫情影響,竣工回補的結點又有所推遲,但我們認為在疫情影響趨弱後,竣工數據已經逐步修復,尤其是2020 年10-11 月竣工回暖的數據已經有所加快。

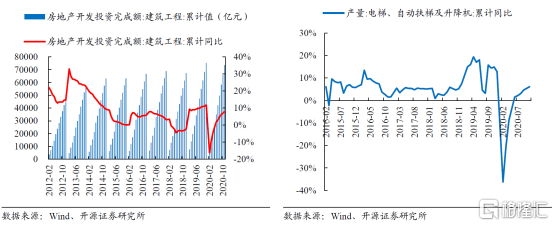

2019 年建築工程投資額、電梯以及平板玻璃產量等竣工前瞻指標累計同比均處於近年高位,對竣工回暖的預期提供了一定支撐。

2019 年1-12 月,建築工程投資完成額、電梯產量和平板玻璃產量分別同比增長11.8%、12.8%和6.6%。最終反映到竣工數據上,我們也可以看到2019H2 竣工數據快速修復,並且全年竣工累計同比最終轉正。

而2020 年雖然受到疫情衝擊,但交房的前瞻指標相比直接的竣工數據也展現了更快的修復速度。2020 年1-11 月,建築工程投資完成額和電梯產量分別累計同比增長7.9%和6.1%。

敏華的成長得益於短期內快速開店紅利,長期來看,同時受益於功能沙發市場集中度的提升和竣工週期的回暖。當前公司的估值已經在向消費品公司切換,對應2021年估值28倍,2022年估值23倍;作為具有品牌消費類屬性的公司來説,估值方面有明顯優勢。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.