【方正宏观】如何理解CPI、PPI的冰火两重天?

作者:王丹、陶川

来源:川阅全球宏观

2019年9月份,CPI同比3.0%,前值2.8%,市场预期2.8%;PPI同比-1.2%,前值-0.8%,市场预期-1.3%;

核心观点

9月CPI同比扩大至3.0%、PPI同比则降至-1.2%,二者分化加剧,本质是当前经济供给冲击和需求收缩均有所加剧。9月猪价同比涨幅接近70%并带动一系列肉类消费品价格普涨,当前能繁母猪存栏和生猪存栏仍未见底,猪瘟疫情带来的供给冲击将持续至明年下半年。而CPI服务项持续回落、PPI生产资料项通缩加剧,则显示了需求收缩的影响。展望后市,猪肉供给冲击将支撑CPI进一步上行,尤其是1月份叠加春节错位因素CPI大概率破“4”;CPI向PPI传导、逆周期政策发力,以及供改带来的产能利用率保持韧性,当前PPI处于磨底的过程中。

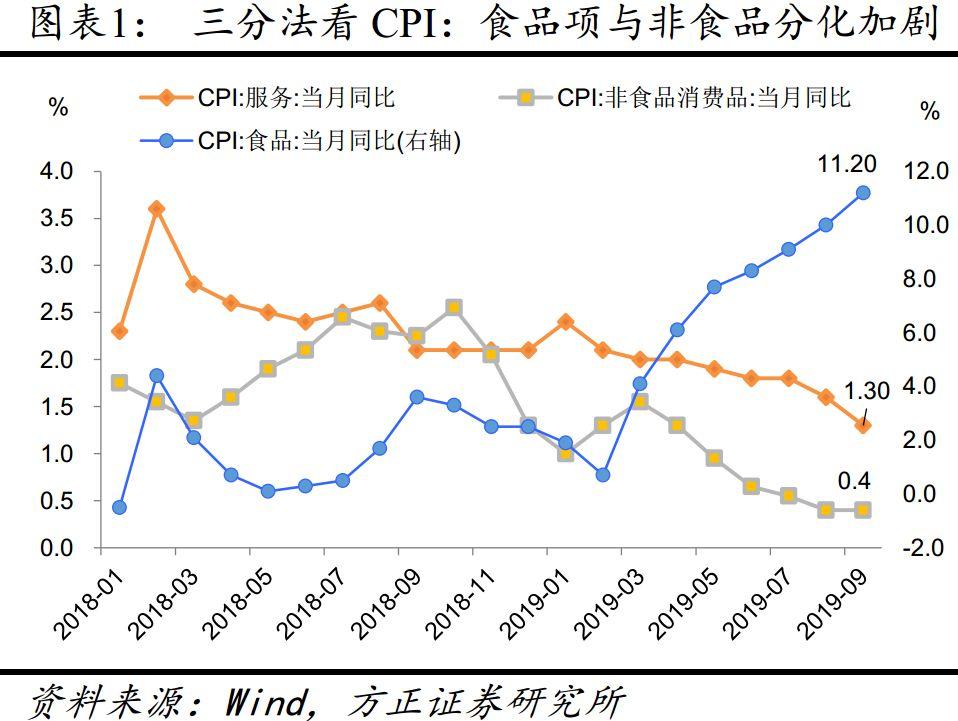

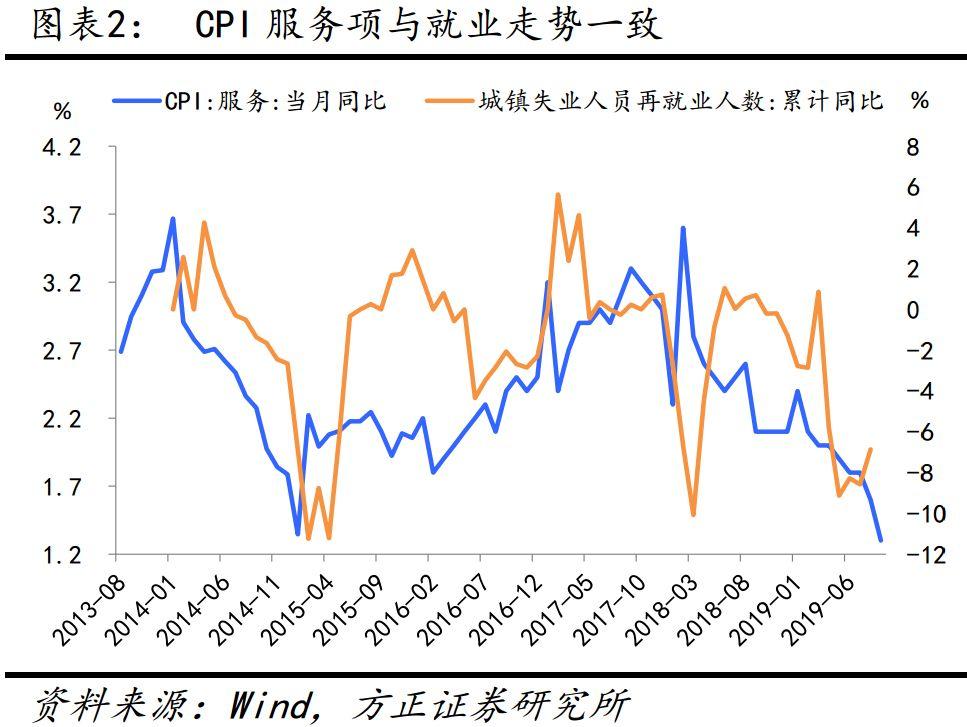

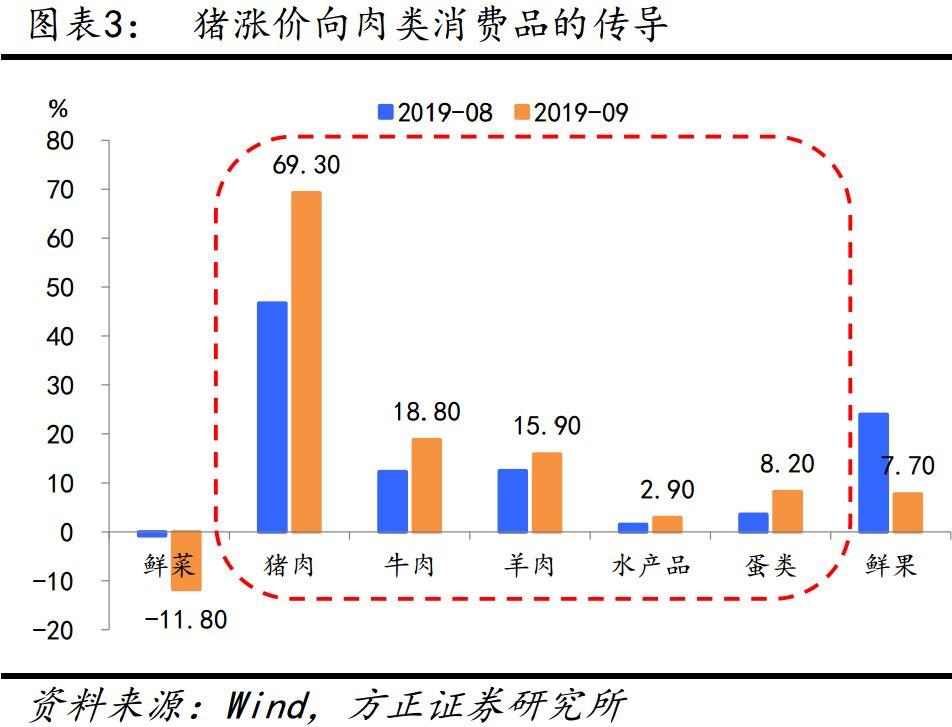

猪涨价向肉类消费品传导,CPI触“3”。9月CPI同比涨幅扩大至3.0%,高于市场2.8%的一致预期。三因素拆分法来看,食品与非食品项的分化继续加剧,食品项同比扩大至11.2%,较前值回升1.2个百分点;服务项则连续两个月走弱,同比降至1.3%(图表1),服务项的回落显示当前经济下行、尤其是稳就业压力有所加大(图表2)。食品分项来看,猪肉同比上涨69.3%,较前值扩大22.6个百分点,并带动牛肉、羊肉、水产品等肉类消费品大涨(图表3)。

