本文來自格隆匯專欄:中金研究,作者: 黃亞東 段玉柱等

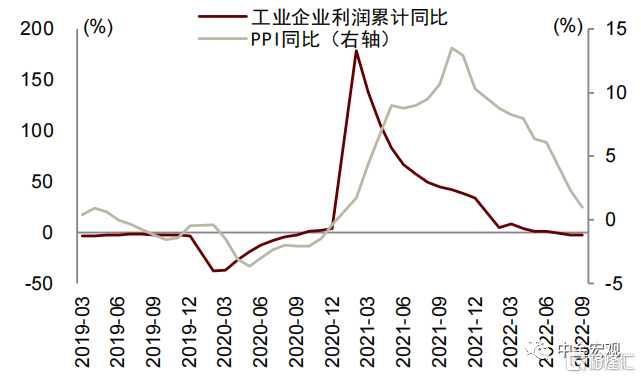

2022年1-9月全國規模以上工業企業利潤累計同比下滑2.3%,較2022年1-8月下降0.2ppt。單月來看,我們推算2022年9月利潤同比增速為-3.8%,比8月上升5.4個百分點。受低基數的影響,工業增加值增速上升,帶動9月利潤增速回升。工業企業利潤結構改善,中游製造業利潤佔比上升。展望未來,我們認為,短期內出口增速下降,房地產投資恢復緩慢,工業企業利潤仍有面臨壓力。

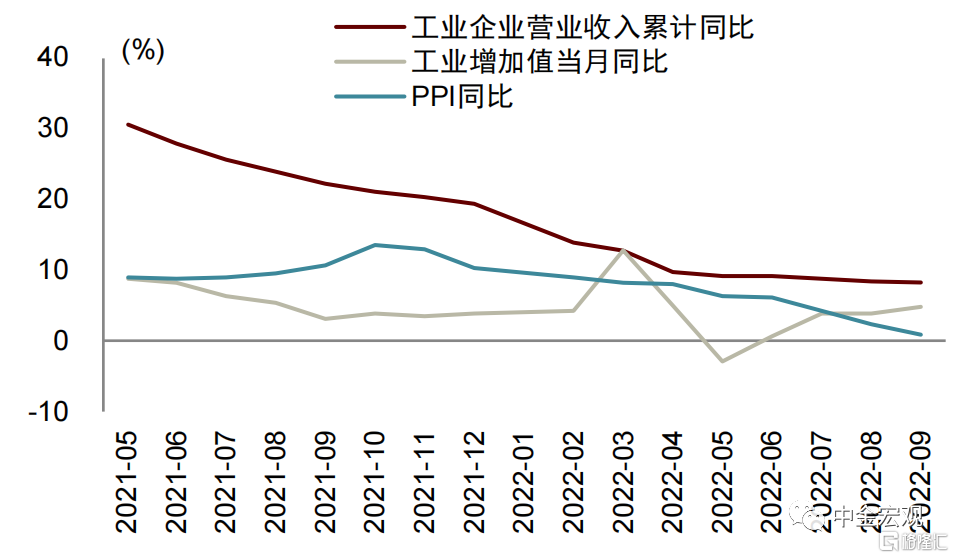

工業企業收入累計小幅下跌。在量的方面,2022年9月工業增加值同比增長6.3%,較8月上升2.1ppt。由於2021年9月限電限產造成了工業增加值同比增速的低基數,2022年9月工業增加值同比增速有較大的提升。在價的方面,2022年9月PPI同比增速為0.95%,相比8月下降1.35ppt,自2021年10月以來PPI持續回落。海外加息效果繼續發酵,海外經濟衰退概率增加,大宗商品價格近期下降,帶動PPI繼續回落。布倫特原油結算價從9月1日的92.36美元/桶下降至9月30日的87.96美元/桶。我們推算9月工業企業營業收入單月同比增速為6.8%,比8月上升1個百分點,主要是工業增加值增速上升的影響。由於9月單月增速仍較1-8月累計增速低,所以2022年1-9月工業企業營業收入累計同比增長8.2%,較1-8月的增速下降0.2ppt。

