欧美平稳恢复,南美成新“震中”——5月25日全球疫情与经济重启高频跟踪

作者:华泰固收

来源:华泰固收强债论坛

摘 要

核心观点

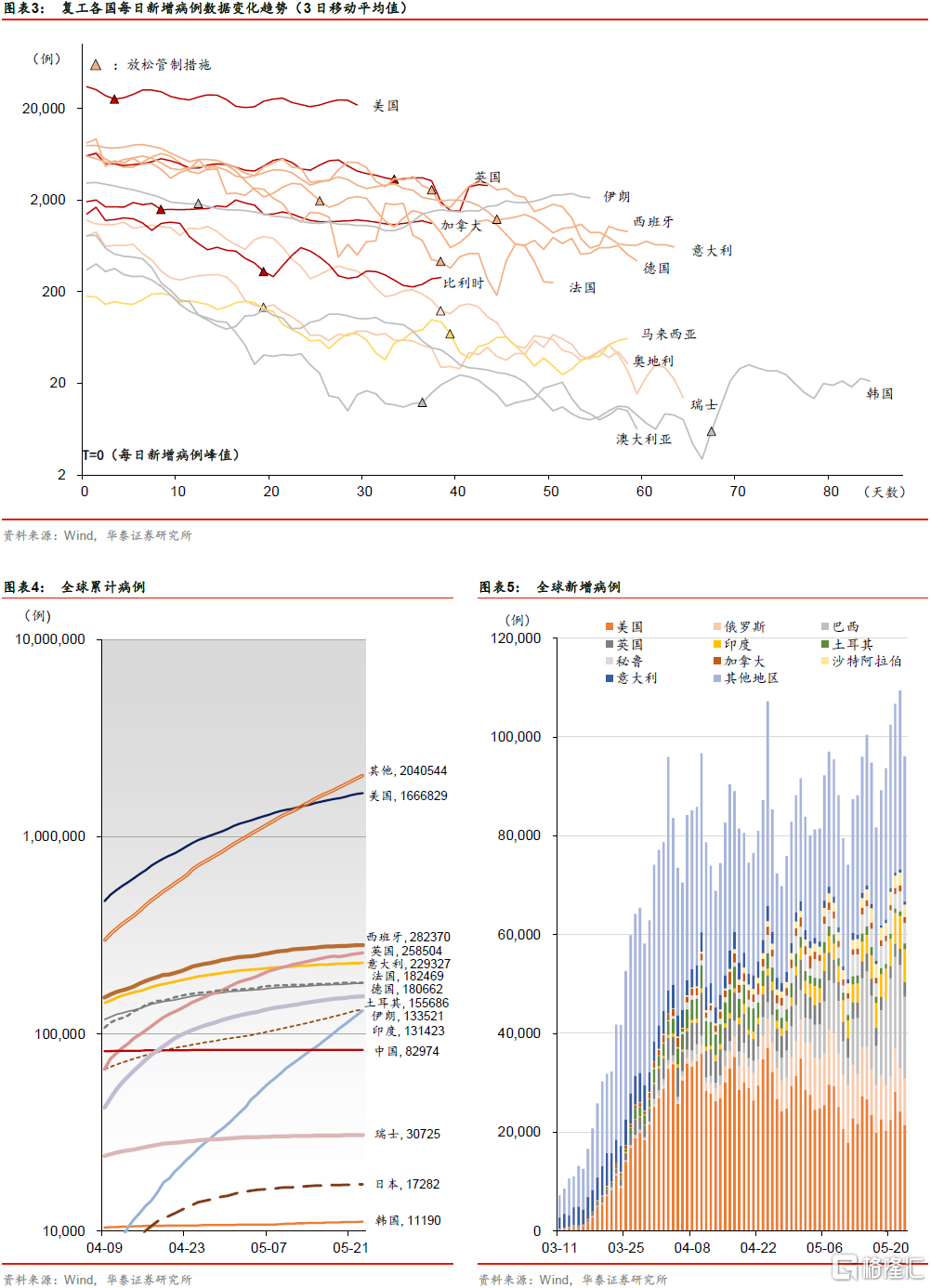

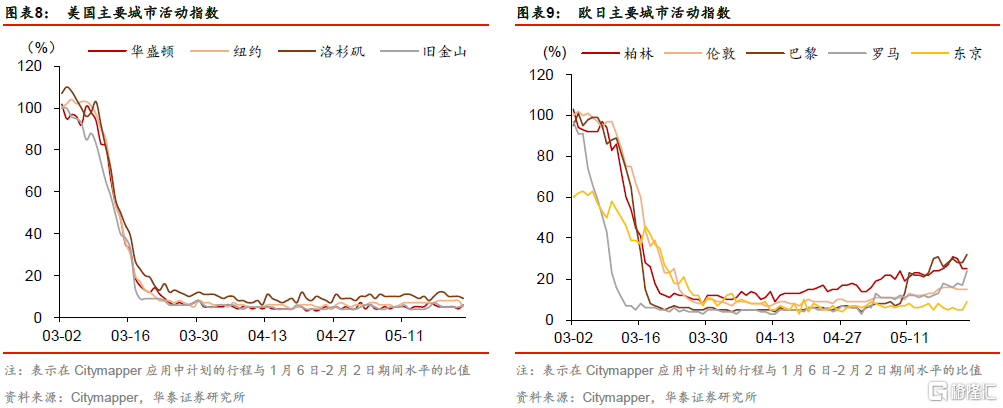

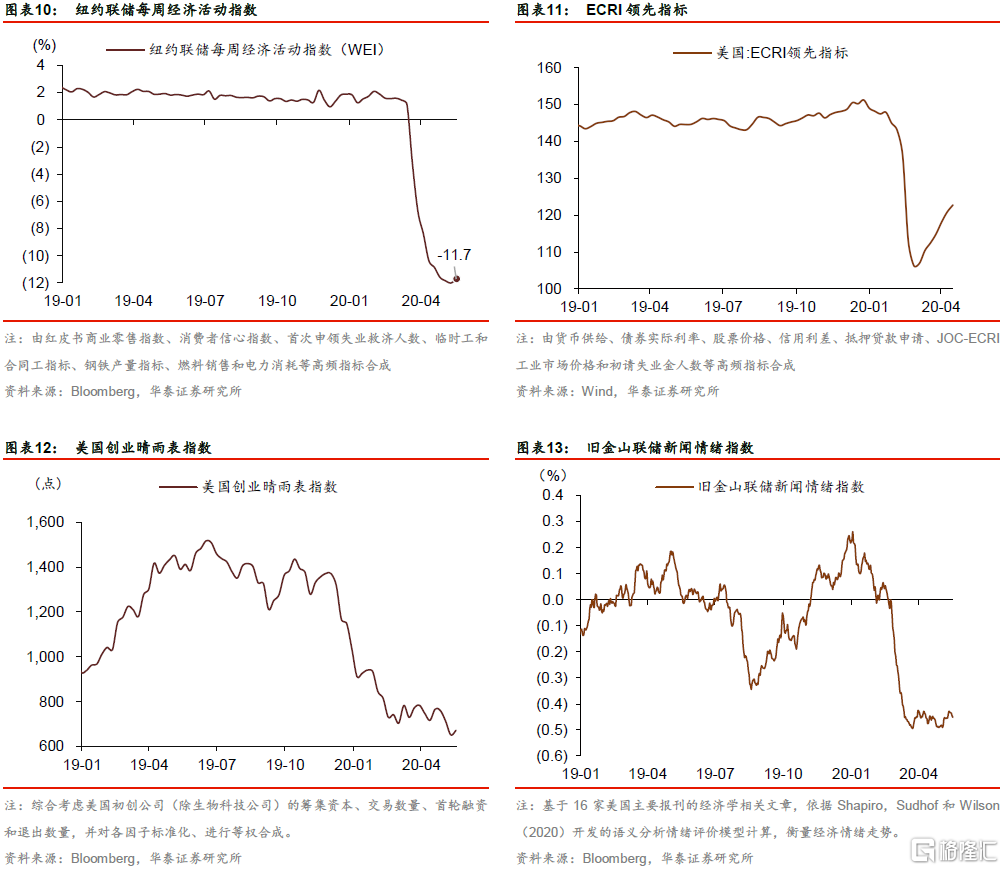

近日发达国家、新兴市场国家恢复状况继续分化。欧洲多国疫情持续趋缓,美国现有确诊重现下降趋势,而新兴市场国家疫情仍在扩散,世卫组织官员表示南美已成为新冠疫情的新“震中”。巴西新增病例升至约2万例/日水平,累计确诊升至全球第二位。在目前情况下,巴西部分城市的商业恢复计划可能带来疫情进一步扩散的风险。从各大主要城市的交通状况看,巴黎、柏林的经济重启进程仍处于领先地位,罗马的恢复速度在加快,美国、日本城市交通状况尚在低位徘徊。5.8-5.15当周美国ECRI领先指标继续回升,反映出经济预期的不断回暖,未来仍需观察实体经济供求状况。

