8月15日盤後,陝西煤業(601225.SH)公佈了其2019上半年的業績報告。儘管營收出現了雙位數的增長,銷量亦十分不錯,但陝煤的利潤卻未能同步上行。

中績增收不增利

財報顯示,上半年公司實現營業收入325.86億元,同比增長24.17%;報告期內歸屬於上市公司股東淨利潤58.71億元,同比下降1.23%;陝西煤業的毛利率為43.94%,同比下降10.7個百分點,淨利率為18.02%,同比下降4.6個百分點。上半年實現EPS0.60元。

不過,公司總資產同比再增1.1%,突破至1218.51億元;歸屬於上市公司股東的淨資產月528.44億元,同比曾航4.3%;經營現金流仍保持着高速增長,實現110.34億元,同比增長73.7%。

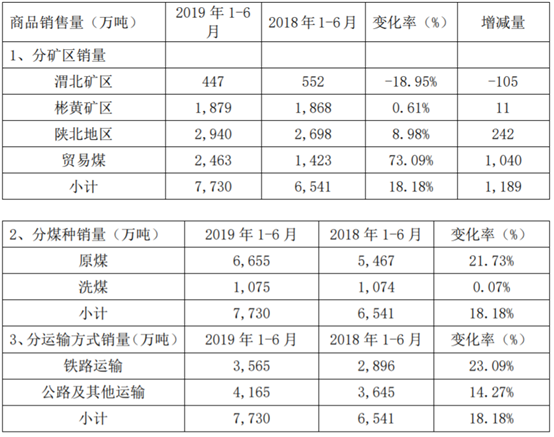

財報顯示,2019年上半年公司煤炭板塊分別實現收入和毛利318.77億元和159.43億元,同比分別增長30.74%和22.17%。煤炭收入增長主要來自貿易煤採購增加帶來的銷量增長以及價格的上漲。

上半年公司煤炭產量為5370萬噸,同比增長1.88%;商品煤銷量7730萬噸,同比增長18.18%,其中貿易煤2360萬噸,同比增長85.83%;煤炭銷售均價412元/噸,同比上漲10.63%;噸煤銷售成本為206元/噸,同比上升18.99%,噸煤毛利為206元/噸,同比上升3.38%。

由於煤炭銷售的量價齊升,公司營收亦實現了顯著增長,這值得慶賀。然而,在營收實現雙位數增長的同事,陝煤不論是淨利率還是毛利率卻有所下滑,這又是為何?

成本高企之痛

根據公司公告,上半年原選煤完全單位成本為206.13元/噸,同比上升32.89元/噸,增幅為18.99%,由此來看,上升的成本主要來自於資源税和復墾基金。

受制於成本顯著提升,上半年公司幾個主產煤煤礦業績均出現不同程度的下滑,其中張家峁實現淨利潤9.1億,同比下降6.19%;紅柳林實現淨利潤10.8億,同比下降15.63%;檸條塔實現淨利潤12.7億,同比下降24.41%。

同時,考慮到小保當一號礦井及選煤廠項目已正式進入聯合試運轉,投運初期煤質尚未達到最佳狀態,因此綜合來看,上半年公司營業成本為182.67億元,同比增長53.59%,拖累公司毛利率表現,上半年毛利率為43.94%,同比下降10.74個百分點。

值得注意的是,上半年陝煤的銷售費用、管理費用、財務費用分別為10.66、25.29、0.77億元,同比增速分別為2.73%、21.52%、10.29%,其中管理費用增長主要來自於小保當的攤銷和小保當、袁大灘的耕地佔用賠償費。總體來看公司期間費用率為11.27%,同比下降0.88個百分點。

目前來看,煤炭行業內,動力煤價格下行趨勢已經確立,焦煤產業鏈需求仍處週期高位,價格風險尚待顯現。經歷供給側改革後行業供應的散亂格局得到根本改觀,在安全、環保的制約下,煤炭週期的底部要顯著高於前幾輪週期;行業進入存量市場階段,企業的縱向整合和橫向整可能帶來價值及估值體系的變化。

險資新進入股

財報顯示,截至2019年上半年,根據公司公佈的前十名股東持股情況可發現,華夏人壽保險股份有限公司累計持有公司3.2億股,佔公司總股本的3.2%,其中Q2單季累計買入2.4億股,佔公司總股本的2.4%,位列公司第七大股東。

事實上,陝西煤業的股價自年初至今累漲超25%,年內高點達到9.76元后有所回落,目前在9元附近橫盤波動。

另一方面,蒙華、靖神開通在即,助力公司打破運輸瓶頸。榆神四期作為十四五重點規劃項目,儲量達到421億噸,開採條件較為優越。陝煤集團作為主要開發主體,有望建設若干千萬噸級大型礦井。未來伴隨蒙華鐵路的開通及煤炭資源的進一步集中化,陝煤集團及公司有望複製重慶模式,藉此打開湖南湖北江西的煤炭市場,由此未來業績依然有望得到釋放。

券商怎麼看?

廣發證券認為,陝西煤業資源稟賦好, 成長性突出。 一方面,隨着小保當一期、袁大灘煤礦、小保當二期投產,公司產量有望逐年提升。另一方面,公司銷售結構有望逐步優化, 蒙華鐵路預計 2019年四季度投入運行,公司中長期將受益於鐵路運力改善帶來的量價提升。看好公司盈利的成長性和可持續性,參考歷史估值給予公司 19年 PE 估值 9.5倍,對應合理價值 11.06元/股, 維持“買入”評級。

國盛證券認為,公司在資源稟賦、產業佈局及股東背景方面均明顯強於行業平均水平,考慮到公司優異的資源稟賦,出眾的成本管控能力,確定性的增量,高而穩定的分紅比例,以及未來蒙華鐵路開通後長協佔比的進一步提升,公司業績有望迭創新高,維持“增持”評級。

More Content