中芯國際(00981.HK):淨利潤好於預期,N+1先進製程小量試產,維持“買入”評級,目標價41.97港元

機構:中信證券

評級:買入

目標價:41.97港元

中芯國際為國內第一大、全球第四大晶圓代工廠。我們長期看好公司成熟製程持續擴產做大規模,14nm以下先進製程研發持續推進並取得良好進展,認為公司具備超越國際二線廠商的能力,長期有望躋身國際一線行列,為芯片製造國產替代核心標的。公司收入規模連續兩季度創新高,產能利用率維持高位,維持“買入”評級。

▍2020Q3收入符合預期,收入提升由大客户集中訂貨以及其他業務共同貢獻。公司2020Q3收入10.825億美元(環比+15.3%,同比+32.6%),符合公司近期上調後的指引(環比+14%~16%);收入增長表現較好,一方面是產品組合變化拉動,我們認為H客户在9月15日相關制裁生效前的集中拉貨或是原因之一。H客户產品涵蓋14nm、28nm等較先進製程及8英寸晶圓成熟製程;另一方面,其他業務收入(如光罩製造、晶圓測試、設計服務等)亦表現較好,光罩製造、晶圓測試及其他業務佔總收入比重過去6個季度持續提升,3Q20佔比達14.6%。

▍2020Q3毛利率符合預期,淨利潤好於預期。毛利率24.2%(環比-2.3pcts),符合上調後指引(23%~25%),環比下降主要源於Q3起中芯南方先進工藝新增折舊,此前市場已有預期。在大客户拉貨和8英寸晶圓需求旺盛背景下,3Q20公司產能利用率為97.8%,維持高位運行;ASP達到641.75美元,環比+8%,我們認為在公司產能利用率保持高位、大客户拉貨的情況下,新產品及新訂單代工價格有正常的上浮。歸母淨利潤2.56億美元(環比+85%),好於預期,其中三季度其他經營收入中政府項目資金1.38億美元,二季度為0.41億美元。

▍受針對大客户的貿易政策影響,2020Q4收入下滑已有預期,毛利率指引預計受先進製程折舊影響有所下滑。Q4收入指引環比-10%~-12%,考慮到大客户訂單受貿易政策影響在四季度開始暫停,市場已有預期,指引下滑幅度略好於預期;毛利率港股公告指引為16%~18%,A股公告指引為19%~21%,考慮到中芯南方先進製程折舊影響,基本符合預期。兩地公告差異來自會計準則不同,如存貨跌價港股計入成本,A股計入資產減值損失。全年收入增長預期上修至24%~26%,全年毛利率目標高於去年的20.6%。

▍下修資本開支8億美元,我們認為主要來自出口管制之下海外設備廠商的影響。公司2020年資本開支計劃從67億美元下修到59億美元,主要是由於美國出口管制使部分機台供貨期延長或有不確定性及物流原因致部分機台到貨延遲。10月初美國商務部工業與安全局(BIS)向部分供應商發出信函,對於向中芯國際出口的部分美國設備、配件及原物料須事前申請出口許可證後,才能繼續供貨。中芯國際2020年3月公告曾披露採購自泛林(LAM)、應用材料、東京電子的設備訂單,分別為6億美元、5.4億美元、5.5億美元,採購金額較大。

▍先進製程進展順利,第一代先進製程(14nm)良率達業界量產水準,第二代先進製程(N+1)進入小量試產。芯動科技於2020年10月發佈公眾號文章表示已完成了基於中芯國際FinFETN+1先進工藝的芯片流片和測試。“N+1”是中芯國際對其第二代先進工藝的代號,其與現有的14nm工藝相比,性能提升了20%,功耗降低了57%,邏輯面積縮小了63%,SoC面積減少了55%。N+1與市場所謂的7nm相比,實際上在功耗和規模非常相近,就性能而言略弱。公司定位N+1成為低成本的應用,相比普通7nm減少10%左右成本。N+1的NTO(NewTape-out新流片)在2019Q4、2020年初已經在客户產品驗證階段。按照先前預期,在2020Q4可以看到有限量產(LimitedProduction)。結合公司公告及相關新聞來看,目前正按計劃進度進行。

▍風險因素:市場需求下行;國際環境不確定性;新技術研發、量產低於預期等。

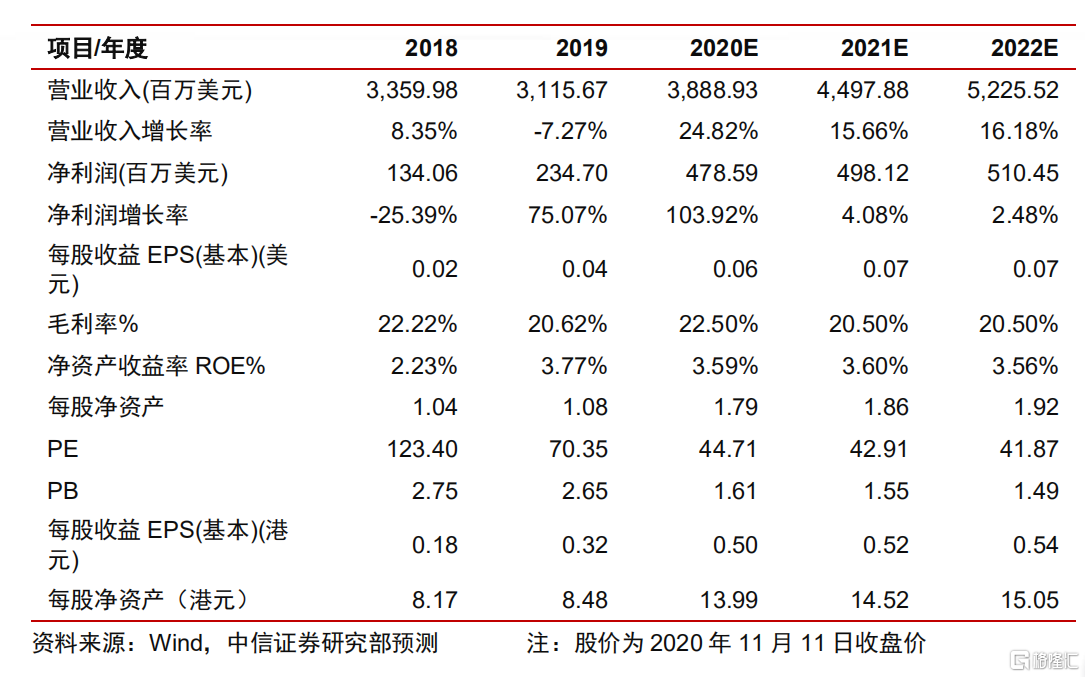

▍盈利預測、估值及評級:我們預計公司將持續受益國產替代、下游景氣,全年趨勢向好,3Q20淨利潤表現超預期,政府項目資金跟隨先進製程研發有望持續發放,因此我們上調公司2020/21/22年淨利潤預測至4.79/4.98/5.10億美元(原預測為2.87/3.19/3.60億美元),對應EPS預測為0.50/0.52/0.54港元(原預測為0.30/0.34/0.38港元),每股淨資產13.99/14.52/15.05港元,按照2020年3倍PB,給予目標價41.97港元,維持“買入”評級。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.