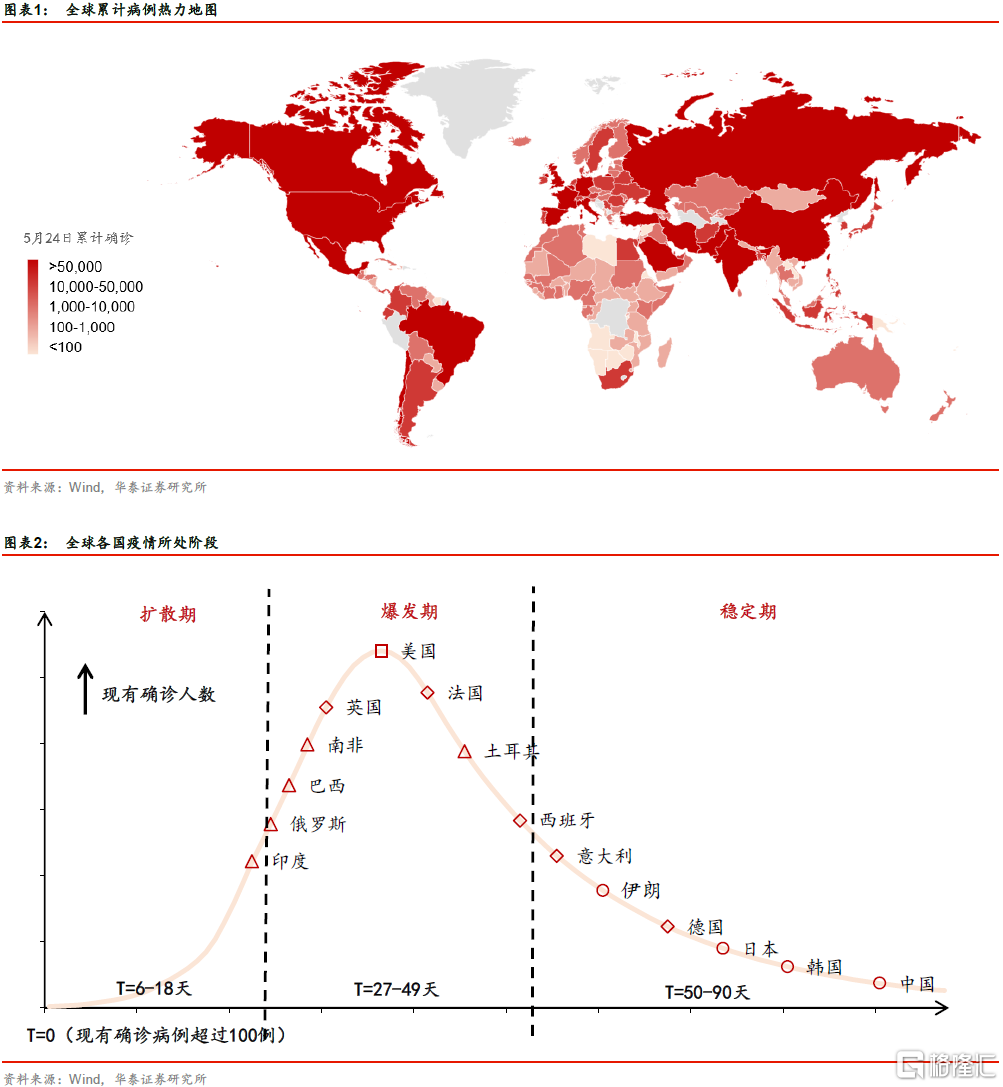

疫情发展:南美成疫情新“震中”,美国现有确诊重现下降趋势

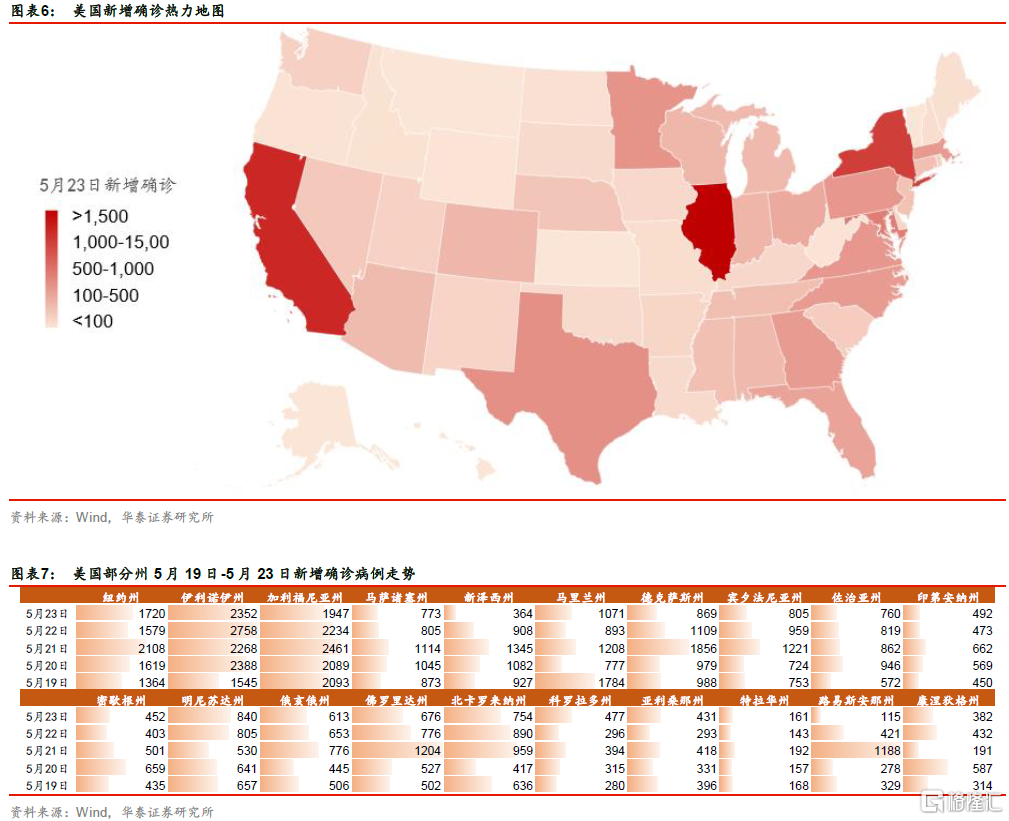

世卫组织卫生紧急项目负责人瑞安表示,南美已成为新冠疫情的新“震中”,巴西是受影响最严重的国家。巴西单日新增病例升至约2万例/日的水平,确诊总数超过俄罗斯成为全球第二位,仅次于美国;即便如此,巴西部分城市仍然计划逐步恢复商业活动。印度连续4天刷新单日最大增幅,非洲累计确诊病例超过10万例。美国现有确诊病例于5月23日再次出现下降,但疫情仍处在平台期。欧洲多国疫情持续趋缓,西班牙全境5月25日起均进入降级第一阶段,英国6月8日起入境人员必须自行隔离14天,法国新冠肺炎疫情总体平稳。日本政府计划于5月25日解除国家紧急状态。

