昨晚,曾被網民稱作“互聯網頭號流氓”的二三四五爆了顆大雷。

1月24日晚間,二三四五發布關於2020年度計提資產減值準備的公吿,2020年度擬計提各項資產減值準備合計12.41億元—13.93億元,預計虧損近10億元。

此外,二三四五還公佈了2020年度的業績預吿,同樣大幅虧損。2020年度,該公司營業收入為11.5億元—14億元;扣非淨利潤為虧損8.4億元—10.4億元,比上年同期下降221%—248%。

兩份文件發佈後,今日股價果然做出了反應。截至收盤,二三四五全天封死漲停,股價現報1.95元,成交額8782萬元,最新總市值111.6億元。

鼎盛時期,二三四五市值曾高達750多億元。截至目前,與2015年3月創下的112.75元歷史高點相比,二三四五股價已累計跌去近100%。昔日的互聯網巨頭,難道終究要走上退市之路?

二三四五業績表現如此之差,主要有三個原因。

(1)市場份額下滑

首先是受疫情影響,客户的互聯網推廣支出有所減少,公司的互聯網推廣活動也因疫情受到一定的影響。事實上,從2019年開始,該公司無論移動端還是PC端業務收入都出現大幅下滑的趨勢,去年的疫情更是大大加速了這一趨勢。

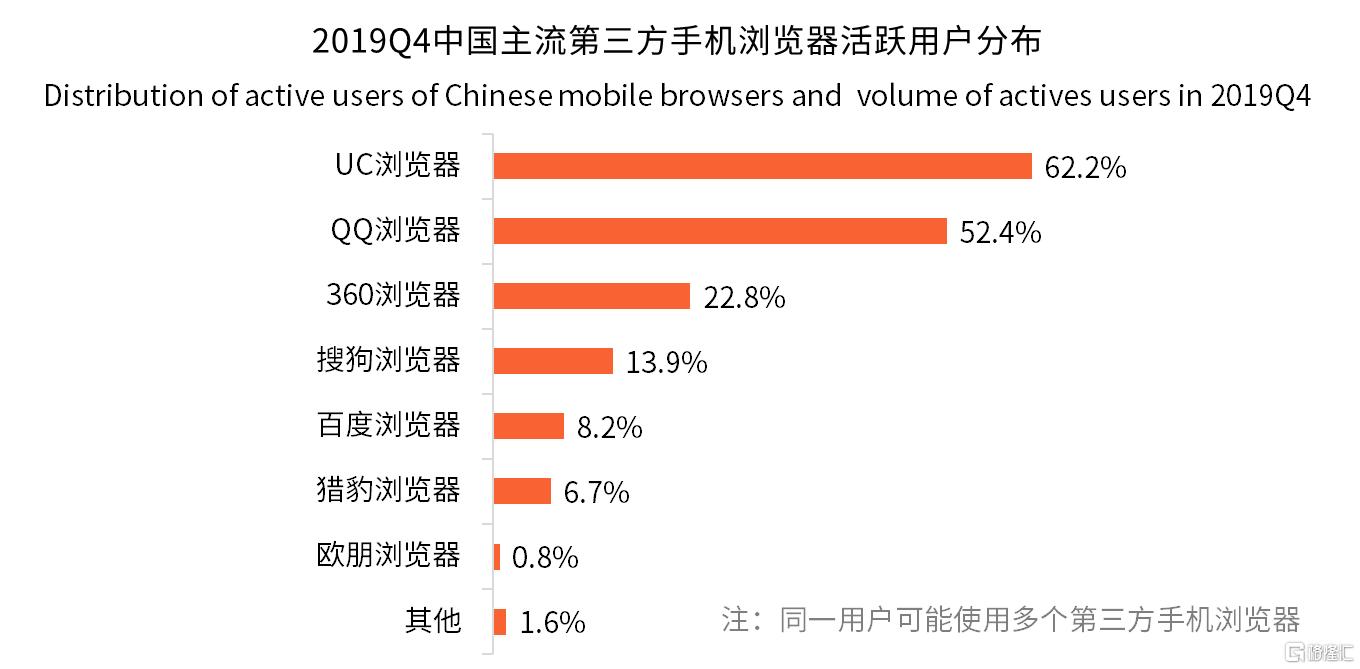

數據顯示,2016年,二三四五旗下拳頭產品2345瀏覽器市場份額排名還超過了搜狗瀏覽器,僅次於360瀏覽器、QQ瀏覽器,居國內瀏覽器第三位。然而到現在,無論PC端還是手機端,排名前10位的瀏覽器都已見不到2345的影子。

