本文來自格隆匯專欄作家:開源證券趙偉

報告要點

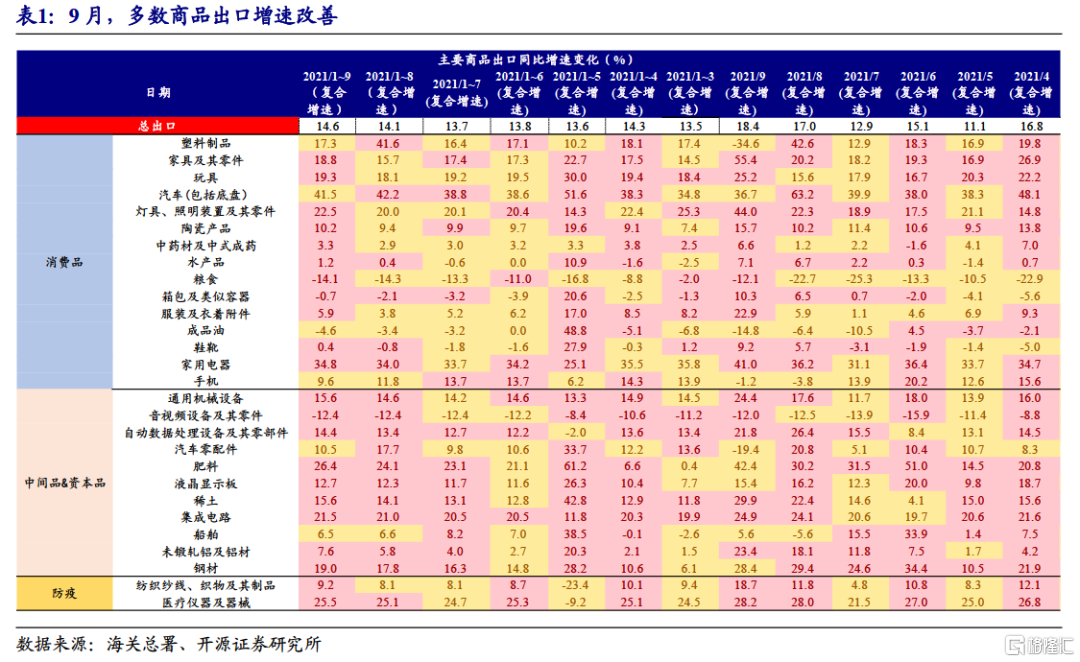

9月出口增速回升,多數商品出口改善

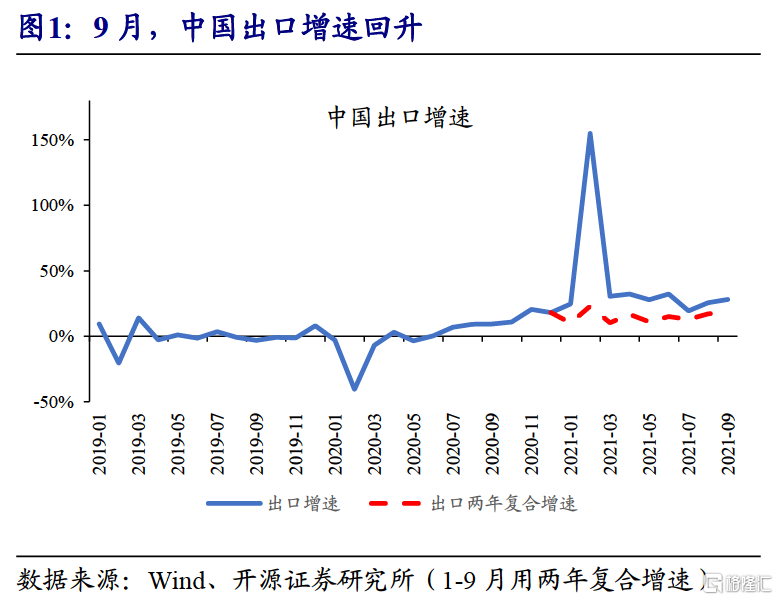

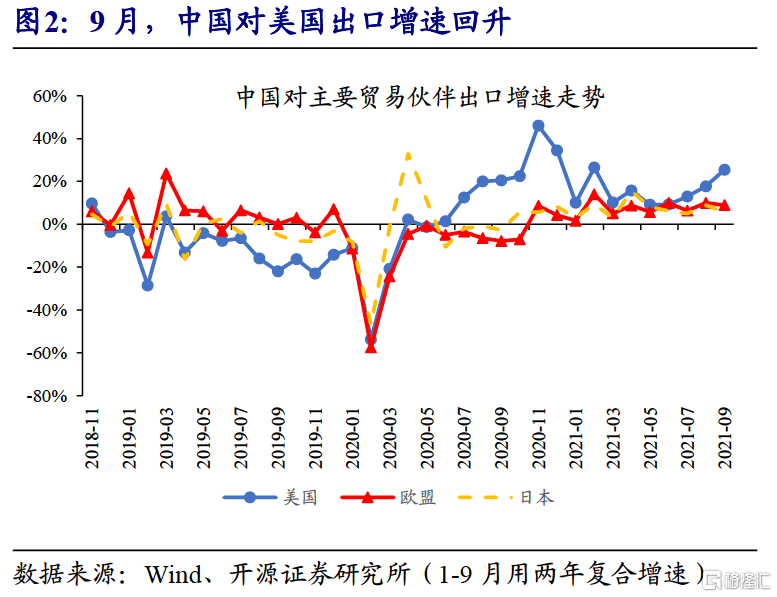

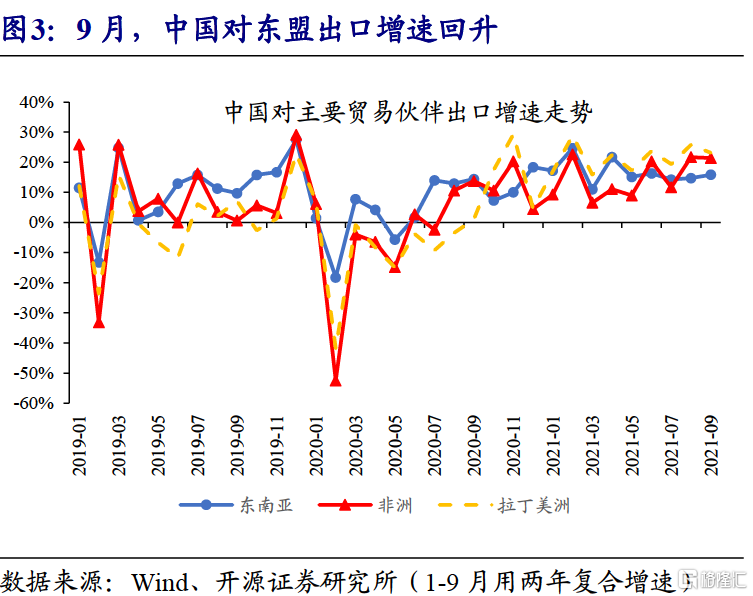

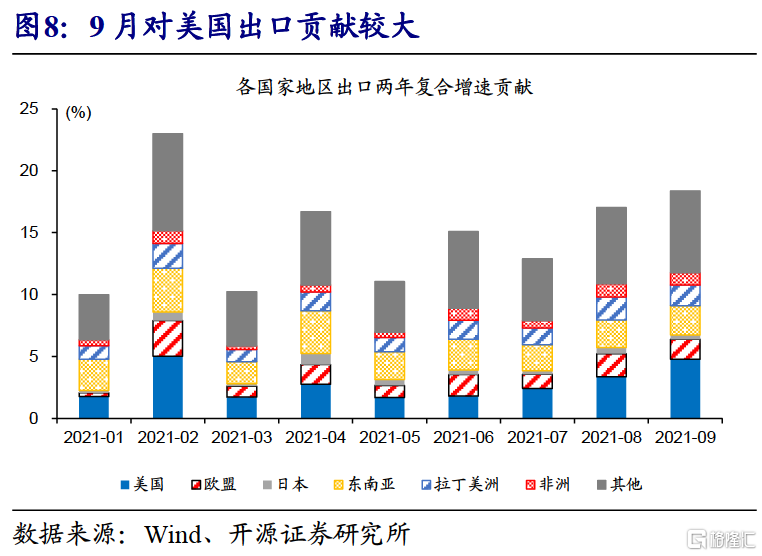

9月,中國對美國、東南亞的出口增速擡升明顯。具體來看,9月出口同比增長28.1%,高於預期21.1%、前值25.6%;兩年複合增速爲18.4%,較8月增速提升1.4個百分點。發達經濟體出口來看,9月,中國對美國出口兩年複合增速25.5%,較8月大幅擡升7.7個百分點;對歐洲、日本兩年複合增速分別爲8.9%、5.9%,較8月下降1.1、3個百分點;對新興市場出口方面,9月,中國對東南亞出口兩年複合增長15.9%,較8月增速提升1.1個百分點,對非洲、拉丁美洲出口兩年複合增長21.4%、23.1%,較8月增速分別下降0.3、2.6個百分點。