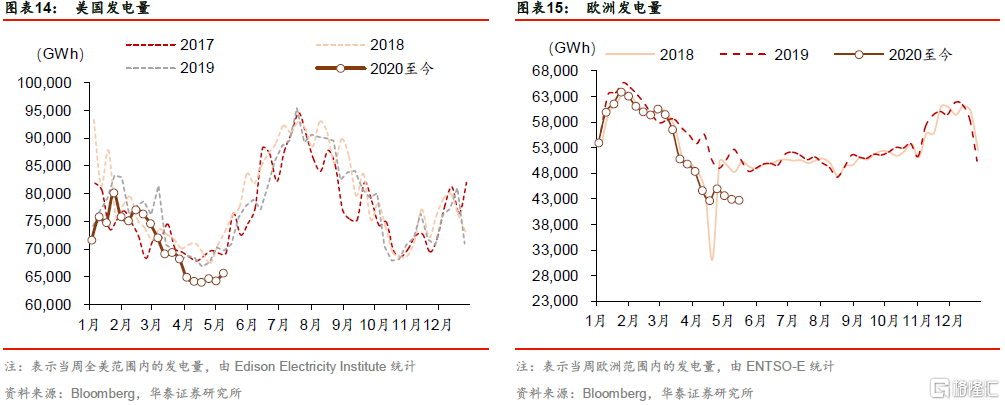

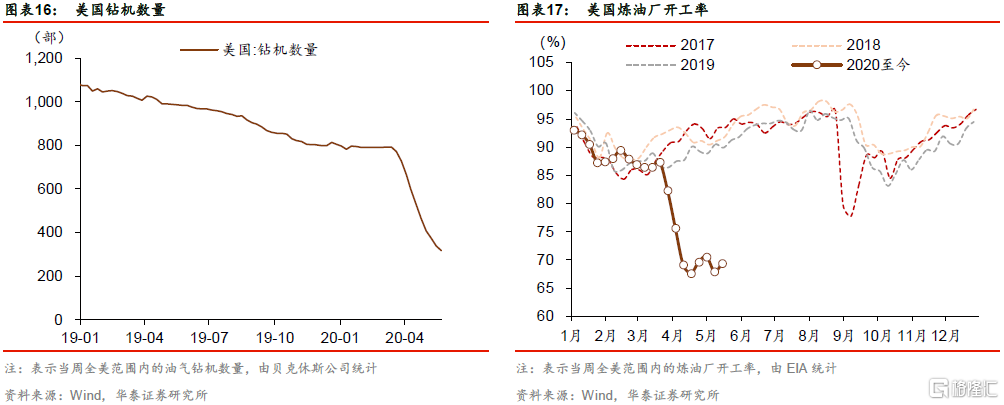

工业生产:能源生产状况低位震荡,需求端回暖有望带动产能恢复

从发电量上看,5.8-5.15当周Edison美国发电量环比回升0.61%,相较去年同期仍存在6.9%的差距。从美国能源企业的生产状况看,5.8-5.15当周EIA公布的炼油厂开工率为69.4%,相比前一周的67.9%回升1.5个百分点,目前仍在低位震荡,相较于往年同期90%左右的水平仍存在较大差距;5.8-5.15当周贝克休斯公司公布的美国油气钻机数量录得318部,相较于前一周进一步减少21部。目前美国所有50个州均已进入重启阶段,能源等工业品需求有望逐步回升,或将带动供给端产能恢复。