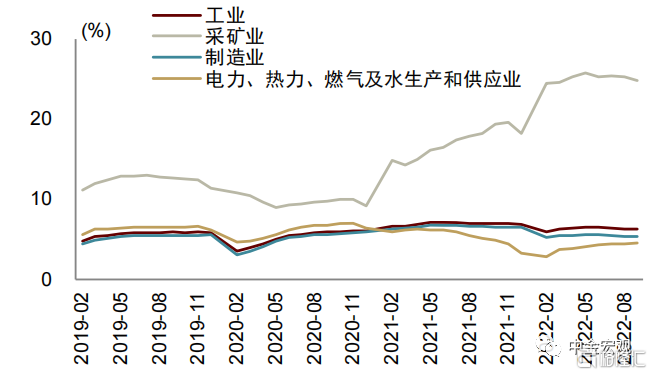

營業利潤率小幅下降。由於PPI下降,帶動了上游行業的利潤率下降。2022年1-9月工業企業整體利潤率為6.23%,比1-8月下降0.06ppt。其中,採礦業1-9月利潤率為24.81%,較1-8月下降0.42ppt;製造業1-9月利潤率為5.32%,較1-8月下降0.03ppt;電力、熱力、燃氣及水生產和供應業1-9月利潤率4.53%,較1-8月上升0.09ppt。

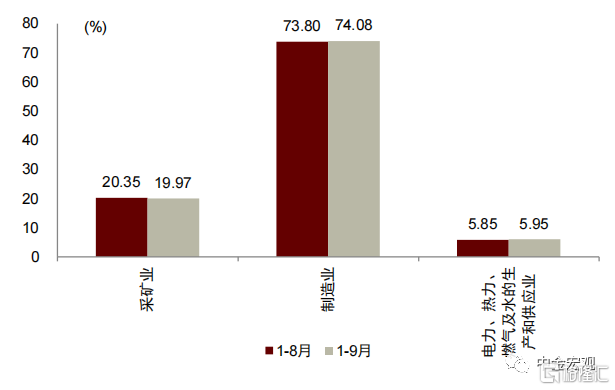

工業企業利潤結構有所改善。由於PPI下降,上游行業利潤佔比下降。2022年1-9月,採礦業利潤在工業企業利潤中佔比為19.97%,較1-8月下降0.38ppt;製造業利潤佔比為74.08%,較1-8月上升0.28ppt;電力、熱力、燃氣及水生產和供應業的利潤佔比為5.95%,佔比上升0.1ppt。

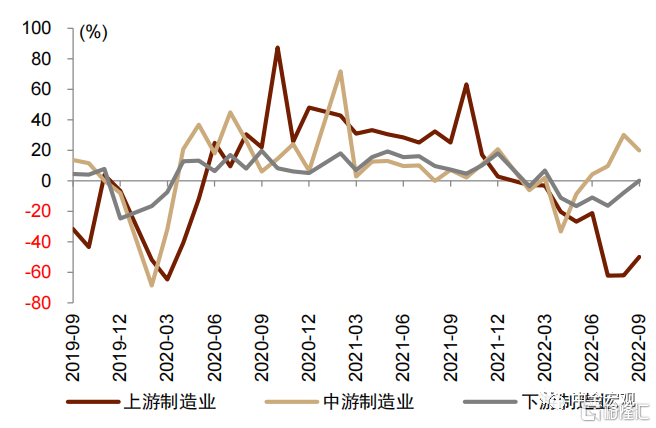

由於PPI和CPI剪刀差繼續收窄,利潤重心繼續向下遊移動。2022年9月,PPI與CPI剪刀差為-1.9%,較8月下降1.7個百分點。我們構造的利潤分化指數從8月的86.9下降至9月的83.9,表明下游行業利潤佔比上升。

