機構:華西證券

評級:增持

事件概述

2020H,公司實現收入 61.81 億元,同比下降 1.2%;歸母淨利潤為 6.83 億元,同比下降 14.1%;扣非歸母淨利潤為 6.83 億元,同比增長 22%,符合預期。扣非歸母淨利增速高於歸母淨利增速主要由於 2019H 聯營公司上海紅雙喜處置土地獲得一次性收益 2.7 億元。2020H,經營現金流量 4.79 億元,同比下降 65%,經營現金流量/淨利為 70%。

分析判斷:

1 、 分渠道看, 2020H 直 營 / 特許經銷商 / 電 商 / 國 際 增 速 分 別 為 -24%/2%/23%/-30% , 佔 比 為22%/50%/27%/1%,直營下降主要由於高線城市受疫情影響更大,而上半年雖然公司對經銷商進行了部分減單,但隨着市場恢復,經銷商收入同比小幅增長;其中,(1)按外延開店和內生同店分拆:直營收入下降中,開店/同店分別下降 0%/24%;經銷收入增長中,開店/單店出貨額分別變動-6%/9%;(2)從整體流水來看,2020H 整體零售流水(在線及線下)10%-20%低段下跌(2019H20%-30%低段增長)。

2、分品牌看,李寧主品牌/YOUNG 開店分別增長-7%/16%至 5,973/1,010 家;

3、分品類看,鞋/服裝/配件和器材分別增長 0%/-4%/15%;

4、分區域看,中國市場/國際市場 98.9%/1.1%,國內北部/南部/華南部增速分別為 1.8%/-1.9%/-7.8%,增速分別下降 22/45/52PCT。

5、分季度看:(1)從流水來看,2020Q2,李寧線下渠道(不包括 YOUNG)零售流水中單位數下降(我們估計 4 月下降 high teens、5 月微幅轉正),其中零售渠道為 10%-20%低段下降、批發渠道為高單位數下降,整體較 Q1 環比提升(Q1 線下整體 20%-30%低段下降,其中零售渠道同比下降 30%-40%中段、批發渠道同比下降 10%-20%高段);電商零售流水獲得 20%-30%高段增長(較 2020Q1 環比增長超 10PCT);(2)從同店來看,2020Q2 零 售/經銷同店分別為 10%-20%高段下降/10%-20%低段下降,環比提升(根據零售/批發增速和店數估算,Q1 零售/經銷同店分別下降約 20-30%中段/10-20%高段);電商同店增速為 20%-30%中段增長(Q1 無符合同店銷售標準的店鋪數據)。

6、分產品看,新品線下零售流水 10%-20%中段下降(其中單價提升低單位數),舊品降幅略好於新品。2020H,毛利率為 49.5%,同比下降 0.2PCT,相較同業來看,在國際品牌大幅打折背景下,公司折扣控制較好;淨利率為 11.1%,同比下降 1.6PCT;扣非淨利率為 11.1%,同比上升 2.1PCT。淨利率提升主要由於費用率下降 2.3PCT(銷售/管理費用率為 31.5%/5.6%,同比下降 0.8PCT/1.6PCT)。

庫存壓力加大,應付賬款週轉天數同比改善,整體現金循環週期縮短。2020H 末,公司存貨為 14.93 億 元,同比增長 12.8%、較年初增長 6%,存貨/收入為 24%,平均存貨週轉天數為 84 天,同比提高 10 天;渠道庫存增長 10%-15%。6 個月售罄率下降超 6PCT,3 個月售罄率下降約 5PCT;受舊品存貨消化放緩影響,存貨減值準備/存貨原值同比提高 2.6PCT 至 11.2%。應收賬款為 7.89 億元,同比增長 4.4%,應收賬款週轉天數為 22天,同比下降 2 天。應付賬款為 13.43 億元,同比增長 10.8%,應付賬款週轉天數為 76 天,同比上升 10 天。平均運營資金總額下降 7%,現金循環週期為 30 天,同比縮短 2 天。

投資建議

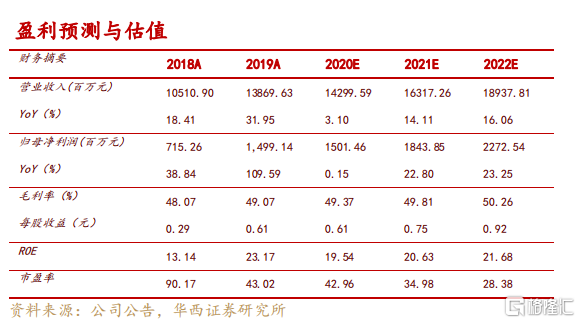

我們認為,公司提前在 2019Q4 進行大幅去庫存,提前釋放了一部分經銷商的庫存風險、上半年經銷商恢復正增長,復甦好於同業。公司未來增長在於:(1)費用率改善、提價和中高端產品佔比提升帶動毛利率提高共同貢獻淨利率提升空間,2020 年目標達到 10-10.5%;(2)線上業務有望維持高增長;(3)線下渠道結構不斷優化,部分直營轉經銷店,從批發到注重終端流水增長,進一步渠道下沉。維持盈利預測不變,20/21/22年EPS 為 0.61/0.75/0.92 元,對應目前 PE 為 43/35/28 倍,維持“增持”評級。

風險提示

時尚運動流行趨勢變化風險、庫存積壓惡化風險、終端折扣加大風險、電商增速放緩、系統性風險。

More Content