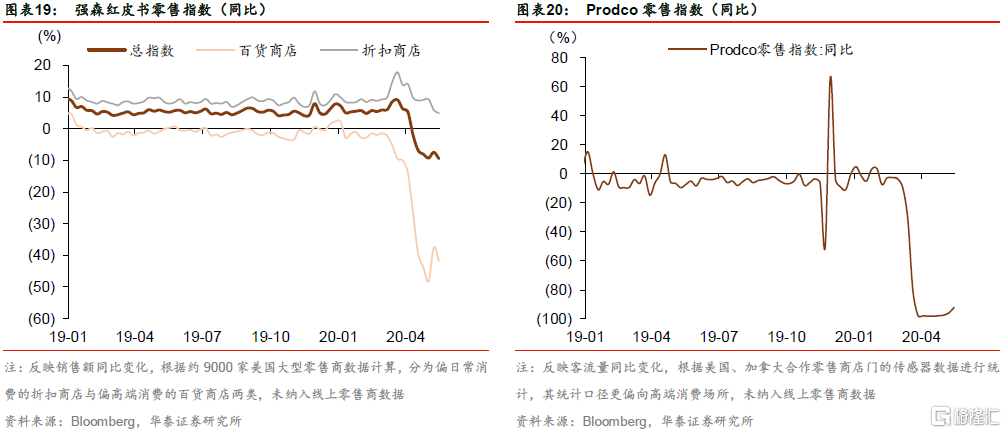

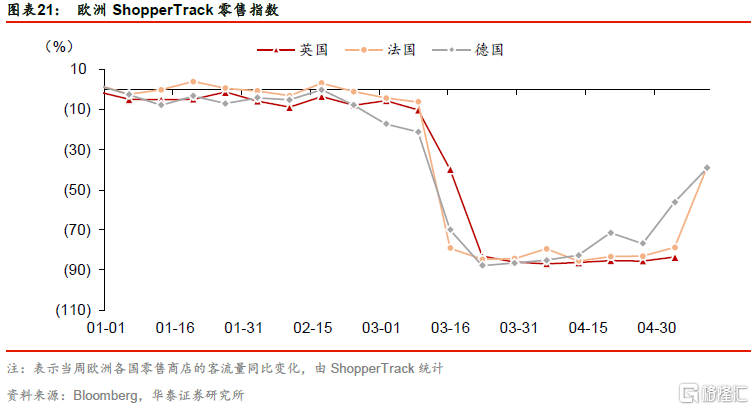

服务业:全球餐饮业持续恢复,德法零售业回暖可期

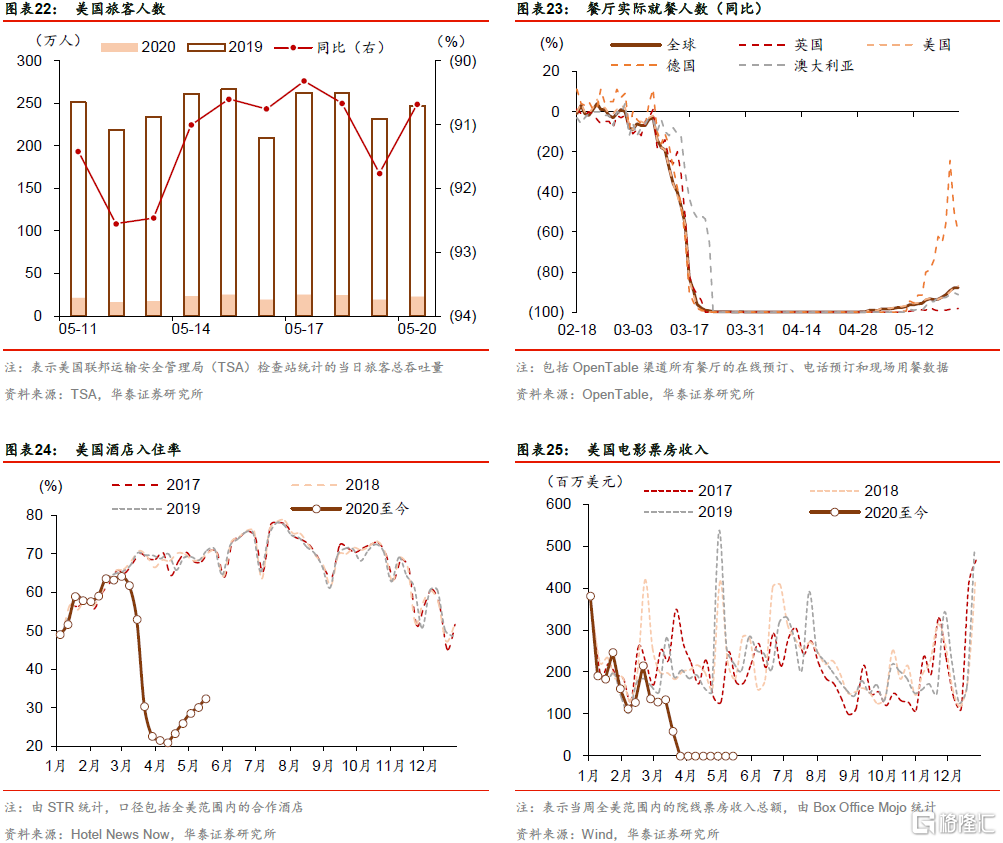

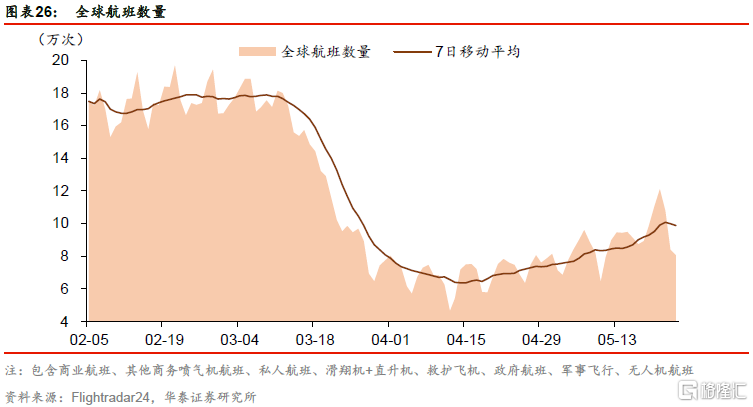

从零售销售方面看,滞后公布的5.4-5.11当周德国、法国ShopperTrack零售店客流量同比均大幅回升至-40%左右,近期乐观的经济重启形势或将带动零售业进一步复苏。从餐饮娱乐方面看,OpenTable统计的各国实际就餐人数同比变化近日出现不同幅度回升。从全球来看,5月23日这一指标录得-87.75%,餐饮活动处于持续恢复阶段,其中德国自5月21日一度回升至-24.40%,继续领跑海外餐饮业恢复进程,英国情况则仍不理想。从航空旅游方面看,全球航班数量仍在稳步回升,5.18-5.24当周平均数量达9.9万次,相较于前一周增加0.9万次。

各国政府动态

