近期以來,一些上市公司紛紛披露了新年1月份的業績。而數據顯示,截至目前,包括廣發證券(000776.SZ)、海通證券(600837.SH)、國泰君安(601211.SH)在內的17家上市券商已經公佈了2020年1月份的業績數據。此外,一些像華鑫證券、上海證券、花旗證券這樣未上市的券商也同樣公佈了最新的業績。

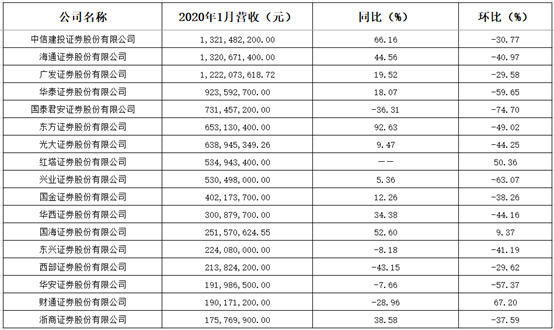

從上述上市券商的營業收入規模來看,2020年1月份,這17家券商的營收(所有以母公司口徑統計為準)全部超過1億元,其中3家券商的營收超過了10億元的規模,6家券商的營收規模處於5億元至10億元區間,其餘的8家券商的營收則處於1億元至5億元區間。

具體而言,中信建投、海通證券、廣發證券分別以13.21億元、13.21億元、12.22億元的營收排在前列,華泰證券、國泰君安、東方證券緊隨其後,營收分別為9.24億元、7.31億元、6.53億元,而浙商證券則以1.76億元的營收排在榜單末尾。

對比數據可以發現,中信建投1月份的營收規模是浙商證券的7.51倍,中小券商的業績和行業頭部券商的業績之間還是有比較大的差距。

(數據來源:同花順iFinD)

從營收的同比增速來看,今年1月,上述券商營收規模同比增長的有11家,其中東方證券1月的營收同比增長92.63%,是這17家上市券商中最高的;營收規模同比下滑的有5家,西部證券以-43.15%的營收增速排在末尾;而紅塔證券因為在2019年7月才上市,1月份營收的同比增速未知。

從營收的環比增速來看,2020年1月份目前僅有財通證券、紅塔證券、國海證券三家上市券商的營收環比增長,分別為67.2%、50.36%、9.37%;其餘14家上市券商的營收環比增速均為負值,其中國泰君安的營收環比下滑74.7%,位居最末。

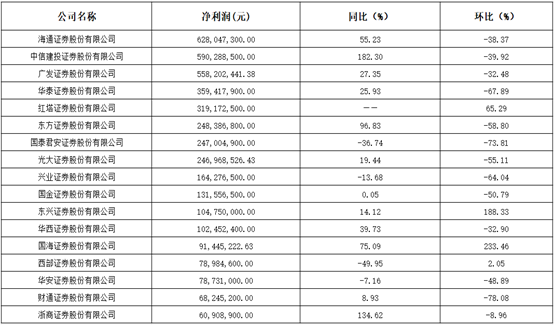

而從上述上市券商1月份的淨利潤(所有以母公司口徑統計為準)規模來看,淨利潤超過5億元的有3家,9家券商的淨利潤在1億元至5億元之間,5家的淨利潤不足1億元。

在這17家上市券商中,海通證券、中信建投、廣發證券1月份的淨利潤分別為6.28億元、5.9億元、5.58億元,排在前列;華泰證券、紅塔證券分別以3.59億元、3.19億元的單月淨利潤緊隨其後;而1月份淨利潤規模最少的則是浙商證券,僅為0.61億元。

同樣的,像海通、廣發這樣的大券商的淨利潤要遠遠超過財通證券這些中小券商。

(數據來源:同花順iFinD)

從淨利潤的同比增速來看,今年1月,上述券商淨利潤同比增長的有12家,其中中信建投1月的淨利潤同比增長182.3%,同比增長最多;淨利潤同比下滑的有4家,西部證券以-49.95%的營收增速排在最後;紅塔證券1月淨利潤的同比增速未知。

而從淨利潤的環比增速來看,2020年1月份目前包括國海證券、東興證券、紅塔證券、西部證券4家單月淨利潤環比增長,其中國海證券、東興證券的淨利潤環比增速分別為233.46%、188.33%;其餘17家上市券商的營收環比增速均為負值,其中國泰君安、財通證券的淨利潤環比下降超過7成。

值得注意的是,從上述營收、淨利潤的數據來看,這17家上市券商披露的2020年1月份的業績相較於2019年12月的業績有較大幅度的下滑。

據悉,之所以會出現上述情況主要是因為上市券商2019年12月的業績亮眼,環比基數較高。

另外,受疫情影響,休市時間延長也在一定程度上影響了券商的業績。

值得一提的是,雖然2020年1月業績環比表現不佳,且疫情仍在繼續,但是一些券商機構對行業依然發表了比較樂觀的看法。

渤海證券發表研報指出,短期來看疫情對資本市場影響的不確定性依然較大,需要關注市場波動影響下信用業務面臨的信用風險。長期來看,如果疫情短期內得不到有效控制還將會對券商線下業務的開展產生一定影響,如投行業務等。但隨着監管層逆週期調控措施的持續加碼,疫情對線下業務的影響也僅侷限於業績兑現節奏上,整體而言影響不大。

該機構研究人員認為,在資本市場深化改革進程中,資本市場改革、流動性以及A股市場上漲帶動的β屬性等券商板塊上漲的驅動因素都將兑現,而龍頭券商在資本市場深化改革“扶優限劣”的政策傾斜下將最直接受益。

天風證券研報表示,疫情對於券商業務開展並無直接影響,且無風險利率預期下移、政策利好有望持續加碼,目前市場交易量環比好轉,風險偏好有所回升,券商板塊估值調整後具備吸引力。

該券商研究人員指出,目前證券行業平均估值為1.9x PB,大型券商估值在1.1-1.7x PB之間,行業歷史估值的中位數為2.4x PB(2012年至今)。未來券商的商業模式轉向“資本化投行”(投行+PE模式),研究投行投資均強且可協同的政策券商才可提升ROE。

More Content