閲文集團(00772.HK):中長期邏輯下,閲讀與變現潛力有待重估,首次“買入”評級,目標價54.87港元

機構:西南證券

評級:買入

目標價:54.87港元

投資要點

投資邏輯:短期看閲文戰略調整,佈局免費閲讀;中期看新麗傳媒眾多精品劇後續上線帶來業績提升、對估值的催化,以及在線閲讀用户數的提升;長期看與騰訊關係愈加緊密帶來的更深度渠道支持、對 IP工業化運營的探索。

在騰訊 2020 一季報公開電話會議中,騰訊的管理層對於閲文的規劃包括:1)探索免費閲讀模式,通過免費模式的廣告支持+付費模式,為作家創造更多價值2)通過打擊盜版、多元貨幣化、幫作品獲得更多用户等來提升作品價值,繼續推動閲文集團核心價值的提升。騰訊或能加速閲文對免費閲讀的佈局,以及最大化 IP內容的開發。

內容找讀者、外部獲取用户成本提升,閲文背靠騰訊 10億級用户基數,競爭後期用户獲取優勢凸顯。18/19年,番茄、米讀等免費閲讀 APP 依靠內外部流量短時間內快速獲得了千萬級用户。目前 BBAT 等玩家均已入局、外部流量成本提高,2020年以來,免費閲讀 APP格局、用户數較為穩定,20年 4月,在線閲讀行業廣告投放數量 TOP5 的 APP 75%以上的廣告都投在騰訊廣告平台,文背靠騰訊流量池,在競爭趨緩的背景下,無論是免費還是付費閲讀,用户獲取優勢都更明顯。

免費閲讀為行業帶來新增量(習慣盜版閲讀的用户+無閲讀習慣的用户) ,隨着審美水平的提升,或能向閲文的主陣地-付費閲讀轉化,帶來用户數的提升。1年 6 月,免費平台米讀和七貓與付費平台 QQ 閲讀、掌閲的用户交叉率僅在4.8%-8.0%之間,免費閲讀超 90%的用户是非付費用户。由於免費閲讀內容質量存在短板、付費閲讀價格不貴(付費閲讀 75%的用户月花費在 30 元以下)而閲文是付費閲讀行業龍頭,在頭部作家與作品佔比方面具有壓倒性優勢,免費閲讀培養的正版用户長期來看或會向閲文傾斜。

20年底,影視劇需求端料將旺盛,新麗傳媒精品劇儲備豐富,或能有更高售價。在影視政策和資本寒冬背景下,疊加疫情延遲開工的影響, 2020下半年到 202年,電視劇行業或面臨劇荒。與此同時,快手、西瓜視頻、B 站等入局長視頻頭部內容的爭奪或將捲土重來。新麗作為市場上為數不多精品劇頻出的影視內容公司,曾出品《我的前半生》、《慶餘年》等爆款影視劇,目前已殺青的作品包括大 IP 劇《新鹿鼎記》《新天龍八部》《斗羅大陸》,以及具備爆款品相的都市情感劇《他其實沒有那麼愛你》;20年 5月,拍攝中的劇集包括:大 IP劇《青簪行》《流金歲月》,以及諜戰劇《叛逆者》,籌備中的劇集包括《慶餘年 2》等公司後期影視劇儲備充足,在需求端旺盛的背景下,或能獲得更高議價權。

我國處於 IP 運營體系工業化的探索期,閲文背靠騰訊有望率先出成果:1)I篩選:閲文的訂閲、付費模式能夠快速篩選出好內容;2)理念角度:閲文 201年生態大會上提出的“IP 全鏈服務”的具體操作已經初步可以看出系統化、流程化操作的雛形,閲文集團提出的“IP共營合夥人制度”已處於 IP4.0 的理念以 IP 本身的世界觀為主導,基於同一世界觀的多個內容 IP 進行深入挖掘和多角度的縱橫開發;而行業內的大多數公司仍然處於尋求全產業鏈的高效聯動的IP3.0 理念;3)產業鏈角度:閲文背靠騰訊互娛生態體系,擁有漫影遊資源,打造了 IP全產業鏈孵化的基石;4)IP打造的經驗角度:《斗羅大陸》的紙質書、單行本漫畫、動漫、頁遊、手遊陸續推出,漫影遊同步聯動,目前由公司旗下新麗傳媒出品的《斗羅大陸》電視劇也正在籌備中,達到 IP精品化開發。

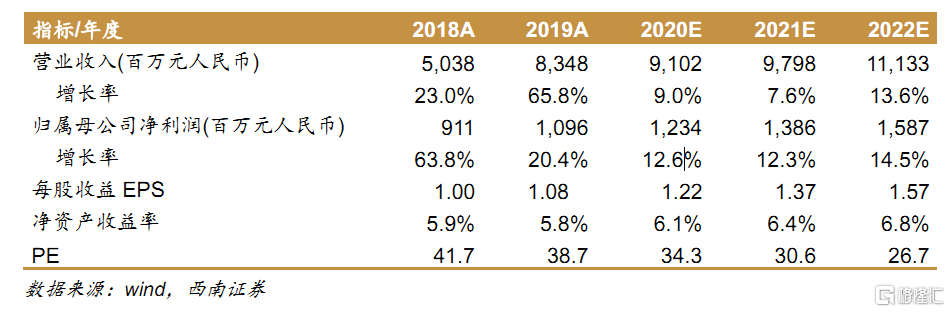

盈利預測與評級:預計公司 2020-2022 年歸母淨利潤分別為 12.3/13.9/15.9 億元,同比增速分別為 13%/12%/15%,對應估值分別為 34/31/27 倍,考慮到:新麗精品劇儲備豐富,免費閲讀競爭趨緩,公司是內容的絕對龍頭,公司 IP 工業化運營有望率先出成果,享受一定估值溢價,首次覆蓋,給予“買入”評級,目標價 54.87港元。

風險提示:在線閲讀新進競爭對手增加投入風險;影視項目進展不及預期風險;網文、影視劇政策趨嚴風險;海外業務拓展風險。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.