機構:信達證券

評級:買入

本期內容提要

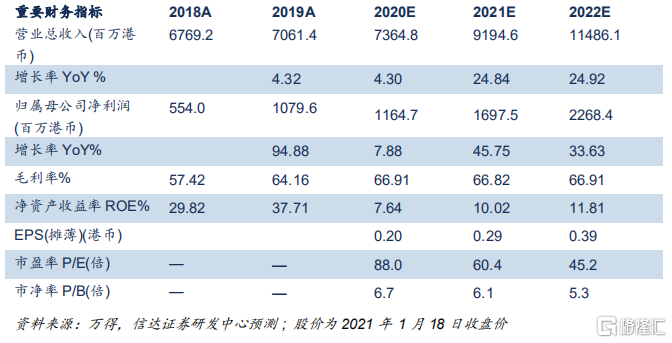

國內洗衣液與洗手液龍頭品牌商。公司成立於 1994 年,是洗衣液及洗手液行業龍頭品牌商,同時佈局廚房衞浴等家居清潔產品;其中洗衣液連續11 年市場第一,19 年市場份額超過 24%,洗手液連續 8 年市場第一,19年市場份額超過 17%,家居清潔尚在培育期,市佔率排名第五,19 年市場份額為 1.7%。2020 年 12 月公司港交所上市,實際控制人持股比例超過 75%,股權集中。近年來公司收入平穩增長,歸母淨利率提升帶動業績高增長,截止 2019 年,公司收入 70.5 億港幣,17-19 年複合增速為12%,歸母淨利潤為 10.8 億港幣,17-19 年複合增速為 254%。

品類升級及新品類普及推動家清行業平穩增長,對標海外集中度品牌商格局有提升空間。根據 Frost&Sulliva 數據,2019 年中國家清行業市場規模為 1108 億元,15-19 年複合增速為 5%,行業平穩增長;對標美國、日本成熟市場,2019 年中國家清人均支出佔比存在一倍以上提升空間。品類升級與新品類普及提升是驅動行業增長重要因素,例如洗衣液佔比衣物清潔行業僅 40%,將持續替代洗衣粉,衣物柔順劑、地板清潔劑等品類逐步普及帶來新市場。我國家庭清潔行業品牌商集中度較高,2019 年衣物清潔、家居清潔、個人護理領域 CR3 分別為為 48%、61%、65%,相比於日本、美國發達市場超過 80%的集中度存在提升空間,例如衣物清潔領域日美 CR3 分別為 92%、83%,頭部企業有望藉助渠道資源、品牌積澱及資金實力進一步提升市場份額。

產品持續創新、重視終端用户運營、流量變化敏鋭、信息化前瞻佈局為公 司長期穩健發展護航。其一,公司具備紮實研發基礎,善於產品創新,為產品持續迭代提供基礎,公司 2008 年及 2015 年國內首創洗衣液及濃縮洗衣液,掀起品類升級革命,樹立專業化品牌形象;其二,公司注重終端消費者運營,強化品牌心智,自 2009 年加大線下促銷人員對消費者對接,2015 年創新 O2O 模式增強與用户溝通,頭部品牌中藍月亮品牌享受溢價;其三,公司流量變化敏鋭,線上滲透率超過行業平均水平 15pct;其四,前瞻信息化佈局提升產業鏈運營效率,增強終端洞察,提升渠道管理精細化程度及生產效率,為長期發展奠定基礎。

渠道優化及濃縮洗衣液新趨勢提升衣物清潔市場地位,加大推新有望打開家居清潔天花板。未來公司將在衣物清潔及手部清潔領域繼續深耕,同時補足家居清潔領域短板,具體而言:1)優化渠道佈局,加大終端下沉力度,擴展品牌終端觸達率:公司近年推出針對分銷商的數據系統以及針對終端促銷人員管理系統,提升線下分銷渠道管理效率;同時進行分銷商優化,淘汰合作不佳分銷商,加大優質分銷商資源開拓,擴大網點下沉深度。 2)濃縮洗衣液方興未艾,公司作為行業領引者有望借得先機搶佔流量: 19 年海外發達市場濃縮洗衣液滲透率超過 90%,中國市場僅 8%,未來提升空間大,公司作為國內濃縮洗衣液標杆,約 28%市場份額,未來有望加大市場培育提升份額。3)加大推新,率先佈局家居清潔領域,提升細分市場份額:19 年公司新出 4 款高端產品,重點佈局廚房及衞浴領域,有望拉動細分領域增速。

盈利預測與投資評級:我們看好品類升級迭代以及新興產品滲透率不斷提升對產品家庭清潔行業推動作用,行業保持平穩增長,同時藍月亮作為洗衣液、洗手液等升級品類龍頭品牌商,將通過渠道延展優化以及前瞻新品佈局提升份額,未來可期。我們預計公司 2020-2022 年收入分別為 74 億港幣、92 億港幣、115 億港幣,同比增速分別為 4%/25%/25%,歸母淨利潤歸母淨利潤分別為 11.65 億港幣、16.98 億港幣、22.68 億港幣,對應增速分別為 8%、46%、34%,根據最新收盤價(2021 年 1 月 18 日)對應 PE 為 88 倍、60 倍、45 倍;根據相對估值法,與化粧品公司相比,公司 PEG 為 3.1 倍,低於可比公司 4.4 倍平均水平;根據絕對估值法,假設公司半顯性增速為 15%,永續增速為 1.5%,WACC 為 8.4%,每股合理內在價值為 21.95 港幣,存在低估;首次覆蓋,給予“買入”評級。

股價催化劑:渠道擴展進度及優化效果好於預期、至尊濃縮洗衣液及其他新品類市場推廣效果好於市場預期,衣物清潔行業消費升級進度加快。

風險因素:1)渠道優化及延展不達預期;2)新品銷售不達預期;3)原材料成本上漲及費用未能優化進而影響利潤率提升;4)市場格局惡化影響份額提升。

More Content