分商品來看,多數商品出口增速改善。9月,消費品除塑料製品、汽車、成品油和手機外,其餘商品出口增速均改善;其中,傢俱、燈具、家電、玩具、服裝增速較快,兩年複合增速分別爲55.4%、44%、41%、25.2%、22.9%,較8月增速提升35.2、21.6、4.8、9.5、17.1個百分點;中間品和資本品除自動數據處理設備、汽車零配件、液晶顯示板、鋼材外,其他商品兩年複合增速均有提升。

9月出口回升,或主要由於價格因素

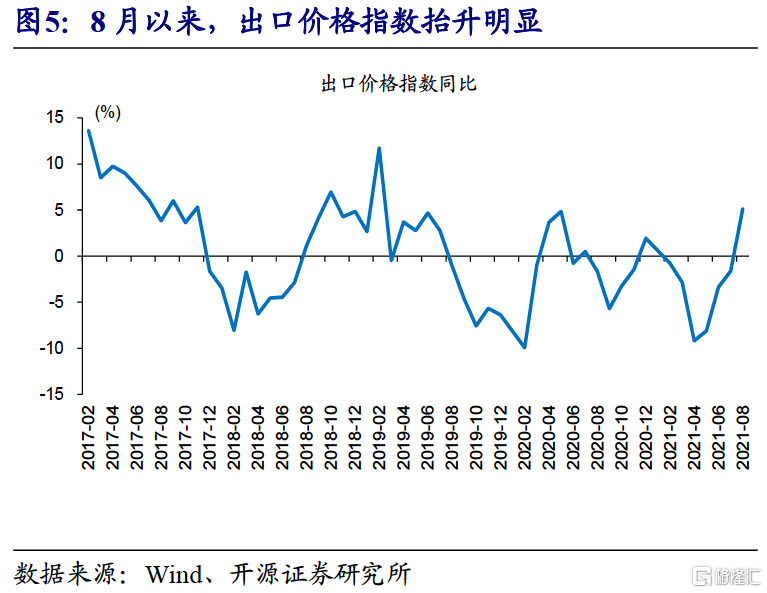

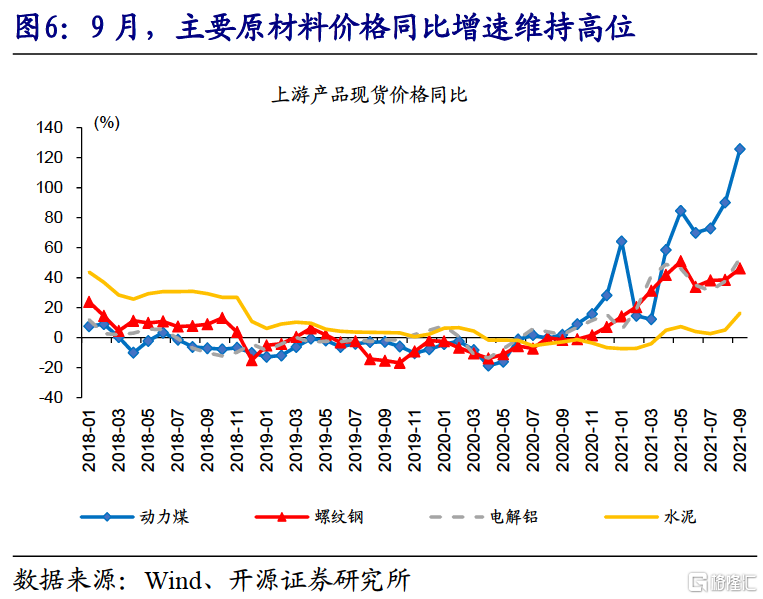

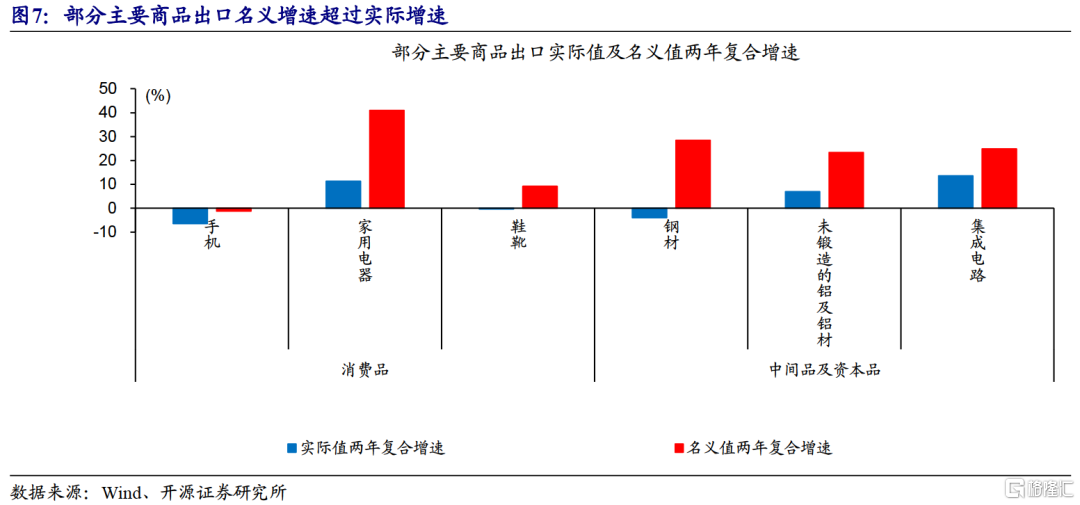

9月出口擡升,或主要由於價格因素。伴隨原材料價格上漲,年中以來,出口價格指數同比增速持續擡升;8月,出口價格指數同比上漲5.1%,較7月增速擡升6.8個百分點;9月高頻數據顯示,主要原材料價格同比增速仍較快,繼續推升出口價格增速。