其實,早在2016年之前2345稱霸瀏覽器市場的階段,這家公司的產品在用户羣體中就已臭名昭著。不僅惡意木馬,軟件捆綁,廣吿彈窗等現象層出不窮,並且還有難以卸載、惡意推廣等卑劣行徑。種種原因,使2345當年曾被冠以“中國互聯網毒瘤”的稱號。

因此,其市場份額的下滑在情理之中,而這也或是其互聯網推廣收入萎縮的根本原因。

(2)互聯網金融業務受挫

其次是受互聯網金融服務業務市場環境變化的影響,二三四五在2019年度對互聯網金融服務業務進行調整。

這部分業務的收入降幅是最大的,2018年,二三四五的互聯網金融業務收入還高達18億元,2019年則只有10億元。2020年前兩個季度,該項業務收入只餘1.05億元,同比上年降餘83%。

數據來源:IFinD

2015年2月,二三四五募資48億投入互聯網金融業務。所謂互聯網金融業務,實則是指其現金分期金融產品“2345貸款王”、“2345車貸王”和麪向B端商户的“2345商貸王”等產品。2017年,該項業務甚至佔到二三四五毛利構成的65.5%。

然而從2018年開始,國家對互聯網金融加強監管,開展相關業務的公司都已經出清,二三四五亦於2019年度開始對互聯網金融服務業務進行調整,收入佔比較大的現金貸業務被叫停,導致該公司營業收入呈逐年下滑之勢。

值得一提的是,在互聯網金融業務折戟後,二三四五開始尋求新的業務轉型。2018年開始大力發展區塊鏈等金融創新領域,2020年5月又啟動並確立了“移動互聯+人工智能”的發展戰略。但目前來看,頻頻轉型並未能挽救該公司逐年下滑的業績。

(3)商譽減值

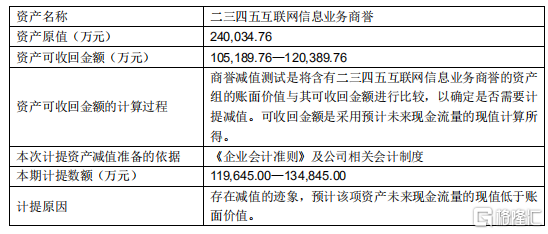

最後,則是二三四五在2020年大約12億元-13.5億元的商譽減值。商譽減值暴雷是二三四五2020年度業績形成鉅額虧損的主要原因,而這筆商譽還要追溯到2014年。

當年,二三四五的前身海隆軟件通過實施重大資產重組,收購上海二三四五網絡100%股權,完成了從軟件外包廠商向軟件、互聯網綜合平台的轉型。但與此同時,公司也形成了24億元商譽。

數據來源:公司公吿

正是因為這筆商譽存在減值跡象,二三四五才擬對該部分商譽計提減值準備11.96億元至13.48億元。

另外,在業績虧損、轉型不利的情況下,二三四五高管及大股東頻頻減持的消息,更是給投資者的心頭澆了盆涼水。

2020年5月13日至2020年10月30日期間,浙富控股於通過集中競價交易和大宗交易的方式合計減持2.47億股,佔公司總股本的4.23%。同時,浙富控股計劃自2020年11月2日起的六個月內減持公司股份不超過3.26億股。

2020年初,浙富控股還以9.93%的持股比例位居二三四五第一大股東。截至2020年10月30日,浙富控股持股比例僅餘5.7%。

數據來源:公司公吿

另外,自2013年11月海隆軟件重大資產重組停牌起,原實控人及法人包叔平及一致行動人曲水信佳就減持2.6億股,在不到6年的時間裏減持至持股比例僅2.23%,失去實控人地位。也就是説,從2017年11月2日起至今,一直都處於無實際控制人狀態。

雖然2020年業績預虧,是二三四五上市後首度虧損。但這家公司背後的問題,恐怕遠遠沒那麼簡單。

More Content