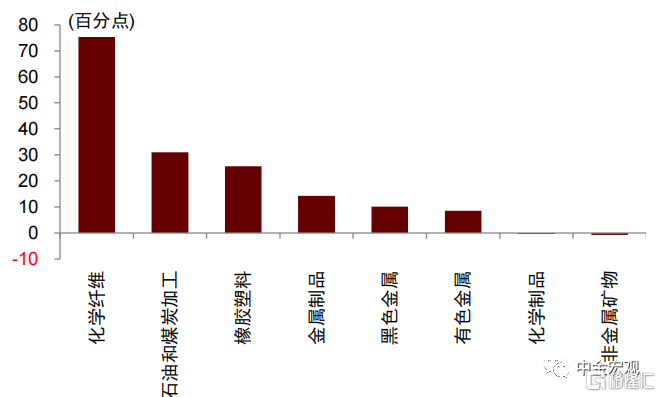

細分行業看,能源價格下跌支撐原材料製造業和電力行業利潤改善,工業利潤分化程度有所收斂。9月,採礦業利潤增速下滑3.5個百分點至10.6%,主要是煤炭價格下跌拖累利潤下行。對應地,製造業、公用事業利潤均有改善,尤其是受能源價格影響較大的上游原材料製造業、電力熱力的生產和供應業,利潤增速分別改善12.2和526.6個百分點。其中,化學纖維、石油和煤炭加工、橡膠和塑料製品等行業利潤增速改善20個百分點以上。伴隨外需下行和汽車刺激效果減弱,中游設備製造業利潤增速有所回落,不過依然保持了19.8%的高位增長,其中電氣機械及器材、汽車、運輸設備等利潤增速保持在30%以上。

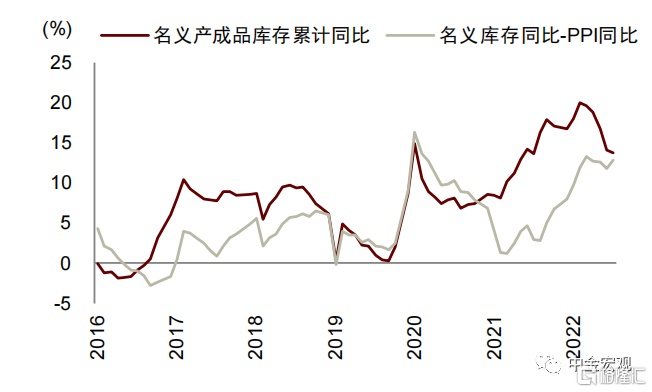

工業企業實際庫存還有繼續回落的空間。2022年9月末產成品名義庫存同比增加13.8%,較8月末下降0.3ppt。排除掉價格因素後,2022年9月末產成品實際庫存同比增加12.9%,較8月末上升0.9ppt。雖然工業企業產成品實際庫存在9月有所上升,但仍然處於歷史相對比較高的位置,高於2010年以來工業企業產成品實際庫存同比增速的均值(8.35%)。PMI數據中9月製造業產成品庫存指數為47.3,仍然處於收縮區間。因此,向前看企業庫存還有繼續回落的空間。

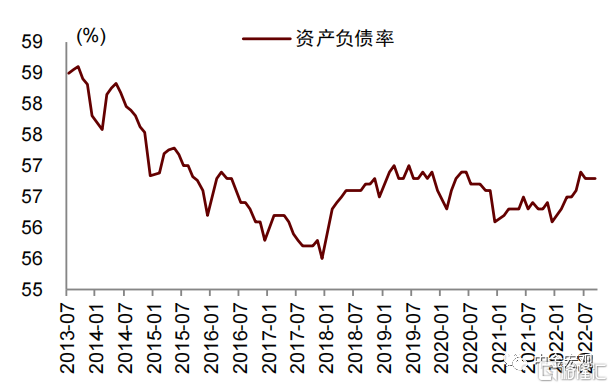

資產負債率保持平穩。2022年9月末工業企業整體資產負債率56.8%,同比上升0.5ppt,環比持平。目前,工業企業的資產負債率仍然處於歷史相對較低水平,低於2010年以來的均值(57.25%)。

圖表1:工企營業收入、工業增加值與 PPI 同比

資料來源:iFinD,中金公司研究部

圖表2:工企利潤與 PPI 同比

資料來源:iFinD,中金公司研究部

圖表3:累計營業利潤率

資料來源:iFinD,中金公司研究部

圖表4:工業企業利潤佔比

資料來源:iFinD,中金公司研究部

圖表5:9月,工業利潤分化程度有所收斂

資料來源:Wind,中金公司研究部

圖表6:9月,化學纖維、石油和煤炭加工等能源依賴型行業利潤增速改善較大

資料來源:Wind,中金公司研究部

圖表7:實際產成品庫存上升

資料來源:iFinD,中金公司研究部

圖表8:資產負債率

資料來源:iFinD,中金公司研究部

More Content