從主要產品的實際出口來看,消費品手機、家用電器、鞋靴實際值兩年複合增速低於名義值增速5.2、29.7、9.4個百分點,鋼材、鋁材、集成電路等,實際值兩年複合增速低於名義值增速32.3、16.4、11.3個百分點。

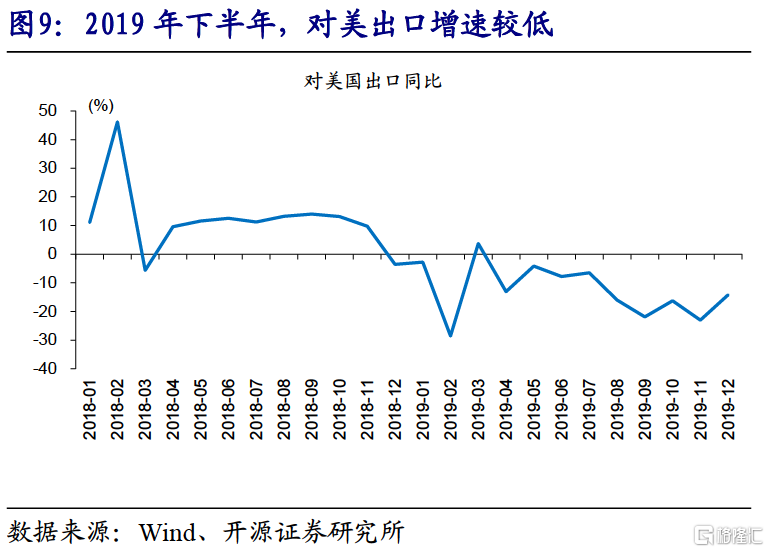

出口增速回升,還受基數效應的影響。9月,中國對美國出口,兩年複合增速25.5%,較8月大幅擡升7.7個百分點,帶動整體出口兩年複合增速提升4.8個百分點,高於東南亞(2.4%)、歐盟(1.6%)、日本(0.4%);剔除對美國出口後,9月出口兩年複合增長16.9%,與8月增速持平。對美出口兩年複合增速大幅擡升,主要由於基數效應;2019年9月,中美貿易摩擦影響下,中國對美國出口同比大幅下滑至-21.9%。

