中国财险(2328.HK):市场竞争力持续增强,分红率有望进一步提高,维持“买入”评级

机构:中泰证券

评级:买入

投资要点

事件:中国财险公布2019年中报,上半年总保费同比增长15.1%至2360.4亿元,综合成本率上行1.5ppts至97.6%,年化总投资收益率提高0.1ppts至5.3%,上半年净利润同比增长39.1%至168亿元,净资产较年初增长12.4%至1590亿元,数据表现良好。

人保财险上半年经营亮点:市场竞争力增加,经营管控效果显著。

1、人保财险通过“警保联动”,“主干道巡视”,“农网协同”等保险+服务+科技的模式创新,拉动增量保费同比提升20%,车险续保率在部分地区业务暂停的情况下提升0.1ppts至66.6%。市场份额较去年末提升1.1ppts至35.1%,在四家中心城市市场份额重返第一,多家中心城市市场份额上升,市场竞争力进一步提升;

2、人保财险上半年持续提升业务质量和理赔管控能力,通过稽查,科技,进项增值税抵扣和驾安配平台减少了123亿理赔漏损,叠加费用支出的减少,使得人保财险上半年经营现金净流入87.3亿元,大幅扭转过去2年的净流出情况,有助于防范流动性风险和提高可投资资产规模增速;

3、上半年在车险行业增速放缓的背景下,人保财险非车险业务实现高速增长,占总保费的比重较去年同期增加5.7ppts至46%,且除了政策性的大病医疗险之外均实现承保盈利;

4、上半年销售渠道去中介化卓有成效,车险直销指控业务增速12%,占比较去年同期提升4.8ppts至68.3%,有助于降低销售费用,增加客户粘性。

综合费用率下降速度略慢主因已赚保费形成率和增加增值服务投入,猪瘟和台风赔付风险可控。

1、人保财险2019年上半年综合费用率下降1.pppts至32.9%,下降幅度小于手续费率支出的降幅,主要原因是上半年已赚保费形成率较去年同期下降6ppts至76.3%,同时公司加大了直销直控,警保联动和客户维护等增值服务费用;

2.人保财险猪瘟已经赔付支出2800万元,利奇马台风报损35亿元,预计实际赔付25亿元以下,风险可控;

下半年展望:股息率有望进一步提升,是当前利率环境下的较优选择。我们认为中国财险下半年有较好的投资机会:

1)车险报行合一监管继续升级,有利于手续费率保持低位;

2)三次商车费改和报行合一折扣率因素造成的车均保费下降效应进入尾声;

3)已赚保费形成率逐渐提高,全年综合成本率有望下行;

4)2018年12月公司没有参与联营企业华夏银行的定增,视同股权处置有7.4亿元的投资损失,我们看好公司全年的净利润增速;

5)人保集团明确将在今年15.7%的分红率上有所提升,人保财险作为集团分红的最大贡献者,分红率有望在当前39%的基础上进一步提高;

6)财险没有资产负债久期却口,在当前利率下行的环境下受影响程度小;

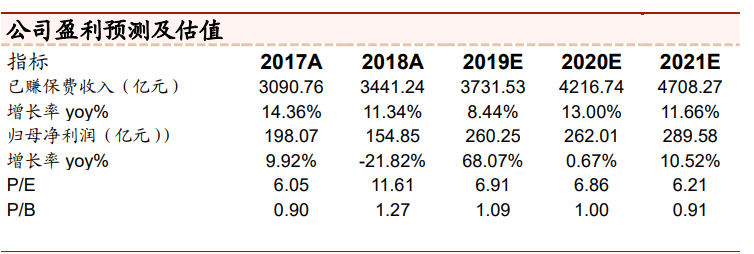

投资建议:我们预计中国财险2019年扣非净利润为218亿元,同比增长40.7%,净资产同比增加17%,roe回升至16.7%,当前股价对应19年pe和pb为6.9倍和1.1倍,维持买入评级。

风险提示:车险手续费率监管放松,下半年出现巨额巨灾风险,权益市场大幅下滑。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.