美国共和党内部未能对下一阶段刺激达成一致意见,其中最大争议在于对地方政府的资助,部分官员担忧救助金可能用于偿还疫情前的遗留债务。英国政府新增投资2.83亿英镑全面恢复公共交通,首相约翰逊表示确定英国可以进入第二阶段的放松管控,部分学校将按计划于6月1日开放。德国计划用税收政策为社会保险提供支撑。日本政府考虑编纂第二轮追加预算,价值或将超过100亿日元。新兴市场国家方面,俄罗斯政府拨款250亿卢布支持汽车工业。巴西部分城市将逐步恢复商业活动,学校、电影院和剧院仍将保持关闭。阿根廷再次延长居家隔离令至6月7日。

风险提示:全球大规模重启经济导致疫情反复;疫苗研发取得突破性进展。

全球疫情跟踪

美国疫情跟踪

全球主要城市活动情况

综合指标

工业生产

零售销售

餐饮旅游

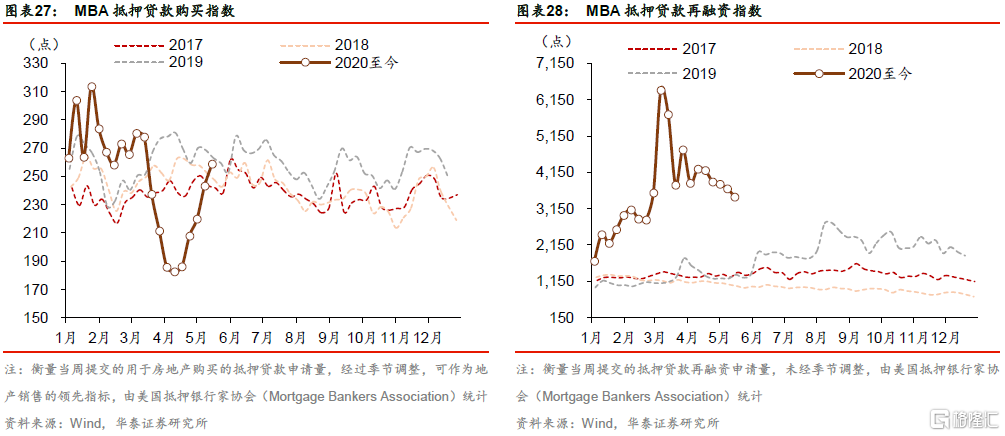

抵押贷款市场

风险提示

1、全球经济重启进程导致疫情反复。政府放松管控本身以疫情反复风险为代价,各国医疗卫生水平、居民自身生活习惯中存在的问题可能再次暴露,从而引致疫情的再次扩散。

2、疫苗研发取得突破性进展。在全球加急开展新冠疫苗的研发的背景下,如果疫苗能够在短时间内研制成功,疫情带来的全球冲击将较快恢复。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.