出口短期仍有韌性,中期或有壓力

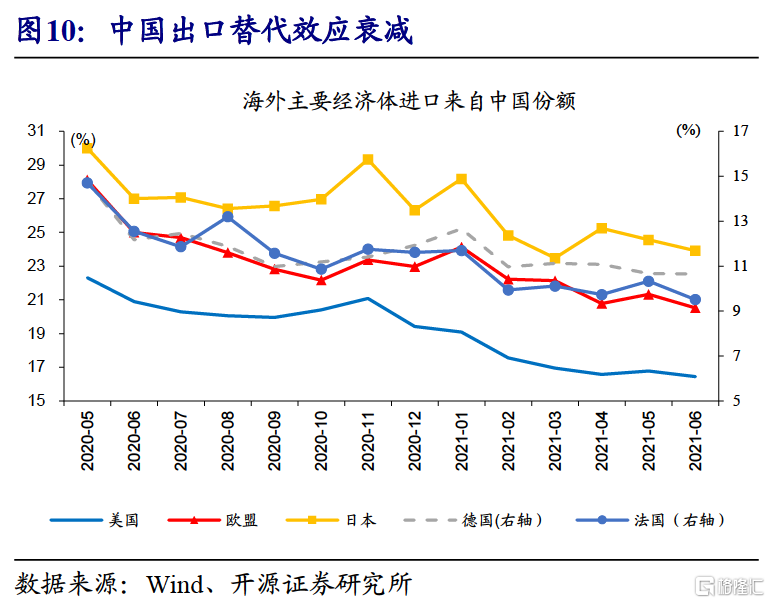

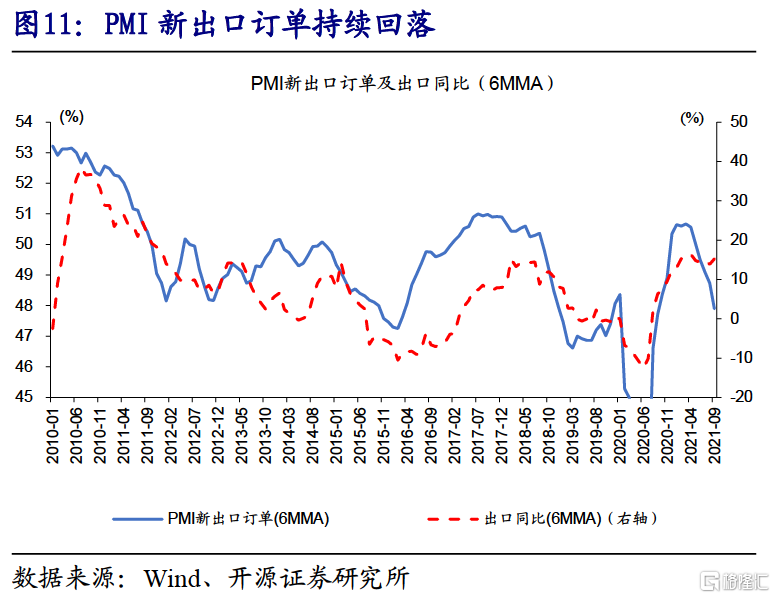

價格因素支撐下,出口短期仍有韌性;中期來看,伴隨替代效應衰減、新出口訂單持續回落,出口或仍有壓力。能耗雙控影響下,工業生產受限,推升價格漲幅,對出口增速構成支撐;中期來看,伴隨海外經濟體疫苗普及、生產活動修復,主要生產型經濟體出口份額回升,中國出口“替代效應”趨衰減。此外,PMI新出口訂單,9月錄得46.2%,較8月回落0.5個百分點,連續5個月在榮枯線以下。

重申觀點:價格因素支撐下,出口短期仍有韌性;中期來看,伴隨海外復工復產,中國出口“替代效應”衰減;同時,PMI新出口訂單連續回落下,出口仍承壓。

經過研究,我們發現:

(1)9月,中國對美國、東南亞的出口增速擡升明顯。具體來看,9月出口同比增長28.1%,高於預期21.1%、前值25.6%;兩年複合增速爲18.4%,較8月增速提升1.4個百分點。發達經濟體出口來看,9月,中國對美國出口兩年複合增速25.5%,較8月大幅擡升7.7個百分點;對歐洲、日本兩年複合增速分別爲8.9%、5.9%,較8月下降1.1、3個百分點;對新興市場出口方面,9月,中國對東南亞出口兩年複合增長15.9%,較8月增速提升1.1個百分點,對非洲、拉丁美洲出口兩年複合增長21.4%、23.1%,較8月增速分別下降0.3、2.6個百分點。

(2)9月,消費品除塑料製品、汽車、成品油和手機外,其餘商品出口增速均改善;其中,傢俱、燈具、家電、玩具、服裝增速較快,兩年複合增速分別爲55.4%、44%、41%、25.2%、22.9%,較8月增速提升35.2、21.6、4.8、9.5、17.1個百分點;中間品和資本品除自動數據處理設備、汽車零配件、液晶顯示板、鋼材外,其他商品兩年複合增速均有提升。

(3)9月出口擡升,或主要由於價格因素。伴隨原材料價格上漲,年中以來,出口價格指數同比增速持續擡升;8月,出口價格指數同比上漲5.1%,較7月增速擡升6.8個百分點;9月高頻數據顯示,主要原材料價格同比增速仍較快,繼續推升出口價格增速。從主要產品的實際出口來看,消費品手機、家用電器、鞋靴實際值兩年複合增速低於名義值增速5.2、29.7、9.4個百分點,鋼材、鋁材、集成電路等,實際值兩年複合增速低於名義值增速32.3、16.4、11.3個百分點。

風險提示:疫苗有效性不及預期。

More Content