發生了什麼?券商率先暴漲,A股中信漲停,誰在瘋狂買入?

來源:新浪港股

1月12日消息,進入2021年以來,港股開啟上漲模式,一舉突破28000點關口,即使在昨日A美股市集體撲街的情況下,港股恆指依然錄得增長,內資7個交易日瘋狂湧入港股近千億,港股新一波升浪來了嗎?金融三大行業輪動,券商股集體爆發,什麼信號?

南下資金7個交易日湧入近千億,發生了什麼?

今年以來,港股一舉突破28000點,創去年2月以來新高。昨日,A股抱團股殺跌,美股集體收跌,港股依然錄得正增長。

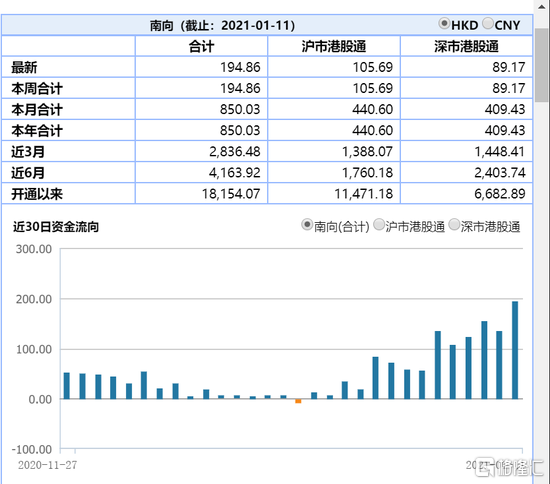

港股暴漲的背後,一方面來自內資連續增持港股。據wind數據,6個交易日全部流入超百億,淨流入總額大約850億港元。昨日淨流入額逼近200億,創歷史新高。截至發稿,南向資金再度流入超100億,7日累計流入950億港元。

近7天數據來看,南下資金加倉中國移動逾200億港元,僅週五加倉就超100億港元,中國聯通、中國電信均超10億,進入前十榜單。此後中國移動也迎來暴漲行情,根據盤後數據,內資成為中國移動,甚至中國聯通、中國電信大漲的根源。

騰訊控股獲得內資買入超200億,此外,中芯國際、中海油、思摩爾、吉利汽車也獲內資買入居前。

港股暴漲的背後,另一方面是因為港股去年跌幅基本處於全球低位,處於估值中樞較低位置。張憶東表示,2020年受地緣政治與海外疫情的影響,港股的風險偏好受到明顯壓制,不僅跑輸A股甚至還跑輸了整個新興市場,AH股的估值溢價高達50%。就是説,在A股和港股同時上市的一家公司,如果其在A股的估值是合理的,那麼在港股就便宜了50%,而這類公司的基本面與香港本地的疫情和地緣政治無關,這明顯是被錯殺了。

中信證券表示,戰略性增配性價比更優的港股。2020年港股在全球主流指數範圍內明顯滯漲,恆指全年漲幅僅為-3.4%。當前恆指動態P/E僅有13.0倍,相比滬深300的16.0倍和標普500的22.9倍明顯偏低,在今年基本面修復的趨勢下(我們預計恆指盈利增速從去年的-6.5%上升至今年的15.1%),有更大配置性價比。密集的反壟斷措施推出對港股互聯網巨頭也產生了情緒上的壓制,帶來估值修正和新的配置機會。

中信表示,此外,未來3年中概股集中迴歸是大概率事件,預計將為港股帶來大量優質標的。近期南下資金也在加速增配港股。本週流入量達到655億港幣,超過歷史單週最高流入水平,目前累計淨買入規模達到15576億元,是2015年6月後成立的主動管理型基金總淨值規模的73.8%。港股建議重點關注互聯網、消費電子、教育、農業、上游原材料和金融板塊的龍頭標的。

券商股漲瘋了,誰在瘋狂買入?

隨着互聯網科技、光伏、新能源汽車開始有所回調,A港股市的金融股迎來輪動機會。昨日內銀股上漲,今日上午保險股上漲,今日下午券商股爆發。在各大粉絲羣,大家都在疑問為何券商股爆發了?中信證券A股直接還漲停了,到底什麼信息我們不知道?

截至目前,港股的券商股中,招商證券、海通國際漲超9%,國泰君安國際、中信證券、中信建投漲超8%,A股的招商證券、中信證券直接漲停。

對於券商股上漲,最簡單的邏輯是,去年A股股民人均賺10萬,從事經紀業務的券商自然成為最大贏家,而券商業績期馬上來臨,佈局券商股存在基本的市場預期。

中期邏輯來看,A股全面註冊制有望到來。去年11月,上交所制定《推動提高滬市上市公司質量三年行動計劃》,將推進科創板建設和註冊制改革,按照部署,推動全面實行股票發行註冊制,從源頭把好上市公司質量關。

中信建投表示,我們建議投資者首要關注頭部券商。首先,在資本市場雙向開放的背景下,證券業併購重組是培育航母級頭部券商、保護國家金融利益的重要手段,頭部券商將在財富管理、股權融資等領域集聚市場資源,從而長期業績成長性佔優;其次,近期增量入市資金以機構資金為主,而機構資金傾向於配置業績穩健、估值不貴的個股,頭部券商估值將得到提振。我們建議長線投資者首要關注東方財富和香港交易所,繼續把握中信證券和華泰證券的投資機會。

根據中信證券港股實時數據,中外資聯合助力中信證券大漲。其中,瑞士信貸買入超100萬股,高盛買入超50萬,內資買入50萬,中金買入17萬,中信證券自己買入超10萬股。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.