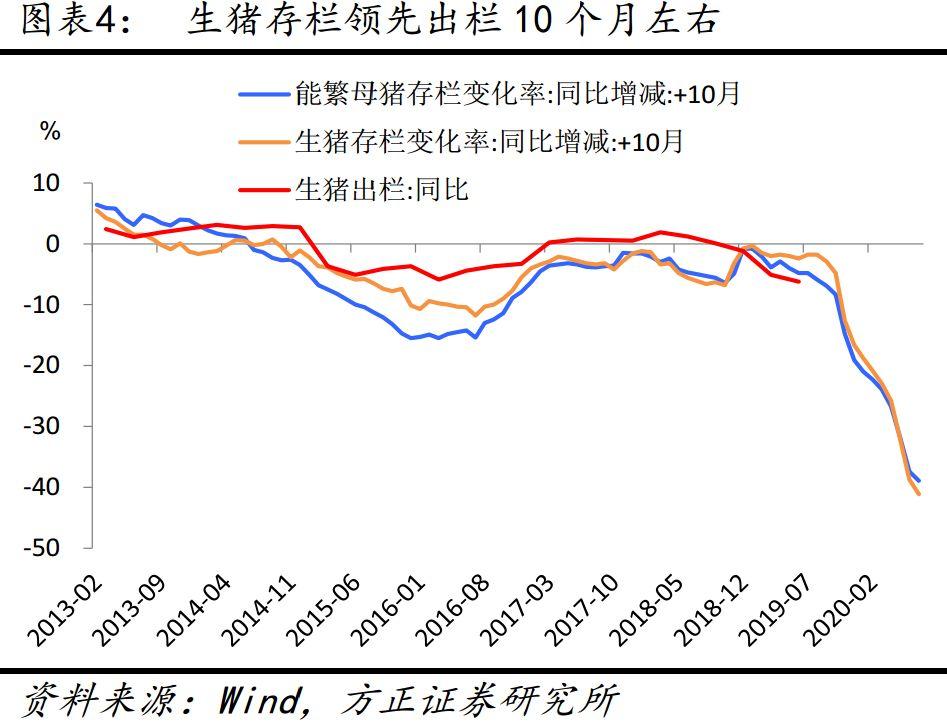

猪周期将支撑1月份通胀破“4”。分析2007年、2010年和2015年三轮猪周期表现,猪肉涨价持续冲击在2年左右;同时,从生猪存栏领先出栏大概10个月左右的角度来看,当前生猪存栏和能繁母猪存栏的同比变化尚未见底,因此猪周期形成的通胀压力至少会持续至明年下半年(图表4)。尤其是1月份叠加春节错位的影响,CPI大概率将突破“4”。

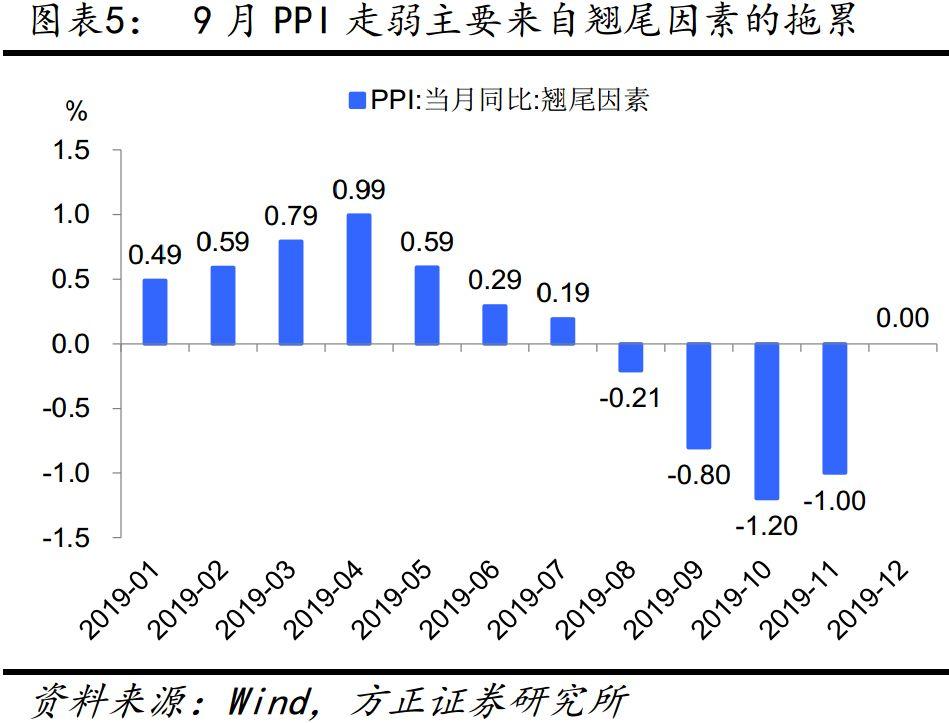

翘尾因素拖累PPI继续下探,CPI涨价向PPI传导。9月PPI同比下降1.2%,较前值继续回落0.4个百分点,创下2016年7月以来新低。但结构拆分来看,9月PPI的下滑主要来自翘尾因素的拖累(图表5),9月PPI环比回升0.1个百分点,重回正增长。分结构来看,生产资料同比下降2.0%,降幅较前值扩大0.7个百分点,连续4个月处于通缩;生活资料同比较前值回升0.4个百分点至1.1%,生活资料的回升主要来自CPI涨价的传导,食品项同比上涨3.3%,较前值回升0.7个百分点(图表6)。

当前PPI处于磨底的过程中。展望后市,中性假设下国际油价缺乏大幅涨价的需求支撑;地产链条前端景气度明显回落(拿地领先新开工9个月左右),地产链条后端(3年前期房销售形成竣工和交付需求)修复还受到地产融资收紧的抑制;隐性债务约束叠加预算内财政前倾,基建需求回升较为乏力。整体来看,内需未见明显向上对冲动能,而翘尾因素拖累将拖累10月PPI继续下探,预计年内PPI大概率将继续在负区间内运行。同时,CPI向PPI传导(图表7)、逆周期政策边际加力,以及供改带来的产能利用率保持韧性,当前PPI处于磨底的过程中。

风险提示:猪瘟疫情恶化;原油供给形势变化;环保政策变化

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.